Starting this year and for the next decade or so, the US expects a massive turnover of wealth from one generation to the next, and at least two more generations. As baby boomers enter retirement, they are projected to hand down more than $80 billion in assets to Gen X, Millennial, and Gen Z descendants.

This is expected to become one of the single largest movements of assets in our nation’s history. Depending on how you look at it, this is a situation that can promise massive problems or a myriad of opportunities. Children, grandchildren, and possibly great-grandchildren will inherit substantial wealth, but may not have anyone to turn to for sound financial advice. How, then, can advisors and RIAs provide financial planning services to their clients’ heirs?

In this article, we'll share insights on DIY planning for KOCs (kids of clients). InvestmentNews delves into important questions like the pros and cons of DIY planning for KOCs and many more.

There is no handbook, nor hard-and-fast rules for doing DIY planning for NextGen clients, or, as financial planner Chuck Failla, CFP like to call them: KOCs (kids of clients). Iff there were, it simply wouldn’t be “DIY”. So, for the intrepid RIA or financial advisor, it helps to be insightful and creative.

The boomer generation that you or your senior partners serviced are markedly different from the younger generations that you want to continue getting business from.

Baby boomers, for instance, were accustomed to working in large corporations, often staying in the same job for years until they retired, hardly ever switching jobs, getting fired or retrenched.

Gen X and Gen Ys (millennials) or Gen Zs, meanwhile, have different beliefs and ideas about work and money. For starters, these younger generations seek work-life balance, social interaction, immediate rewards and results from work, and a quick climb up the corporate ladder.

Some data to support your DIY planning for KOCs (kids of clients) - according to a 2023 study:

This is why advisors should take the time to engage their clients’ heirs early. Capturing their business requires that advisors fully understand that their priorities and needs center around keeping and growing the assets within their families.

That said, here are some ways RIAs and financial advisors can ensure they continue business relationships with their clients’ children and grandchildren (and succeeding generations beyond):

According to this 2022 report, 80% of inheritors who are introduced to a financial advisor at a young age decide to work with them. Meanwhile, only 54% of inheritors who are introduced to an advisor as adults or young adults go on to work with their family’s financial professional.

That same study found that 87% of future inheritors plan to enlist the services of a financial professional at the appropriate time. Seeing that overlap, advisors should consider introducing themselves to their clients’ children as early as possible.

This contrasts with the “standard practice” of so many advisors attempting to secure business from pre-retirees and retirees. While they are most in need of immediate financial advice, connecting with young prospects can benefit your firm in the long term.

Getting clients via referrals is neither quick nor easy. It takes some time, effort, a bit of planning, and presence of mind. While it helps to get a nudge from the parents, appealing to future KOCs ultimately depends on the individual advisor’s or RIA’s sales and conversion skills.

These actions spell the difference in earning business from your clients’ children – all part of your DIY planning for KOCs (kids of clients) toolkit:

As you know, financial advisory is a relationship-based and relationship-dependent industry. To convert your referrals, convince them why having you as their financial advisor would benefit them the most.

There is an epidemic of financial illiteracy and miseducation in America. It’s an ugly truth that many young people who are would-be inheritors, would-be investors, or both, do not have access to truthful and dependable sources of financial information.

A survey shows over half of Gen Y and Gen Z have received poor financial advice after a windfall. With $84 trillion expected to change hands, ensuring sound financial planning is more crucial than ever. https://t.co/UeVTmEXCRz

— InvestmentNews (@investmentnews) May 21, 2024

This is certainly not due to a lack of desire for financial literacy. The financial illiteracy epidemic can be mostly attributed to a lack of accurate and appropriate information that young investors find on social media. Young, would-be investors and potential clients often scour platforms like Facebook, YouTube, TikTok and Reddit for financial information and advice. Even though there are still plenty of good financial books around, social media has become a favored source of financial knowledge.

Read more: Top 10 best books on real estate investing

The good news is that there are some financial influencers or “finfluencers” who can give sound and helpful tips on basic financial principles. The bad news is that this is no substitute for personalized advice for the unique financial needs and goals of individual clients.

That is where experienced RIAs and advisors can step in to fill the real, growing need for financial advice. Thanks to the internet and the fact that many KOCs use it to seek professional financial advice, you can easily become one of their go-to resource persons.

You can “teach on the side” by having and maintaining a presence on the very same social media platforms that KOCs frequently subscribe to and visit for financial advice. What’s more, you can host live events and webinars to build a deeper connection through these touch points with prospects, demonstrating both your ability and willingness to help.

For many finfluencers, this is often part of their marketing strategy – it works as an ad for your services, a platform to launch you as one of the key opinion leaders in the financial space, and even as a virtual calling card KOCs can use to reach out to you.

Everyone wants their opinions validated and listened to, and your clients’ children are no exception. They may not have a lot of assets now, but with the right guidance, they could make bank as well as inherit their parents’ or grandparents’ wealth.

Once you identify potential KOCs and touch base with them, offer an attentive ear. Share tips to help them get where they would like to be financially regardless of their present financial position. Offer advice that suits their needs and objectives but know when to step aside and develop a deeper connection.

