Jump to Winners | Jump to Methodology

Meet some of the best female financial advisors in the US – the women managing hundreds of millions of dollars, navigating clients through market chaos and personal loss, and still fighting for a seat at the table. InvestmentNews’ $100M Club: Top Female Advisors 2026 honorees reveal what it truly takes.

On any given day, financial advisors across America are talking someone off a ledge built from fear – fear of outliving savings, of market swings triggered by a presidential tweet, and of what happens to a lifetime of work when the person who managed it for 30 years retires. In an industry that has long been defined by the white-haired men who shaped it, that voice of calm reason is increasingly female.

InvestmentNews has identified some of the top financial advisors in the US through its $100M Club – a distinction awarded to female advisors who individually manage at least $100 million. This year, 108 women received that recognition, drawn from a competitive field of nominees, each verified by their firm’s compliance department and selected solely on the basis of assets under management (AUM) reported between January 1 and December 31, 2025. No fees were required to nominate, and no marketing relationship influenced the selection.

Behind those numbers lies a more complicated story – one about an industry still grappling with its own demographics, a wealth landscape on the verge of a seismic shift, and the women quietly building practices that may well define the next chapter of American financial life.

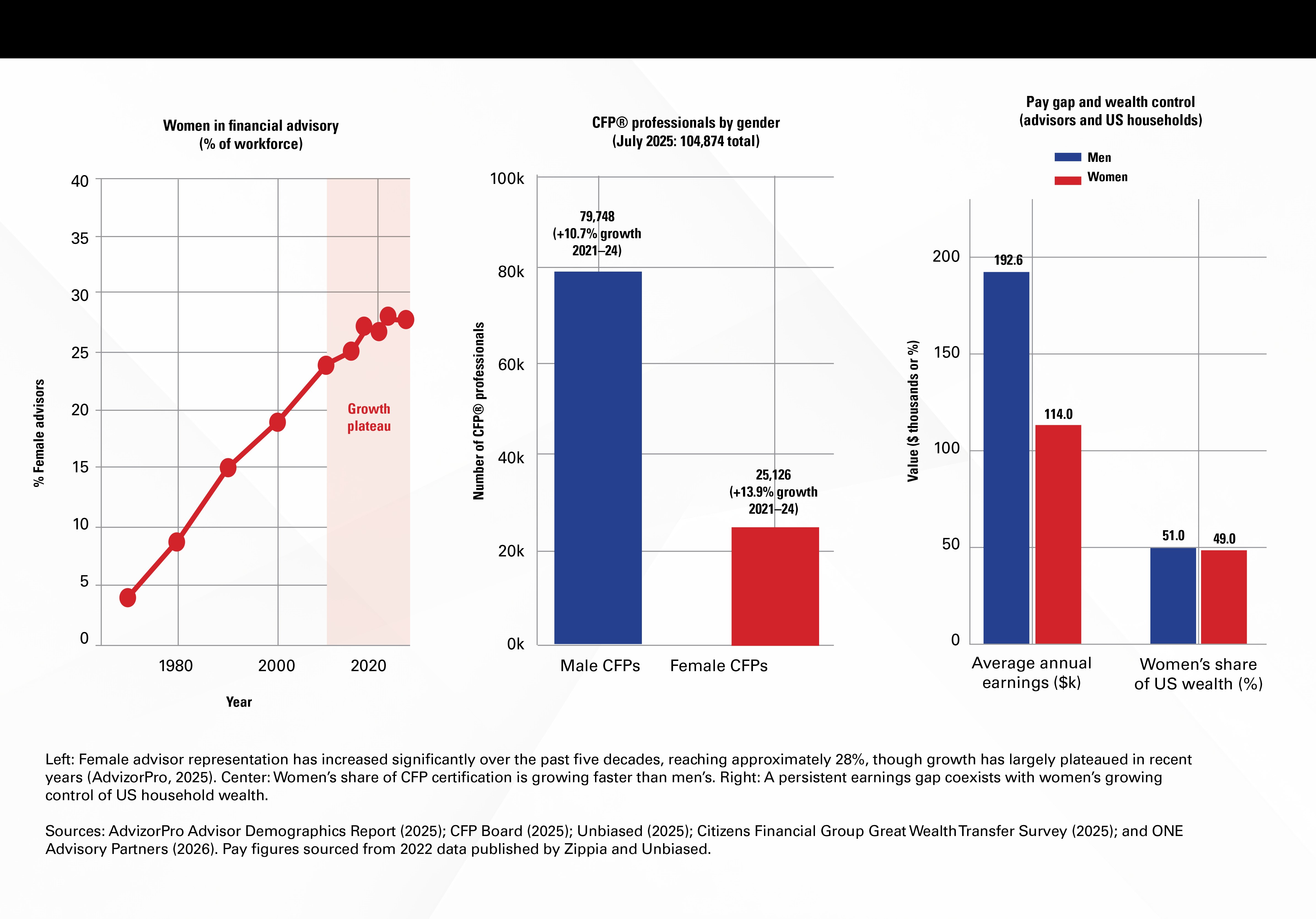

The numbers are unambiguous. Women represent approximately 24 percent of the nation’s financial advisors – a figure that has not only stalled but also edged slightly backward from the high-20s range seen in the 2010s, despite sustained efforts to improve it. Among Certified Financial Planner professionals – the industry’s most recognized credential – women make up 23.8 percent as of December 2025, according to the CFP Board. The advisory workforce remains, as one industry analysis put it, a profession still plateauing in its diversity gains.

