Life Insurance and Annuities

Why a lump sum is not a retirement

For 30 or 40 years, a working person never has to answer the hardest question in personal finance because their employer answers it for them every two weeks. The paycheck shows up. You learn what you can spend by watching what lands in your account. Then you retire, and overnight that question becomes yours alone: how much of this pile can I safely spend this month and every month thereafter, without knowing how long I will live or what the market will do along the way? It is a genuinely difficult problem.

Funds, allocation models, and fee structures – the entire apparatus points toward accumulation. Almost none of it points toward the opposite task: turning that balance back into a reliable stream of income that lasts. A 65-year-old with $800,000 can tell you exactly what they are worth. Ask them what they can responsibly spend each month for the rest of their life, and you will usually get a shrug or a number pulled from an article about the 4 percent rule.

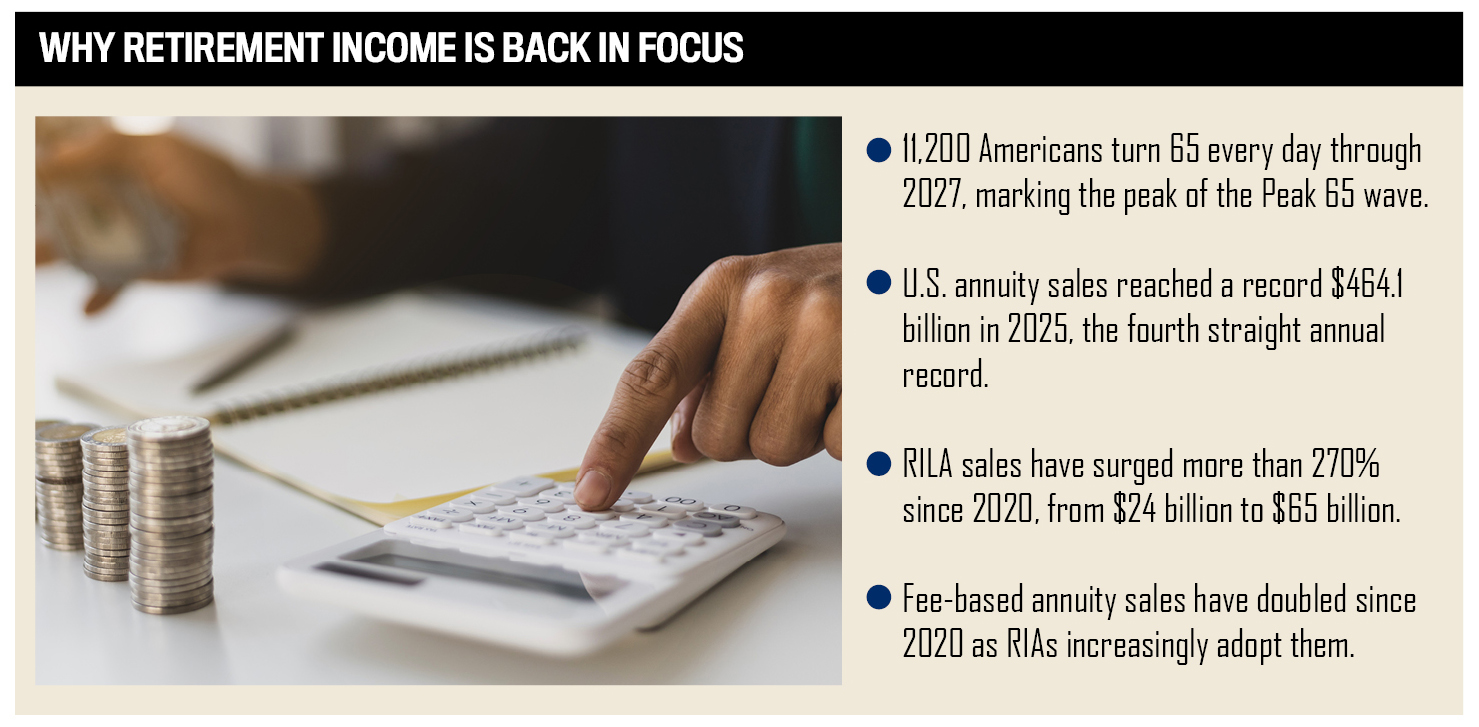

The annuity boom is the market correcting that imbalance, and the scale of the correction is the tell. LIMRA projected U.S. retail annuity sales to finish 2025 above $460 billion, the fourth consecutive record year, and forecasts 2026 sales will hold above $450 billion even as interest rates ease. People are not buying annuities because the products have suddenly become fashionable. They are buying the one thing their portfolios cannot manufacture on their own: an income stream that keeps arriving after the working years stop, for as long as they live.

The income gap is no longer theoretical

The urgency behind that demand became more concrete on June 9, 2026, when the Social Security trustees put a date on the most consequential number in retirement planning. Their annual report projects the retirement trust fund will exhaust its reserves in late 2032, at which point incoming payroll taxes would cover only 78 percent of scheduled retirement benefits. The combined retirement and disability funds would follow by the third quarter of 2034, paying 83 percent absent congressional action.

For a 62-year-old retiring this year, the first scheduled benefit cut now lands inside the first decade of retirement. The one guaranteed income stream most Americans still count on is itself scheduled to shrink.

