Every time there's a potentially transformative development in advisor technology, it seems to trigger a fresh round of debate over what the value of an advisor really is. When mass-market spreadsheet tools like VisiCalc and Lotus-1-2-3 and later Excel first came out, people wondered whether there was any need to pay a financial planner to run cash flow projections and time value of money calculations when consumer tools could do it themselves with software at a fraction of the price. Similarly, when more powerful advisor-specific comprehensive planning software like eMoney and MoneyGuide came along, people wondered whether a consumer-facing version of the same tools would eliminate the need to hire an advisor who could run them. Later, robo-advisor tools like Betterment and Wealthfront caused consternation over their ability to manage an asset-allocated portfolio at a fraction of the cost of a human advisor. And now as generative AI tools like ChatGPT, Claude, and Gemini have emerged over the last few years that can research and answer questions on-demand, more than a few people have wondered why you would hire an advisor to create a financial plan when ChatGPT can create something (almost?) as good instantaneously.

But as much anxiety as these tools may have caused among advisors, after the fact it turned out that each barely registered as a blip among clients who actually hired advisors. Because none of these tools got in the way of why most clients hire advisors, which is to have a human who will listen to them and make them feel heard, give them a recommendation that will best suit their needs by how well they're understood, and be helpful and responsive to any requests or questions the client asks them (not to mention saving them the time and cognitive load of needing to figure it all out for themselves in the first place). Clients continued to hire advisors who met this criteria for them, and to the extent that ostensibly-competitive technology altered the relationship at all, it was for the better – as advisors adopted spreadsheets, then financial planning software, robo portfolio management technology, and (increasingly today) AI, they were able to expedite or automate away many of the manual calculations, workflows, and analysis that had once taken up more of their time, allowing them to focus more on clients' needs and do deeper and more comprehensive planning, effectively increasing the value and quality of their services thanks to the technology. Clients rarely if ever noticed the changes in the technology itself, because the advisor's process for making rebalancing trades or running Monte Carlo simulations wasn't why they hired the advisor in the first place (and often occurred behind the scenes anyway).

However, there is likely at least theoretically a line at which technology could start to fundamentally alter the client-advisor relationship and undermine the value that the advisor provides. For example, if an advisor exposes sensitive client information to a software provider that sells or misuses the data, or has it stolen due to lack of security protocols, that might cause a breach in the trust that the client places in the advisor to safeguard their private information. But at a more fundamental level, if a piece of technology turns out to get in the way of the underlying reason that the client has hired them in the first place – again, to be a human who listens to the client, makes the best recommendation for their needs, and is responsive and helpful with requests and questions – clients might start to become wary of that technology and any advisors who use it. Or stated more simply, clients hire advisors to be their advisors, not to be the person who just enters their information into AI and get the output that the client could have typed in and read the responses from themselves.