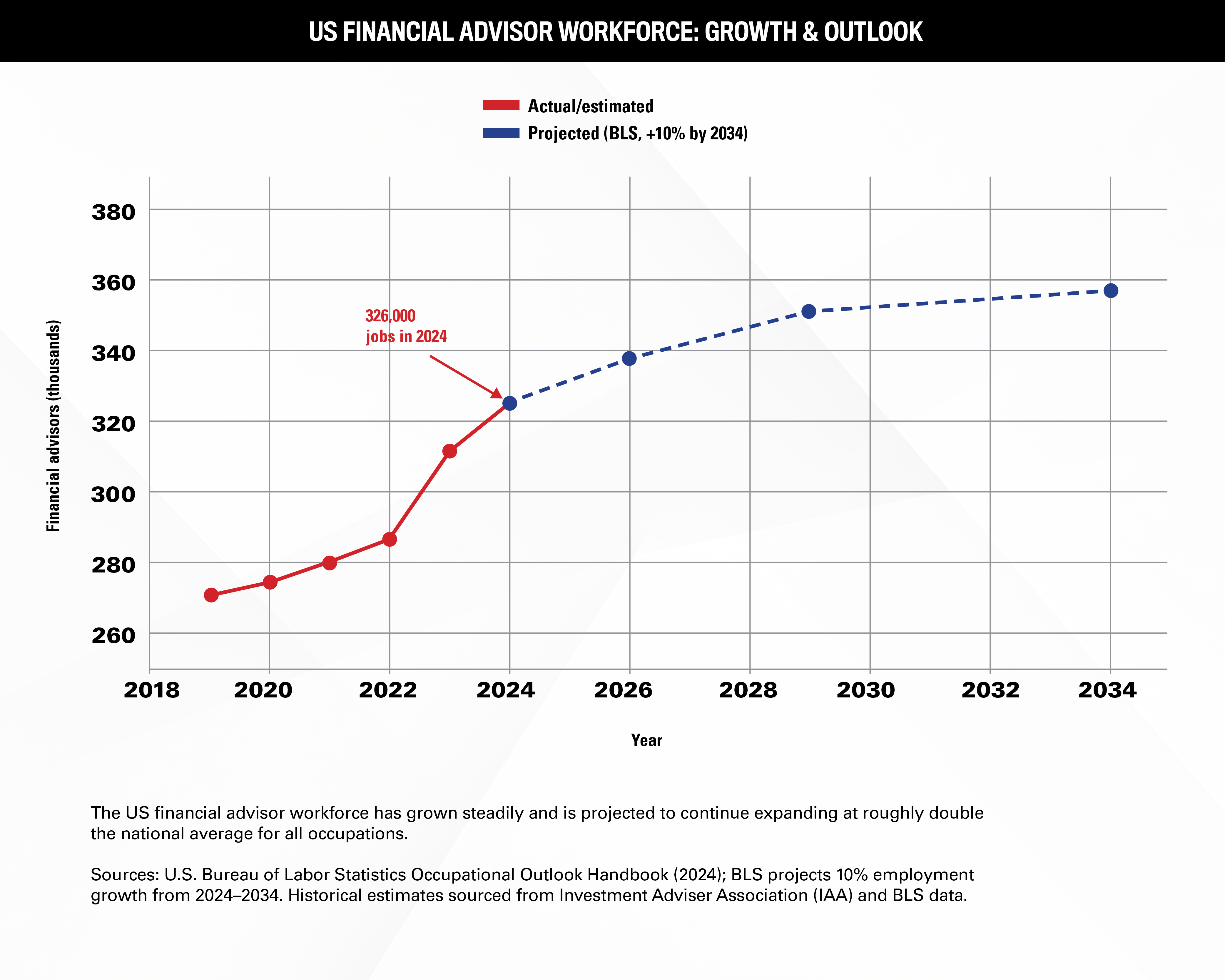

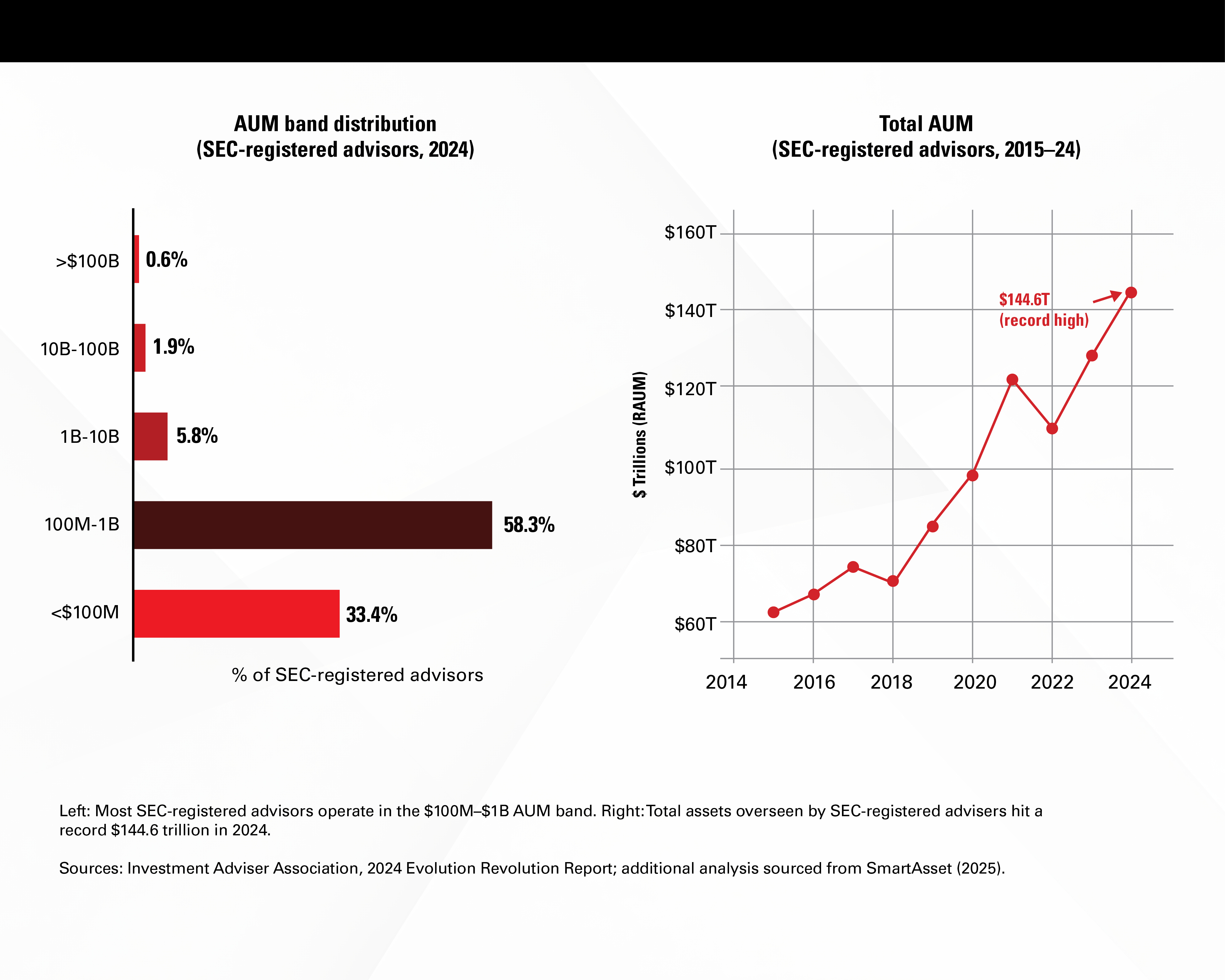

Yet step back, and the broader industry picture is one of remarkable expansion. The US had approximately 326,000 personal financial advisor jobs in 2024 up from around 271,000 in 2019, according to the Bureau of Labor Statistics. The agency projects a further 10 percent employment growth through 2034, adding roughly 24,100 new openings annually. Meanwhile, SEC-registered investment advisers now oversee a record $144.6 trillion in assets – a 12.6 percent increase from 2023 – according to the Investment Adviser Association’s 2025 data. The number of clients also reached a record 68.4 million.

The industry’s structure remains heavily dominated by smaller operators. According to the Investment Adviser Association’s 2025 data, 58.3 percent of all SEC-registered advisers manage between $100 million and $1 billion in assets – the same range that includes this year’s $100M Club honorees. Nearly 88 percent have fewer than 50 employees. Yet it is the top tier that controls most of the assets: the 207 largest firms alone manage 66.1 percent of all AUM. The $100 million threshold, in other words, marks a meaningful professional milestone but not an elite scale – it is where most of the profession actually lives.

Between the 1970s and the 2010s, female representation in the profession climbed steadily, from around 4 percent to roughly 28 percent. Since then, the share has slipped back to approximately 24 percent – a decline that reflects structural barriers still embedded in how the profession recruits, promotes, and retains women.

