BlackRock strategists cool on credit

The firm's research arm sees investment-bond bonds hampered by frothy valuations and rising interest-rate risk, but are somewhat bullish on junk-rated debt

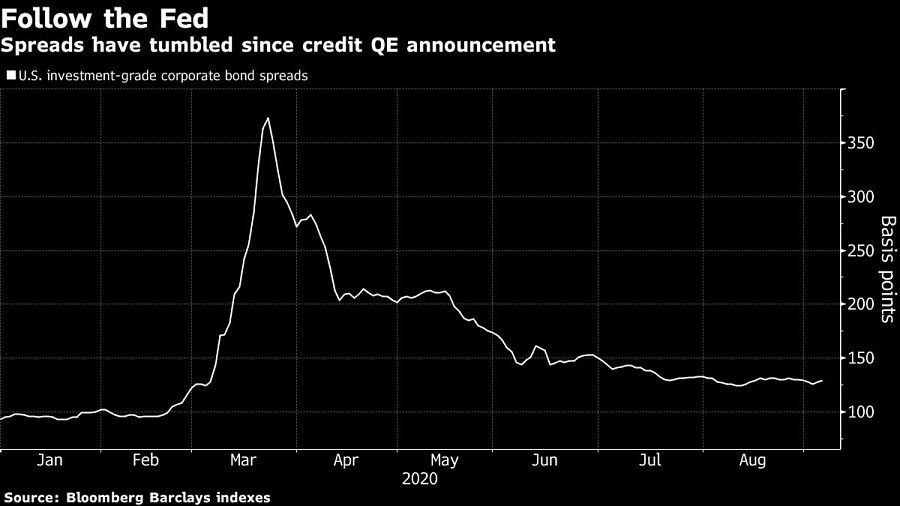

The Federal Reserve famously tapped BlackRock Inc. to help engineer a recovery in corporate bonds from the depths of the corona crisis. Now, strategists at the firm say the rally in investment-grade credit looks exhausted.

BlackRock Inc.’s research arm just downgraded the asset class to neutral from overweight on frothy valuations and rising interest-rate risk. With premiums over government bonds almost back to pre-crisis levels, BlackRock Investment Institute’s chief fixed-income strategist sees little upside while a new fiscal package remains stalled and a contentious U.S. election looms.

The market is “looking for more policy decisions and more money coming into the economy,” Scott Thiel said. “When we look at it from a valuation and policy perspective, as a return asset class, investment-grade credit doesn’t look as attractive as it did when we initiated the long” in late March and early April, he said.

While BlackRock strategists cut their overweight recommendation on investment grade, they’re still “moderately” bullish on corporate bonds overall, especially junk-rated debt. Members of the BlackRock Investment Institute don’t make investment decisions on behalf of the firm.

The cautious tone resonates with a move away from corporate bonds at other firms. Netherlands-based Robeco Institutional Asset Management BV, which oversees 155 billion euros ($182 billion), closed its overweight positions on investment-grade bonds this week. At $20 billion fund manager Unigestion in Geneva, head of macroeconomic research Florian Ielpo prefers equity. And Commerzbank Tuesday cut credit to neutral from overweight to avoid duration risk, while adding to equities and real estate investment trusts.

BlackRock landed the role of investment manager for the Fed’s corporate credit facilities thanks to its experience in buying large amounts of company debt. The Fed impact was swift and dramatic: Spreads relative to government debt collapsed more than 200 basis points and are now just 30 basis points away from a full crisis recovery.

But as more companies rush to lock in cheap funding, the market’s sensitivity to changes in interest rates has jumped to record highs. So-called duration hit 10 years for the first time last month, meaning that a 1% increase in yields would shave off a tenth of the average bond’s value.

High-grade credit “is offering little buffer against risks such as rising rates due to its interest rate-sensitive nature,” according to Thiel and his colleagues.

All this creates a conundrum for funds amassing growing cash that needs to be put to work. Active and passive managers that focus on U.S. investment-grade credit received a record influx of almost $15 billion in the week ended Sept. 2, according to Bank of America analysts. In Europe, high-grade funds saw their 22nd consecutive week of inflows.

Some are going further afield to mine for returns. At Eric Sturdza Investments in Geneva, fund manager Eric Vanraes recently bought the hybrid debt of a Mexican bakery chain. The subordinated notes from Grupo Bimbo S.A.B. de C.V. yielded about 5% until their call date, equivalent to 480 basis points more than U.S. government debt.

He also searched for opportunities in bonds whose coupons step up when they are downgraded to junk, as well as notes that are not eligible either for Fed or European Central Bank purchases.

“There are only a few opportunities because the market is too expensive,” said Vanraes, who helps oversee $3.1 billion. He said finding them is a task that’s “difficult but still possible.”

Learn more about reprints and licensing for this article.