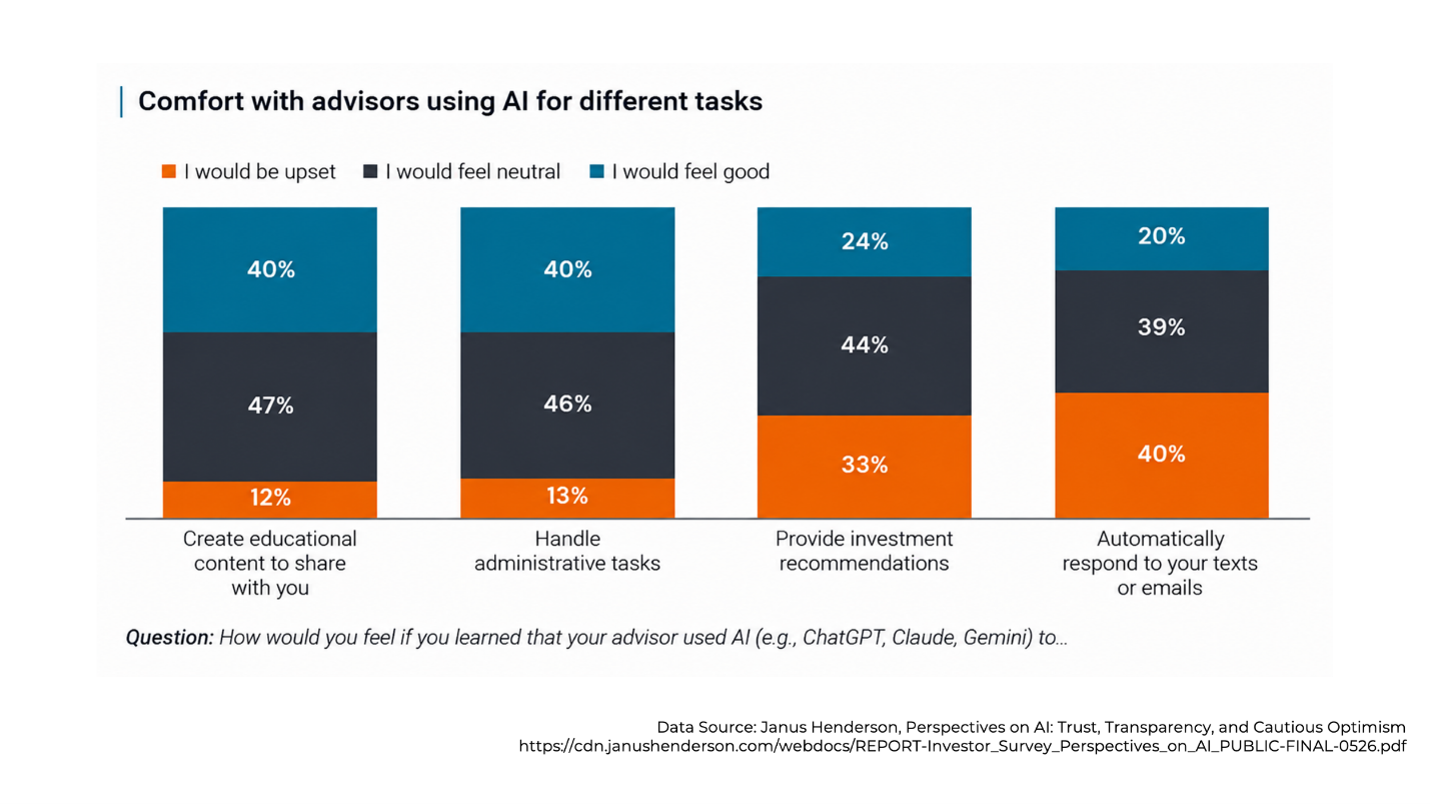

In this context, it's notable to see the results of a new survey by the asset manager Janus Henderson of 1,000 affluent and high-net-worth investors on their attitudes towards the use of AI in finance and investing – both their own personal use and that of advisors. On a whole, the survey found that most clients feel fine about advisors using AI across a variety of uses – for example, 40% responded that they would feel good about their advisor using AI to create and share educational content or to handle administrative tasks, and only 12%-13% responded that they would be upset by it. But by contrast, only 24% of clients responded that they would feel good about their advisor using AI to provide investment recommendations, while 33% would be upset by it. And only 20% of clients would feel good about their advisor using AI to automatically respond to texts or emails, while 40% would be upset by it.

Furthermore, while most investors responded as feeling good to neutral about advisors' use of AI in most areas, a full 80% responded that they would be upset if they learned that their advisor had used AI without disclosing it to them.

So while clients appear to have no particular problem with their advisors using AI per se, there are two big caveats. One is that what the advisor uses AI for matters more than the use of AI alone: clients are much more likely to accept AI when it's used for generalized educational content than for specific recommendations, and are similarly much more favorable towards advisors using AI for behind-the-scenes administrative tasks than for actual interaction with the client, echoing the theme that clients expect human service and human expertise when hiring a human advisor. And second, no matter what the advisor actually uses AI for, clients want to know that the advisor is using it, even if they take no issue with the use of AI itself.

At a high level, these new findings reinforce the idea that, like many technological developments before it, AI is no particular threat to advisors – and despite the anxiety on the advisor side over whether or not to use AI, the reality is that apparently clients won't really register its use anyway, as long as it doesn't intrude on the fundamental client-advisor relationship. If an advisor uses AI to write a blog post or client newsletter or to automate some manual back-office tasks, it won't matter much to existing clients and may even be a net benefit if it allows the advisor to better educate and get deeper into their client relationships. And there's no reason for advisors to hide their use of AI in these areas – and it would seem that it's much better to be transparent and proactive in disclosing when and how the advisor uses AI for these purposes.

However, the survey does also begin to give a sense of where the line really might be where AI starts to encroach on the client-advisor relationship. While the survey asked specifically about AI-generated investment recommendations, the increased client wariness of using AI to provide recommendations presumably extends to financial planning recommendations as well. Which is notable given the recent emergence of tools that use AI to “surface” recommendations based on client data, from Conquest Planning to FP Alpha to Altruist's Hazel tax planning tool (among many others). If clients turn to financial advisors specifically because they're too wary of trusting AI to give them sound recommendations, how will they feel about their advisors using their own AI tools to do the same thing?

And the other big line in the sand is on using AI to communicate with clients. Again, clients hire advisors specifically to be a human who will listen to them, give them the best recommendation for their needs, and be helpful and responsive to questions and requests. While AI might help with the very last part – being responsive – it clearly matters more to clients that they're hearing from the advisor themselves than that they simply get a fast reply. Which has its own implications for AI-powered communications tools for clients and prospects, from AI “receptionists” and automated texting features such as offered by CurrentClient to AI-generated prospect outreach offered by FINNY. In a world where it's feeling increasingly difficult to interact with a human in any customer service context, how will clients react if they feel they can't be certain that the 'person' who is writing or texting them from the advisor's account is actually the advisor?

The bottom line is that just like spreadsheets, financial planning software, and robo-advisors before it, AI is just a tool – albeit a far more powerful one with a much broader range of potential uses. When used to expedite or automate tasks that get in the way of the client-advisor relationship, it can be a net positive if it allows the advisor to focus more on the relationship parts. But when it's used to expedite or automate away the very human-service parts of the client relationship itself, that's when clients may start to notice and become wary (and doubly so if the advisor tries to pass it off as themselves without disclosing that they're using AI). Which means while there's always a temptation to get more efficient and use AI to build 'personalization at scale', there's only so much that real personalization can scale before the client starts to wonder if they're really interacting with the human they hired.

This article first appeared on the Nerd’s Eye View at Kitces.com at https://kitc.es/advisortech-june2026, and has been reprinted here with permission.

For years, large firms have been facing penalties and questions from regulators over interest rates for clients’ cash accounts.

Market volatility can be stressful, but it also represents opportunity for advisors and their clients.

After years of mixed signals and shifting timelines from Jamie Dimon, Wall Street sources suggest the race to lead JPMorgan Chase has entered its decisive stretch.

Advisors and broker-dealers adjusting to the March 2026 threshold change face bigger challenges around back-end monitoring than the new dollar limit itself.

Wealth management firm has seen an aggressive period of growth in the past year.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.