The private safety net thinned first and further. Only about 15 percent of private industry workers had access to a defined benefit pension as of 2024, according to U.S. Bureau of Labor Statistics data. And the savings meant to replace those pensions are inadequate for much of the cohort now retiring: research commissioned by the Alliance for Lifetime Incomes Retirement Income Institute found that 52.5 percent of the Baby Boomers turning 65 between 2024 and 2030 hold assets of $250,000 or less. This is against retirements that routinely run 25 years or longer. With roughly 11,200 Americans turning 65 every day through 2027, the math compounds annually.

Households that once outsourced longevity risk to employers and the government are now being asked to absorb it themselves, and a growing share of them are choosing to transfer it back to an institution built to hold it: an insurer.

The product is income; the deliverable is behavior

Carriers have redesigned products around the specific risks retirees actually face rather than the accumulation logic of the working years. They have moved away from opaque, proprietary indices toward broad, recognizable benchmarks that an advisor can explain and a client can track.

Allianz Life, which introduced its Performance Lock feature on RILAs more than a decade ago, has expanded the ability to lock in index gains from once per year to as many as 12 times per index year, a concrete example of shifting clients from enduring volatility to managing it. Modern income riders increasingly separate the accumulation and income phases, letting a client participate in growth while securing a protected income floor, and higher interest rates since 2022 reset the economics of those guarantees, making payout levels viable that the prior low-rate decade could not support.

Retirees who doubt their income will last systematically underspend, even when their balance sheets say otherwise. A guarantee that covers essential expenses changes spending behavior, not just portfolio statistics.

This is why the framing of retirement itself has shifted. As Erin Culek, head of financial protection and retirement solutions at Guardian, puts it: “Retirement today is no longer a single event but a multidecade transition driven by longer lifespans, evolving work patterns, and the decline of traditional pensions.” A transition of that length, with phased work, bridge years before Social Security, and rising late-life health costs, cannot be financed with a single withdrawal rate. It requires income that can be layered, timed, and adjusted, which is precisely what current annuity design now permits.

American Equity makes the same point from the distribution side, arguing that the breakthrough comes when the sales conversation stops being about the product at all: “Adoption increases when the discussion shifts from ‘Should I buy an annuity?’ to ‘What risks do we need to manage in retirement?’” That reflects a real reordering of the planning process, where the income problem is diagnosed first and the instrument is chosen second, the way a doctor settles on a treatment only after naming the condition.

What will determine who wins

The structural tailwinds are not in question – execution is. Three capabilities will separate the leaders over the next five years.

First, translation. Annuities still lose more sales to their own complexity than to any competing product. The firms that win will be the ones that make the category legible: plain benchmarks, explainable mechanics, and a conversation anchored in risk rather than jargon. The carriers already doing this report that the diagnosis-first approach changes who buys and how confidently they hold.

Second, distribution breadth. Fee-based annuity sales have doubled since 2020 as registered investment advisors increasingly integrate annuities into planning, according to January 2026 data from LIMRA. It is a trend worth dwelling on because it signals the product crossing from the insurance channel into the fiduciary mainstream. An instrument that was once sold around the edges of a financial plan is moving into its center.

Third, operational speed. Suitability automation, digital applications, and responsive service are no longer differentiators at the margin; they determine whether an advisor writes the business at all. American Equity reports that a next-generation application platform with built-in suitability logic cut its suitability review rate from 40 percent to under 8 percent, with a not-in-good-order rate below 1 percent, and that its average speed to answer the phone now runs about 55 seconds (figures provided by American Equity and not independently verified). Those are not glamorous numbers, but they are the difference between a product that gets recommended and one that gets abandoned mid-application. As the company puts it, financial professionals “don’t have time to sit and wait on the phone. Time is money.”

What the boom is really about

It is tempting to read four straight record years as a victory lap for the industry. It is more accurate and more useful to read it as a verdict on what was missing. For a generation, financial services told people that if they saved enough and invested well, retirement would take care of itself. Half of that instruction was sound. The other half quietly assumed that a lump sum and a spending rule were an adequate substitute for the steady income a career used to provide, and millions of people are now discovering, at the least forgiving moment, that they are not.

Allianz Life puts the client’s actual demand plainly: “Clients aren’t just looking for returns or higher interest rates – they want to be reassured as they seek to achieve their retirement goals.” That should be read as a strategy statement, not a sentiment. Reassurance is the product. Everything else, the caps and buffers and crediting methods, is the machinery that manufactures it. The carriers gaining share understand that they are not selling a yield; they are selling a person the permission to spend what they spent 40 years earning.

This is where the industry’s responsibility gets serious, because a product sold on confidence can be mis-sold on confidence just as easily. The same features that let a retiree spend without fear can be layered into something opaque and overpriced if no one is paying attention. The firms that deserve the growth coming their way will be the ones that keep their guarantees legible, hold their renewal rates, and resist the temptation to win on a headline number they cannot honor for the life of the contract. Trust, once it becomes the category’s main selling point, is also the thing it can least afford to lose.

The annuity industry spent decades as a niche answer to a narrow question. The 2026 trustees report, the arithmetic of Peak 65, and four consecutive record sales years have turned that narrow question into the central one in American retirement: who absorbs the risk of a long life. For most of the past 40 years, the answer was the individual, alone with a balance and a guess. The boom underway is the sound of that answer changing. Whether it changes for the better depends less on how much the industry sells than on how faithfully it keeps the one promise the whole category is built on.