Jump to Winners | Jump to Methodology

Amid market volatility, persistent inflation, and an aging population that increasingly must shoulder retirement security, the work of the best financial planners in the US has never been more consequential.

It’s estimated by Northwestern Mutual that Americans will need $1.26 million to retire comfortably. At the same time, surveys show nearly half of Americans expect to retire with less than $500,000, underscoring a widening advice gap and the need for high-quality planning.

Against this backdrop, the profession continues to expand in both scale and influence. As of December 31, 2025, the number of CFP® professionals reached an all-time high of 107,529, an increase of 4.3 percent over 2024. Last year also marked the largest number of exam candidates in CFP Board history, with 11,037 people sitting for the exam, a 5.7 percent increase over 2024. Revenues from fee-based advisory relationships climbed from an estimated $150 billion in 2015 to $260 billion in 2024, reflecting robust demand for human advice that has grown several times faster than the overall population. McKinsey estimates advised relationships will expand at least 28 percent over the next decade, from 53 million to 67–71 million by 2034.

Yet the value of the best financial planners cannot be measured by growth statistics alone. In 2025, CFP® professionals in the US delivered more than 433,390 hours of pro bono financial planning – an 11 percent increase over the prior year – providing an estimated $130 million in services to households that might otherwise go without advice. This combination of technical rigor and public-spirited service reflects the profession at its best.

This report is where InvestmentNews recognizes those financial professionals who stand out within that landscape – planners who, over the past 12 months, have demonstrated not only strong performance but also integrity, client-centric innovation, and a clear commitment to helping individuals and families reach their financial goals. These financial planners are setting the standard for what modern planning can and should be: goals based, evidence driven, and firmly anchored in the best interests of the client.

“The top financial planners distinguish themselves from their peers by building deep personal relationships with clients and offering behavioral finance coaching, complemented by consistent, proactive communication,” says Andrew Blake, associate director, wealth management team at Cerulli Associates. “They prioritize educating clients about the steps taken to achieve their goals instead of merely providing statements and performance summaries. Personalized, holistic advice is vital to fulfilling fiduciary duties and creating a high-touch client experience that fosters trust.”

As portfolios and products increasingly feel commoditized, Matthew Cuplin is unapologetic about what his firm is really selling: service. As a CFP® professional and CFF®, he has built his practice around a high-touch, highly responsive client experience that he insists is still the exception rather than the rule.

“We believe that the product that we deliver is service,” he says. “Nowadays, technology is amazing at what it can put at your fingertips, and advisors exist all over the US. But what we pride ourselves on is that high level of service and responsiveness to our clients, and it makes them know that we care.”

Research shows clients now prioritize trust, communication, and personalized planning over raw investment performance, with the “human touch” eclipsing returns as the main driver of satisfaction and loyalty.

Cuplin and his team lean into that human element by deliberately positioning themselves as “bearers of good news” in an environment saturated with market scares, geopolitical shocks, and dire economic headlines. The goal is not to ignore risk but to pull clients out of a permanent state of anxiety and back toward the progress they are actually making. That optimism is grounded in process. He says, “We try to look at things in the big picture. That then is the blueprint that we use to make our decisions, to build out a portfolio, and to plan insurance coverages.”

Cuplin’s operating model is designed for efficiency. Midwest Financial Group consolidated operations from three locations into a single flagship office, allowing clients to meet the team’s specialists on the spot.

Community presence is another defining theme. Cuplin attributes much of the recent organic growth to visibility and goodwill in the local area. He and his colleagues regularly teach no-cost classes at libraries and community centers, treating those sessions as education and outreach rather than prospecting events. That work lands against a national backdrop in which financial illiteracy is estimated to cost American adults more than $200 billion a year, underscoring the stakes of better decision-making for everyday households.

“Some of the best meetings I’ve ever had were with people who didn’t end up working with us,” he says. “I’m a big believer in karma from the aspect of if you put something out there, it comes back to you.”