There is an encouraging counterpoint in the numbers, however. Between 2021 and 2024, the number of women earning CFP certification grew by 13.9 percent – outpacing the 10.7 percent growth rate for men, according to the CFP Board. Meanwhile, nearly one in four RIA firms (23.5 percent) has at least one female owner or executive, based on 2025 data from AdvizorPro. Among advisors with less than 10 years of experience, women now represent nearly 30 percent of the workforce, suggesting a younger generation entering the profession is more evenly balanced than the industry overall.

Yet the ground beneath the profession is shifting. Of the estimated $124 trillion in assets expected to change hands in the US between now and 2048, a significant portion will first pass to surviving spouses – 95 percent of whom are projected to be women, according to Cerulli Associates’ June 2025 data. By 2030, women are expected to control $34 trillion in investible assets, up from approximately $11 trillion in 2020 – nearly triple the amount they held at the start of the decade, according to research from McKinsey & Company and Citizens Bank published in February 2025. Whoever earns the trust of those women will help shape the next era of wealth management.

Avani Ramnani, managing director at Francis Financial in New York and a respected voice on gender equity in the profession, sees the moment as both urgent and promising. “Barriers still exist, though they feel more structural and less overt,” she says. “The pipeline skews male, and there remains a very high emphasis on sales rather than client development.” Women, she argues, still need sponsorship – not merely mentorship – and firms that have built genuinely diverse leadership are beginning to see the commercial logic of that investment.

Francis Financial itself is led by an all-female leadership team, a fact Ramnani cites with visible pride. “That has organically allowed more female advisors to be interested in joining our team, and from there we work very diligently to support their career paths,” she says.

For Ramnani, the $100 million threshold is meaningful but incomplete as a measure of impact. “Some of the most impactful work being done by female advisors is with clients who are building wealth for the first time, navigating major life transitions, or working with communities that historically have had little access to sophisticated financial guidance,” she adds. “That work doesn’t always show up in a $100M number, but it’s exactly the kind of practice that will matter most as the wealth landscape shifts over the next decade.”

How would you define a “Top Female Advisor” in 2026? Are there still barriers?

“A top female advisor starts with the same qualities as any excellent advisor: deep trust, fiduciary advice, and sound judgment under pressure. But the recognition still matters because women remain underrepresented. Women advisors tend to serve higher numbers of female clients, who have distinct planning needs around longevity, caregiving priorities, and career transitions. That’s a specialized skill set, and increasingly, that’s where the need and opportunities are.”

How would you characterize $100M+ AUM for female advisors?

