A mass exodus of money, an $11 trillion wipeout, and the worst losing streak for global stocks since the 2008 financial crisis. The bad news is that it may not be over yet.

The selloff in the MSCI ACWI Index has dramatically lowered valuations of companies across the U.S. and Europe, but strategists ranging from Michael Wilson at Morgan Stanley to Robert Buckland at Citigroup Inc. expect stocks to fall further amid worries of high inflation, hawkish central banks and slowing economic growth, especially in the U.S.

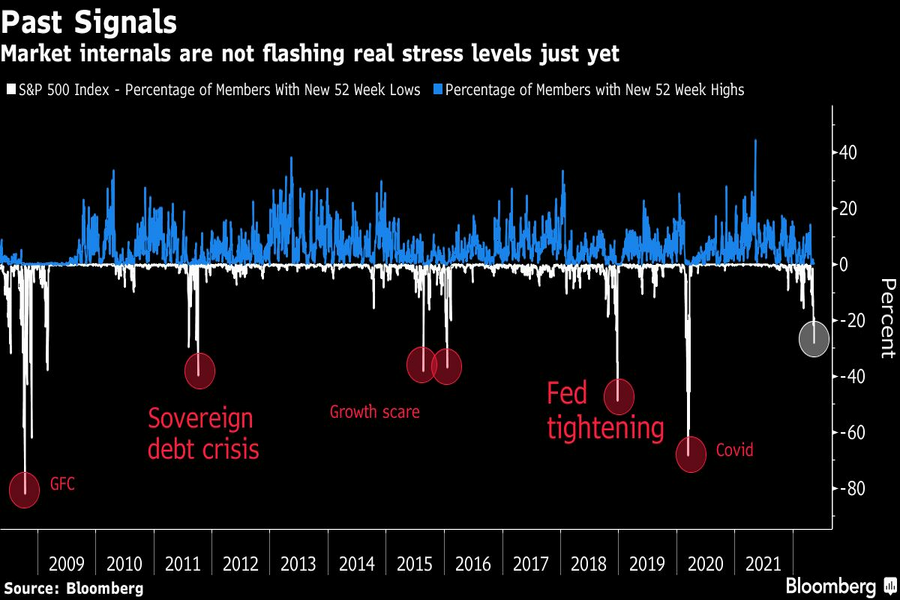

Money is continuing to leave every asset class and the exodus is deepening as investors rush out of names like Apple Inc., according to Bank of America Corp. Historically significant technical levels for the S&P 500 show the index has room to fall nearly 14% more before hitting key support levels, while the share of companies that have so far hit a one-year low is still a far cry from the number during the economic growth scare that slammed stocks in 2018.

“Investors continue to reduce their positions, particularly in technology and growth stocks,” said Andreas Lipkow, a strategist at Comdirect Bank. “But sentiment needs to deteriorate significantly more to form a potential floor.”

On the other side, some say the rout has already created pockets of value across sectors including commodities and even technology, which is valued on future earnings growth and therefore, generally shunned during periods of high interest rates. The Nasdaq 100 rallied on Friday, but it still closed the week down over 2%.

Goldman Sachs Group Inc.’s Peter Oppenheimer has been among the most high-profile strategists to say it’s time to buy the dip, while Thomas Hayes, chairman at Great Hill Capital LLC, said “old school tech” stocks including Intel Corp and Cisco Systems Inc. were now trading at attractive multiples.

But amid the morsels of value, the broader market looks to be buckling as recession creeps more and more into the conversation. And even as growth worries mount, the inflation focus at the Federal Reserve and other central banks means investors can’t count any more on the monetary elixir that’s helped to keep alive the long-running bull market.

The MSCI ACWI has fallen for six straight weeks, the Stoxx Europe 600 is down 6% since late March, while the S&P 500 has dropped more than twice as much.

Here are some key metrics showing the potential downside for stock markets.

The S&P 500 is still about 14% above its 200-week moving average, a level that’s previously been a floor during all major bear markets, except for the tech bubble and the global financial crisis. Strategists at Canaccord Genuity say there could be further declines on Monday on forced margin selling after yet another red week for the U.S. benchmark.

For all the recent declines — the S&P 500 is down more than 13% from its high on March 29 — stress indicators also aren’t at levels seen during comparable slumps. Fewer than 30% of the benchmark’s members have hit a one-year low, compared with nearly 50% during the growth scare in 2018 and 82% during the global financial crisis in 2008.

In addition, the 14-day relative strength index suggests the S&P 500 isn’t yet at the floor. While the Stoxx Europe 600 Index entered into oversold territory last week, the U.S. benchmark has not yet hit that level, which is generally a precursor to a rebound.

Defensive stocks have been in demand as the specter of slowing growth hammers economically sensitive cyclical sectors. The Stoxx 600 Defensives Index is flat in 2022 versus a 15% drop for cyclicals, and strategists at Barclays and Morgan Stanley expect that trend to continue. At UBS Wealth Management, Claudia Panseri sees pricing for a “mild recession” in the cyclical-versus-defensive relative performance.

Comparison with past periods of defensive strength also signals the potential for more to come. Relative gains this year still trail the performance in 2016, brought on by a slowdown in China and Brexit worries, and in the early days of the pandemic in 2020.

Although valuations of technology stocks have fallen sharply — the tech-heavy Nasdaq 100 now trades at about 20-times forward earnings, the lowest since April 2020 — some strategists expect them to remain under pressure from aggressive monetary tightening by central banks.

Tech stocks just suffered their biggest weekly outflows of the year, according to Bank of America. And even after the crushing price drops, Valerie Gastaldy, a technical analyst at Day By Day SAS, says the sector is at risk of losing another 10% before finding a floor.

“I don’t think we have seen capitulation just yet,” said Dan Boardman-Weston, chief executive of BRI Wealth Management. “This week has been pretty brutal, and investor sentiment, especially in the technology area, is shot to pieces. We’re going to have a tricky few weeks and months ahead.”

A new proposal could end the ban on promoting client reviews in states like California and Connecticut, giving state-registered advisors a level playing field with their SEC-registered peers.

Morningstar research data show improved retirement trajectories for self-directors and allocators placed in managed accounts.

Some in the industry say that more UBS financial advisors this year will be heading for the exits.

The Wall Street giant has blasted data middlemen as digital freeloaders, but tech firms and consumer advocates are pushing back.

Research reveals a 4% year-on-year increase in expenses that one in five Americans, including one-quarter of Gen Xers, say they have not planned for.

Orion's Tom Wilson on delivering coordinated, high-touch service in a world where returns alone no longer set you apart.

Barely a decade old, registered index-linked annuities have quickly surged in popularity, thanks to their unique blend of protection and growth potential—an appealing option for investors looking to chart a steadier course through today's choppy market waters, says Myles Lambert, Brighthouse Financial.