Cuplin sticks to the mantra of serving everyone, with a client walking in today experiencing the same level of care, discipline, and consistency as one who started a decade ago.

Financial advisor–senior partner at Summit Global Private Wealth (Utah)

RJ Cunningham has a simple rule for first meetings: no product talk, no annuities, no option strategies, and no alternatives. Instead, he focuses on mapping goals, trade-offs, and timelines before a single investment is proposed. “When I meet with a client, I’m not talking about options trading, stocks, or alternative investments,” Cunningham says. “First, we’ve got to get the plan in place.”

That planning-first stance resonates in a market where anxiety is high and headlines are noisy. Nearly three in four US investors expect stock market volatility to persist through 2025, and a growing share say it is causing them to check accounts more often and second-guess decisions. Cunningham views those conditions not as a headwind but as an opportunity for differentiation. “Anytime volatility enters, I tell other advisors on our team, this is ‘go time’ – this is what’s going to separate you from every other advisor,” he says.

In practice, that means phoning clients more when markets are rough and reaching out before nervous investors call him. His first question when someone fears a looming recession is disarmingly basic: When do you actually need this money? If the goal is 15 or 20 years away, he argues, a short-term drawdown is usually a distraction, not the real risk.

Cunningham, who is a CFP® and ChFC®, leans heavily on metaphor and education to keep clients from making panicked moves. He likens market turbulence to a bumpy flight: when the plane shakes, the pilot doesn’t tell everyone to stand up and walk around – passengers are told to buckle up and ride it out. The same logic, he says, applies to portfolios mid-correction. Abandoning a long-term strategy in midair often does more damage than enduring volatility. That framing is backed by emerging research on advice: in a 2025 Vanguard study, 86 percent of advised investors reported greater peace of mind compared with managing finances on their own.

Referrals tend to come from clients who felt listened to rather than pitched, whether the conversation centered on Roth conversions, Social Security timing, or sustainable withdrawal rates. This is a key driver of how Cunningham’s own metrics have scaled: assets under management (AUM) has grown from roughly $100 million to about $500 million in recent years, with a long-stated goal of reaching $1 billion. But he says the motivation behind that target has shifted. What began as an ambitious number he wrote down in his early 20s has evolved into a measure of how many retirements he can help steward over decades.

That long-term commitment is rooted in a line he discovered in his great-grandmother’s journal: “You help other people get what they want, and you’ll get what you want tenfold.” For Cunningham, the compounding effect of that philosophy shows up less in asset totals than in something harder to quantify, clients who keep showing up or referring others.

Managing director and partner at Steward Partners (Florida)

Clients don’t just come to Faiza Kedir for asset allocation or tax efficiency; they come because she makes a point of understanding the people behind the balance sheets – their families, aspirations, and the legacy they hope to leave.

In a business that can default to spreadsheets and product menus, she positions herself as a long-term partner in her clients’ financial lives. “Clients appreciate having someone who listens carefully, explains complex topics clearly, and helps them make thoughtful decisions during both calm and uncertain markets,” she says.

That philosophy has been stress tested over the past 12–18 months, as investors have navigated inflation worries, rate moves, and intermittent bouts of volatility. Rather than chase headlines or try to outguess every twist in the news cycle, Kedir has doubled down on fundamentals: a disciplined plan and the emotional discipline to stick with it. She emphasizes diversified portfolios, regular check-ins on risk tolerance, and a cadence of proactive communication so clients understand not only what they own but also how each piece supports their objectives. Industry research continues to back that approach; investors with a written financial plan report higher confidence and are less likely to make panic-driven changes during market swings.

Adaptability has been another defining theme in Kedir’s recent work. She notes that markets, regulations, and client circumstances are in constant motion and that effective advice requires both technical fluency and the willingness to adjust as life changes. In one recent case, a newly retired professional was shifting from accumulation to income. Rather than focus narrowly on withdrawal rates, Kedir designed a comprehensive roadmap that integrated retirement cash flow, tax strategy, estate planning, and charitable goals, giving the client clarity not only on “how much” to draw but also on how their money could support the causes and people they care about over time.

