Does Vanguard pose a threat to advisers?

The fund giant's online advice platform is viewed by some as a threat, but others see it as complementary. Trevor Hunnicutt reports.

The Vanguard Group Inc.’s decision to expand its web-savvy retail advice service is sending shivers throughout the financial planning community, which has been watching the growth of software-driven investment management platforms with growing apprehension.

The fund manager’s service, Personal Advisor Services, is still a pilot program. But its rock-bottom price and use of both technology and financial professionals to deliver recommendations to investors is drawing assets and even some acclaim from an unlikely source: financial advisers.

The model-based service provides investors a financial plan, asset allocation scheme, ongoing monitoring and re-balancing, performance forecasting and periodic contact with an adviser for 0.3% of portfolio assets annually. The service “typically recommends” Vanguard funds as investments to clients, according to a company brochure.

David R. Hoffman, a spokesman for the largest U.S. mutual fund house, said the program which has been rolled out quietly, will be distributed “more broadly within the next year.”

“I see this as a very important move in the industry, not just in the digital wealth management industry, but in the broader wealth management industry,” said Sophie Louvel Schmitt, senior analyst for Boston-based research consultancy Aite Group.

@DanPrescher1 It’s not just algorithms & low fees. They’re offering at least some access to human advisors too. @ronlieber @felixsalmon

— MichaelKitces (@MichaelKitces) April 15, 2014

Analysts see Vanguard’s move as a milestone in the evolution of wealth management delivery online, posing a major threat to established ways of providing advice and soliciting clients.

Corporate Insight analyst Grant Easterbrook on the momentum robo-advisers are seeing and Vanguard’s potential impact on the market.

Vanguard’s new initiative has already gained investor assets. By the end of 2013, its first year in operation, the new division, which Vanguard executives described as in development and available only to a small number of clients, already managed $755 million in discretionary assets, according to a company brochure. (Company officials declined to furnish updated numbers, citing “competitive reasons.”)

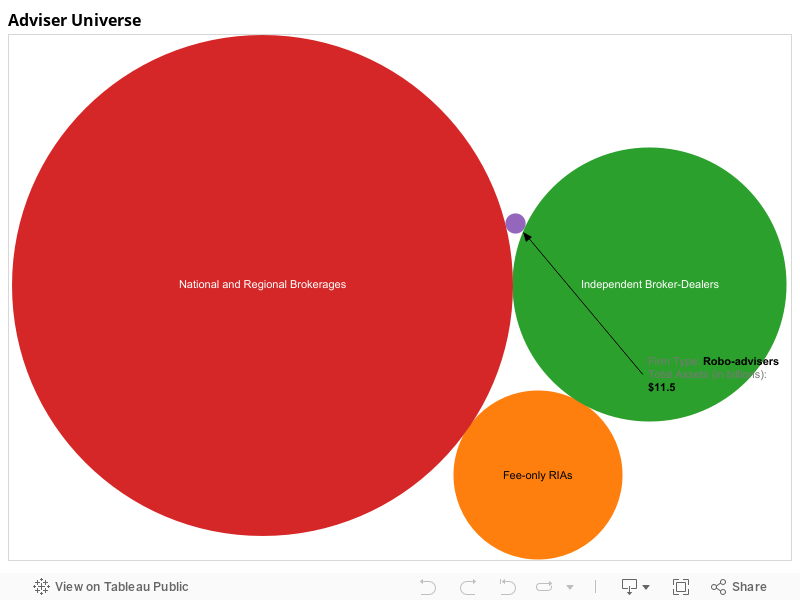

That figure is a pittance in the wealth management field — the four largest U.S. brokerages together employ 52,000 advisers and manage nearly $6.5 trillion. But it already puts Vanguard’s upstart initiative on par with Wealthfront Inc., a leading online startup in the space that is entirely automated, and which last month reported managing $809 million.

A Vanguard executive, Martha G. King, said “plans to create this capability were constructed before Betterment and Wealthfront existed — before they were on the horizon.”

The price of Vanguard’s new service puts it on par with firms that don’t provide continuing relationships with advisers. Wealthfront charges 0.25% on assets over $10,000, while Betterment charges between 0.15% and 0.35%.

Online firms that offer access to advisers cost more — Personal Capital Advisors Corp.’s fees start at 0.95% for the first $250,000.