“It is a major milestone for any advisor. In my experience, for women, it often reflects something deeper. AUM tells you the size of a practice, not the depth of its impact. Some of the most impactful work being done by female advisors is with clients who are building wealth for the first time or working with communities that historically have had little access to sophisticated financial guidance. That work doesn’t always show up in a $100M number, but it’s exactly the kind of practice that will matter most as the wealth landscape shifts.”

What steps would create better opportunities, especially at senior levels?

“Creating better opportunities at senior levels requires three things: intentional sponsorship, transparent progression criteria, and client access. I am so proud of our firm, which has an all-female leadership team and focuses on serving women. That has organically allowed more female advisors to be interested in joining our team, and from there, we work very diligently to support their career paths – beyond just mentorship.”

Kristen Gratton is a financial advisor based in western Pennsylvania who manages over $100 million in assets under management and specializes in tax planning and retirement income strategies for early retirees. She is a 2026 IN’s $100M Club honoree and founder of Gratton & Kerr Financial Group.

It is 5:30 in the morning, and Kristen Gratton is already awake. She has just returned from an overnight flight home from a retirement income planning conference in Orlando – the kind of conference that most established advisors might consider optional, a perk of seniority rather than a professional obligation. For Gratton, it is simply Tuesday.

“I want to be the best advisor I can be,” she says plainly, describing the relentless educational drive that has come to define her practice. “I’ve got to know what’s new and what’s changing.”

Gratton built Gratton & Kerr Financial Group from the ground up, eventually hiring her husband as part of the team five years in. She leads a staff of three financial advisors and two administrative professionals, and her days are now split between client work and the less glamorous demands of running a growing firm.

“It’s hard to lead people where you haven’t been,” she says. “When you’re doing it yourself, you know this is really hard to run a business, so it gives you more perspective on the challenges your clients are facing too.”

Over the past several years, Gratton has identified what she sees as the most underserved dimension of the advisory relationship: tax planning. Not tax preparation – she is clear that her firm does not file returns – but the kind of forward-looking tax strategy that most clients assume their advisors are already doing, and most are not. Her approach now involves sitting down with clients’ accountants, analyzing tax returns alongside investment strategy, and asking what she calls the fundamental question: how do we pay the least amount of lifetime taxes?

Her niche has crystallized around pre-retirees – typically clients between 45 and 65 who want to retire early, before Medicare eligibility. It is a demographic defined by two overlapping anxieties: health insurance costs and the fear of running out of money. Gratton has made herself a specialist in both.

On the question of gender in her profession, Gratton is candid rather than bitter. At a conference recently, she was assumed to be administrative staff. Her husband, present as her business partner, had been congratulated on her behalf. “I feel like I have to prove myself a little,” she says. “Maybe it’s part of my drive – I’ve got to be the best. I’ve got to learn. I’ve got to know.” Her 16-year-old daughter, she adds, recently corrected a classmate who assumed her father was the breadwinner. “She’s like, ‘Actually, no, my mom’s the money maker.’ That makes me really proud.”

You’ve built both a client practice and a business simultaneously. How do those two roles relate?

“They work together, but it’s definitely different challenges. Running your own business versus meeting with clients – they’re very different. But owning a business gives me additional insight when I’m working on my own – to realize the challenges my business-owner clients are facing.”

You recently returned from an overnight conference. What drives that level of continued education?

“I like to learn. I want to be the best advisor I can be. Things can adjust – 20 years ago, there were only mutual funds. Now there are ETFs, direct indexing, and structured notes. If you don’t keep up with it, you’re not doing the best thing for your clients.

As a woman in a male-dominated field, how has that shaped your approach?

“I think it can be a huge benefit – we have the ability to make clients comfortable. But it has also been a challenge. Maybe that’s part of my drive to keep learning, keep growing.”

Lauree Harrison is a senior financial advisor based in Seattle, WA, who manages over $100 million in assets under management and specializes in serving women, millennial investors, and clients navigating major life transitions. She is a 2026 IN’s $100M Club honoree and owner of Cascade Guided Wealth.

Lauree Harrison describes her competitive edge with a single, unexpected word: superpower. As a female advisor in Seattle – a city she notes is demographically and politically distinct, where community ties matter – she has come to see her gender not as an obstacle to navigate but as a lens that makes certain relationships possible.