She cites the example of a recently retired professional transitioning from accumulating wealth to generating sustainable income. “Together we developed a comprehensive plan addressing retirement income, tax considerations, estate planning goals, and charitable giving priorities,” Kedir says. “While every client situation is unique, this reflects my philosophy of thoughtful planning and long-term partnership.”

Partner at Fiduciary Financial Group (California)

By the time many wealthy retirees reach Trevor Scotto’s office, they are worn out from juggling a disjointed cast of CPAs, advisers, and specialists who never seem to be on the same page. Scotto’s differentiator is that tax and wealth management quite literally sit at the same table. Drawing on his own deep tax background, he and his in-house CPAs handle the heavy technical lifting, translating the results into plain English.

Clients receive high-level, integrated planning without having to decode acronyms or referee between professionals who won’t take ownership. That positioning is increasingly powerful in a landscape where tax efficiency has become a central value driver for RIAs, with industry research highlighting tax-aware strategies as a key competitive edge in attracting high-net-worth clients.

The same ethos has guided Scotto’s approach through the last year of market turbulence. Rather than reacting to every headline, he leans on a risk capacity, needs-based framework that starts with what a family actually requires to fund retirement and then works backward. It is an intentionally objective philosophy designed to strip out the emotion that so often derails investors. Once the plan is in place, the mandate is to stay disciplined, keep scanning for financial and tax planning opportunities, and let clients focus on living their lives. Recent investor surveys suggest that advisers who proactively communicate around volatility and connect portfolio moves to long-term income needs enjoy significantly higher loyalty from retirement-age clients, validating Scotto’s approach.

Over the past year, one lesson has crystallized for Scotto: as wealth and business scale, the hunger for simplicity has to grow in parallel. Having recently crossed $1 billion in AUM while raising three young children, he has become even more convinced that time is the only truly non-renewable asset. That insight shapes both his firm and his life. He has surrounded himself with what he calls “insanely intelligent” specialists and built a culture where complexity is managed centrally so clients don’t have to carry it.

A recently retired couple illustrates how that plays out. For years, their adviser told them to “ask the CPA,” while the CPA sent them back to the adviser, promising strategies surfaced but were never implemented, and tax advice focused narrowly on the current year. Scotto’s team ended the ping-pong immediately. With tax and wealth experts in one room, they combed through the couple’s balance sheet, designed a unified, needs-based portfolio, executed a Roth conversion strategy, consolidated scattered retirement accounts, harvested tax losses and gains, updated beneficiary designations to match new legacy goals, and built a straightforward Social Security plan. What had been a source of frustration became a coherent, actionable roadmap.