When you first meet with KOCs, making them feel listened to and understood cannot be overstated. The presenter in this video gives tips on what to say to KOCs, when they’re ready and open to hear your pitch:

While empowering your clients with information, remember that younger people need to know and feel that they are on an equal playing field with you. Their situation will change over time, and it’s crucial that they realize you are a trusted resource for them now and in the future.

KOCs want to make their own mark and not just follow their parents’ choices. Let them know they are in charge of their own destiny and goals when it comes to their financial plan.

KOCs are the next generation of investors. What makes them unique is their tech-savvy nature, and their willingness and adeptness at using tech tools for financial matters. You and your practice must be in line with them.

One way to do this is to adapt the same tech apps that can be of good use to both advisors and KOCs. “We view our client portal as a fundamental tool that fosters engagement across all demographics. It drives advisor/client engagement through advisor-led, client-led, and hybrid models,” said Chad Porche, SVP of product management at financial tech company eMoney Advisor.

“The portal provides the advisor with important data that helps source opportunities to build and grow client relationships by identifying changing priorities, goals and circumstances where the advisor can help, which can include children of clients. Currently, it is used by more than 1 million end-users for account aggregation, budgeting, storing valuable documents, and more.”

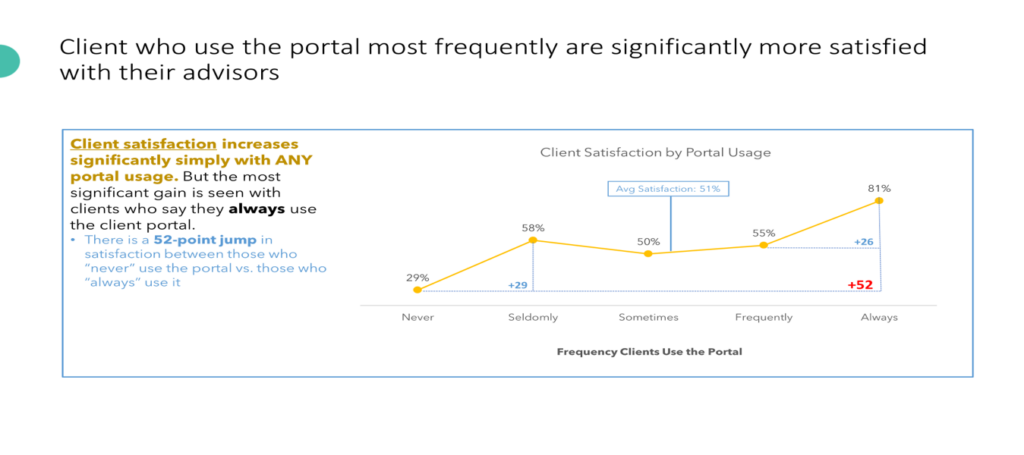

Porche further backs up eMoney’s utility with hard evidence. “Our research continues to show us that a client portal directly impacts the planning experience and leads to higher client satisfaction. You can see how satisfaction increases in the image below, which highlights stats from eMoney’s 2023 Beyond the Plan, The Evolution of Advice study.”

“If an advisor is looking to expand a relationship and engage with their clients’ children, we recommend that they give those children a look into the client portal and showcase the possibilities that lie within the planning relationship,” Porche said.

Apart from apps, it’s extremely important to meet younger generations of investors where they do business, which is often online or via cell phones. This can take less tech-savvy advisors a bit of time to adjust to doing business this way, but the payoff is immense.

Leveraging the tools of the 21st century allows you to do business with any client, not merely those who stand to inherit significant amounts of wealth. For instance, if you’re looking to connect with clients across state lines, you can use video calls to overcome geographical barriers and differing time zones.

RIAs and advisory firms also have the option to place their business online to ensure accessibility, no matter where they are. Younger generations need your help but require that you meet them halfway. Use technology to showcase your skills, flexibility and personality, which could make the KOC’s acceptance of your expertise go smoother.

Putting together and assigning a younger, more diverse team makes it easier for your firm to relate to KOCs. This move can also give KOCs a better chance of success in the pursuit of their goals.

Younger and more diverse advisors may also be more eager to engage with younger clients, whether that be via the way they talk or due to a mutual understanding of modern trends and desires.

Young women KOCs are another demographic that shouldn’t be ignored. With women’s wealth growing faster than ever, this is also the perfect time to hire more women advisors, as they can offer a different perspective and identify with your target clients’ issues.

One lesson to take away from this article is this: however crucial it is to use the tech tools available to woo the next generation of clients, building a relationship with them is still a key factor. Building relationships with KOCs is a win-win situation. Not only do you help longtime clients’ families preserve their wealth for future generations, but you also ensure that your RIA has continued business.

Bookmark our special goRIA section to boost your knowledge, get the latest news, and know the opinions of experts on the RIA practice.

Three advisors who left wirehouses and broker-dealers say the hardest part wasn't the client conversation — it was everything they didn't expect

CEO Ryan Parker says the program supports EP in the industry's "war for talent."

RIA platform Advisory Services Network is tapping into demand for advisors looking to jump from wirehouses and independent broker dealers

Masterworks was launched in 2017 but its RIA, Masterworks Advisers, is just three years old.

The RIA plans to expand its footprint across the U.S. while using AI to free advisors from back-office tasks

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.