Catha Mullen, a spokeswoman for Personal Capital, said the firm earns its fee through many services such as visualization tools that cover personal banking. In addition, the firm recommends a broad suite of nonproprietary products and services like tax-loss harvesting and customization.

It remains to be seen how online wealth managers, which have become darlings of venture capitalists, will react. Betterment is rolling out a turnkey asset management platform that will allow advisers to provide service to clients while using its platform and other integrated features to manage client assets cheaply and efficiently.

But speculation abounds, with industry watchers debating the topic this week on Twitter.

A spokeswoman for Wealthfront, and Joe Ziemer, a spokesman for Betterment, declined to make executives available for interviews, citing scheduling difficulties.

Vanguard brings a powerful brand to the market. The firm ranked third, behind Scottrade Inc. and Charles Schwab & Co. Inc., in a 2013 J.D. Power & Associates study that examined self-directed investors’ customer satisfaction in the U.S.

But the fact that Vanguard’s initiative is drawing comparisons to service providers that advisers often pejoratively call “robo-advisers” could put Vanguard in a difficult spot with a major constituency: fee-based advisers, whose relative growth across the channels of the advice business has paralleled Vanguard’s absolute growth in assets. (The firm has tripled assets in its U.S. fund business in the last decade.)

Most advisers don’t see a threat right now. But in Silicon Valley, Wealthfront’s backyard, advisers are starting to feel competition from online wealth managers, according to Ms. Schmitt. She said she spoke with an adviser who has clients considering Wealthfront and, in at least one case, actually holding a separate account with the firm.

Vanguard executives emphasize that the firm is not opening local offices or providing “high-touch” service and that they’ve been providing direct-to-consumer advice services, in some form, for nearly two decades. That’s longer than the world’s third-largest money manager has even had a unit focused on selling its funds through financial advisers in the U.S.

“Vanguard’s retail offering has been in existence since 1996 — it was never offered with an intention to disintermediate advisers who use Vanguard at all,” said Ms. King, managing director of the asset manager’s financial adviser services division. “We’ve had coexistence of these capabilities for quite some time.”

Company filings with securities regulators list more than 200 Vanguard-trained certified financial planners and investment adviser representatives working with the firm, with nearly 150,000 clients served by its financial planning services.

“By and large, the advisers that we call on in my group are generally courting clients that have greater wealth than this offering, targeting ones with as little as $50,000. Many of those investors would never be in the target market of those advisers,” said Ms. King. “Certainly there’ll be some overlap, but not extensive overlap.”

Anecdotally, there’s little evidence of negative reaction at this point. For most advisers, news of Vanguard’s service stirred up an unexpected response: acceptance, and even approval.

Lights out. RT @cullenroche: @Vanguard_Group is about to drop the boom on robo adivors…. https://t.co/SOWPtNCWiT

— Downtown Josh Brown (@ReformedBroker) April 14, 2014

When Amy Jo Lauber heard about Vanguard’s initiative, the West Seneca, N.Y.-based fee-only financial planner posted the news on Facebook for her clients to see.

“While I can hear my husband saying ‘Don’t post that, they’re your competition!’ I assert that no one competes with me based on what only I do and offer,” she wrote, linking to a column mentioning Vanguard’s initiative. “So here are some great alternatives.”

“I thought it was a great idea, which I suppose is an unusual response from a financial planner,” Ms. Lauber said in an interview. “Once in a while I find people who aren’t in a position to compensate me and if I can’t work out a compensation agreement, I like to have these other resources to refer them to.”

Cullen O. Roche, an adviser for Orcam Financial Group, who has been critical of software-based advisers, said Vanguard’s service looks “cool.”

“What Vanguard is doing is more along the right track,” said Mr. Roche. “They’re providing a lot of the automated portions of this business model through implementing technology and a process for portfolio management and financial planning, but they’re making the human element available.”

Mr. Roche said a lot of what his job involves is examining portfolios and cutting underperforming, overpriced hedge funds and money managers, often in favor of Vanguard products, which he sees as sensibly priced. He doesn’t see the fund manager’s new service as a threat.

“As long as there are bad financial advisers, as long as there are people who don’t understand their portfolio, and there are advisers that I don’t think are providing a lot of value, I’ll be in business,” said Mr. Roche. “If Vanguard ran the whole world, I guess there would be no need for me, but that’s not the world we live in.”

Learn more about reprints and licensing for this article.