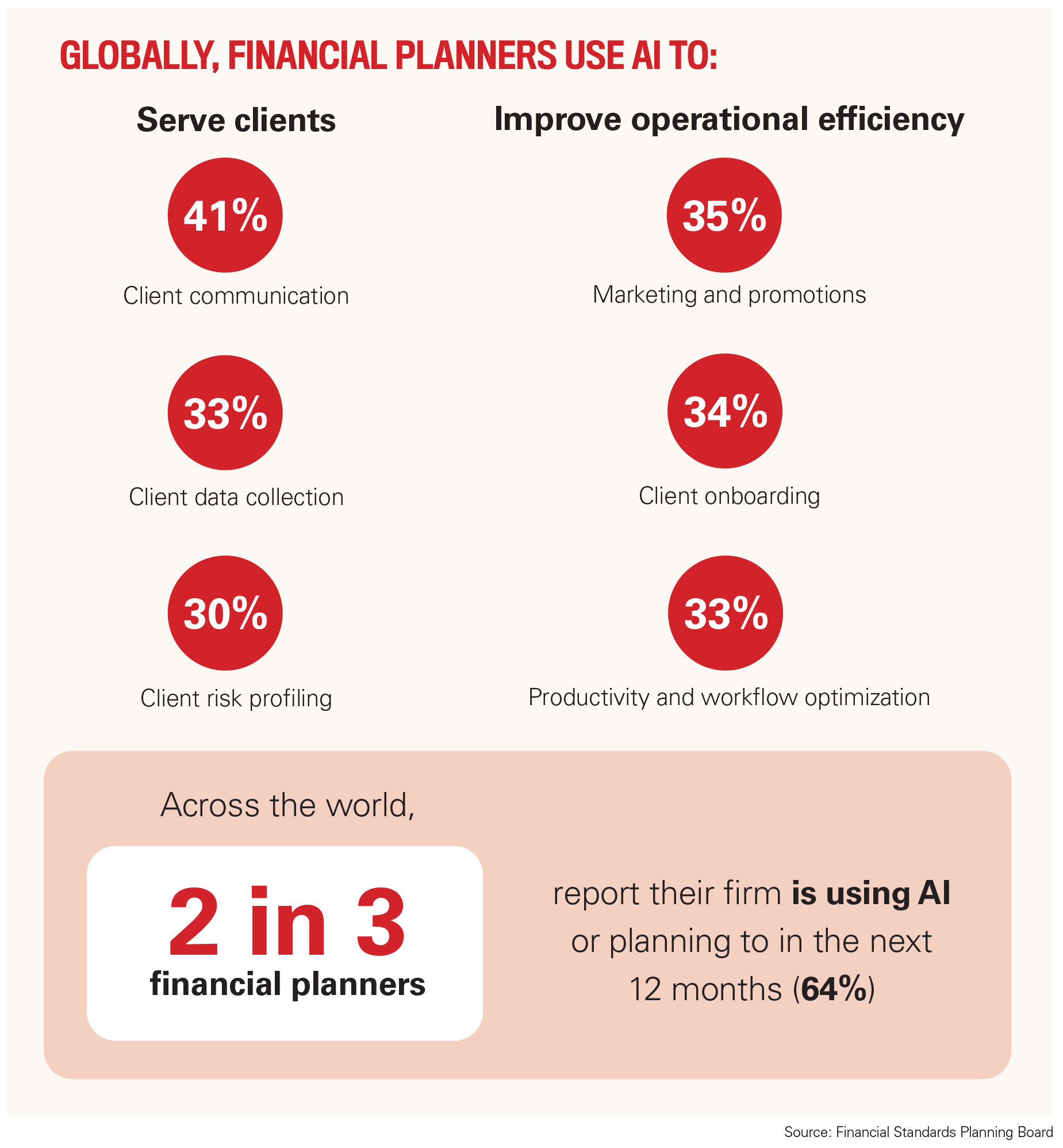

AI is moving quickly from experiment to embedded tool. A 2026 Schwab study of RIAs found 63 percent of advisers are already using AI, most in early stage or “test and learn” mode, with the biggest impact showing up in administrative work and client communications rather than in pure investment selection.

Scotto is part of this trend, as he, along with his team, uses a suite of AI tools to capture pristine meeting notes and automate documentation, particularly on complex retirement and tax plans where missing a detail can be costly. He says, “Right now we use Gemini, Jump AI, and Contio, and we are also dipping our toes into Hazel AI.”

With the machines handling accuracy and admin, Scotto is able to be fully present in the room, asking better questions, spotting planning opportunities in real time, and maintaining the proactive engagement clients value most.

While Kedir incorporates portfolio management platforms, planning software, and secure portals to monitor accounts, model “what if” scenarios, and keep clients engaged. “Technology remains a tool – human judgment and experience are essential when guiding clients through complex financial decisions,” she says.

This chimes with the market, as the Natixis 2025 global survey of individual investors shows only 40 percent say they trust algorithms and AI to support their financial decisions, and separate research finds nearly six in 10 expect the future of advice to be a human–AI partnership rather than a handoff to machines.

Blake adds, “An increasing number of advisors are adopting model portfolios, reducing the time spent on daily portfolio monitoring and compliance, and allowing them to focus more on delivering a premier client service experience. This includes upgrading in-house technology to improve efficiency and guide clients toward investment goals.”

Advisory work has long been portrayed as a solo profession, but the data show a clear payoff toward team models.

Cuplin frames his own success as inseparable from his team. Clients go through the same disciplined process with outcomes tailored by other advisors, plus specialists in taxation, insurance, and administration. That structure creates deliberate redundancy – the “next person in line” can pick up right where he left off – giving clients continuity and peace of mind if life happens to any one adviser.

Consolidating into a single flagship office has amplified the benefits: efficiency is higher, “sharing of ideas” is easier, and the culture of camaraderie is now something clients can feel as they meet, in one place, a CPA for tax planning, a Medicare specialist, and other experts in an unusually polished but accessible setting designed for “millionaires to missionaries” alike. Emotionally, the team also helps him carry the weight of difficult cases; having trusted colleagues to “bounce things off” matters when clients are facing illness or major life shocks.

Studies echo the advantage, with an analysis by Cerulli highlighting that team-based practices generate higher median AUM per advisor ($100 million versus $72 million for solo models) and are better positioned to offer a wider range of planning and high net worth services.

And Cunningham takes a similarly intentional approach. He insists every new prospect meeting includes at least two advisers so clients feel they are “working with a team,” typically pairing himself with a partner or junior planner. For households with more than $5 million in liquid assets, he extends that model into a dedicated family office group, ensuring multiple specialists are in the room for key decisions.

Client benefits are both practical and emotional: broader listening, more perspectives, and better risk management during the volatile periods he calls “go time” for proactive outreach. Clients see that someone will always answer the phone and that their portfolio is backed by an actively managing investment team rather than a single decision-maker.

For Cunningham himself, the team model has improved close rates, exposed his own blind spots, and created a scalable path toward his billion-dollar AUM ambition. “What I’ve found is that 50 percent of something is better than 100 percent of nothing. It goes back to that quote ‘If you want to go fast, go alone. But if you want to go far, go with somebody else.’”

To identify outstanding financial planners across the United States, InvestmentNews conducted a nationwide, nomination-based survey between November 3 and 28, 2025. The process was designed to recognize financial professionals who demonstrate excellence, integrity, and a strong commitment to helping clients achieve their financial goals, based on achievements during the past 12 months.

Nominations were accepted from industry peers, colleagues, clients, and self-nominated individuals. Only financial planners who were formally nominated during the survey period were considered for evaluation. Nominators were required to submit detailed information for each nominee, including professional credentials, areas of expertise, and notable achievements from calendar year 2025.

All nominations were subject to review and confirmation by the nominee’s compliance team to verify accuracy, authenticity, and adherence to ethical and regulatory standards before being accepted into the evaluation process.

A total of 231 nominations were received. Following an objective review and benchmarking process conducted by the IN editorial team, 80 financial planners were ultimately selected for recognition.

Each nomination was evaluated through a qualitative, information-based assessment focused on achievements and contributions over the previous 12 months. Evaluation considerations included:

professional credentials and qualifications

demonstrated areas of specialization or expertise

significant professional or business achievements

evidence of integrity, professionalism, and client-focused service

All entries were reviewed consistently to ensure fairness, objectivity, and editorial independence.

This recognition highlights financial planners who demonstrated professional excellence and meaningful achievement during calendar year 2025, based solely on the information submitted and verified through the nomination process.

To comply with regulatory and advertising standards, this recognition is not based on:

investment performance or portfolio returns

client testimonials, endorsements, or satisfaction metrics

quantitative business metrics such as assets under management (AUM)

any criteria not expressly stated in this methodology

There is no fee to nominate, self-nominate, or be considered for this recognition. This award is not pay-to-play. Some recipients may choose to purchase optional promotional or marketing materials from IN after being selected; however, such purchases have no influence on the nomination process, evaluation criteria, scoring, or final selection.