“The relationships that we do have are stickier,” she says, “because the people who seek us out want the benefit of having a female financial advisor.” Harrison works with women navigating widowhood, divorce, and major career transitions – and with male clients who actively sought a female advisor because they wanted someone who would take time to explain without the jargon.

Harrison came to finance through an unconventional route. She found the profession through a job listing and built her way toward eventually owning her own firm. Along the way, she acquired two books of business from female advisors in Seattle who retired and specifically sought a like-minded successor.

She grew up, as she puts it, with no money and a lot of money stress. That background, she believes, gives her a kind of credibility that clients from similar circumstances find disarming. “Our industry has an upper-crust sort of reputation,” she says. “They all think: you came from money; you went to a great school. It’s like, no, I had student loans. I fought to be here.”

Her view of growth is notably unsentimental for an industry that often equates scale with success. She has turned down acquisition opportunities that did not fit her client profile. She has no interest in managing 20 advisors if it means losing direct contact with the clients she serves.

What defines success for Harrison is simpler and harder to quantify. She describes being the second call a widow made after her husband died – and then helping that widow notify the attorney, the CPA, and the other advisors in her financial life. “It feels nice to be relied upon and just to be that center of trust,” she says.

She also offers an observation about the behind-the-scenes reality of advisory work that rarely makes profiles. “Running a really good business in our industry is hugely about the non-sexy piece – the administrative work,” she says. “We are really, really persistent about making sure every single piece of paperwork is processed correctly, on time, and followed up on.” It is, she says, a large part of why her clients stay.

You’ve called being a female advisor a “superpower.” What do you mean by that?

“The relationships we have are stickier because the people who seek us out specifically want the benefit of having a female advisor. I work with women navigating widowhood and divorce – it’s a natural fit. I’ve also had male clients say they specifically wanted a female advisor because they didn’t want someone to talk over their heads. They just wanted a conversation.”

You grew up without financial security. How does that shape how you work?

“Clients assume you came from money. It’s like, no, I had student loans. I fought to be here. I think that puts them at ease – knowing I understand how much financial security means, because I fought for my own.”

How do you think about growth for your firm?

“I’ll be flexible and open to opportunities if they seem right. But I’ve turned down acquisitions that just weren’t the right client profile. I still really, really want to talk to my clients. I won’t give that up. A lot of the advisors I admire are having the same debate: why grow at all costs?”

Carol Mulcahy is a senior wealth advisor based in Florida with over 40 years of experience in financial services, managing over $100 million in assets under management and specializing in elder care planning and estate transition for older clients. She is a 2026 IN’s $100M Club honoree and partner at Destiny Wealth.

Carol Mulcahy has been doing this since 1985. She has navigated the 1987 crash – on her birthday, as it happens – the dot-com collapse, the financial crisis of 2008, and the turbulence of 2021. She has sat with families as they buried parents, untangled estates, and discovered that the beneficiary designations they never updated had redirected decades of savings to an ex-spouse. She has been, as her former institutional colleagues used to call her, the priest.

“They would send me out,” she recalls with a laugh, “and people would just tell me everything.”

Mulcahy grew up in Boston in a construction family – the daughter of a household where eighteen-wheelers parked outside and life-sized Tonka trucks were part of the scenery. She stumbled into finance in the early 80s, navigated the informal hierarchies of an industry where, as she puts it, Irish Catholics did not always fit with the Boston Brahmin set, and accumulated, across four decades, a kind of wisdom that cannot be taught.

She is based now in Florida, where she trades Boston winters for perpetual heat and serves a predominantly older client base. During the pandemic, when the rest of the financial industry retreated to home offices, Mulcahy was in the building every day.

“People need to know that there was still someone managing your money,” she says. “They just wanted to know someone was there.”

Her core strategy, which she calls the Retirement Distribution System, divides client assets into three pools based on time horizon: money needed in the next 10 years, held conservatively; money in the 10- to 20-year range, invested for growth; and a legacy pool designed to grow over decades. It is an approach built explicitly for the kind of volatility that has defined markets in recent years.

Much of Mulcahy’s practice is now focused on elder care planning – guiding Florida clients and their families through the financial and emotional complexity of aging. She works with CPAs, attorneys, and other advisors to build coordinated plans, catching the kinds of errors – outdated beneficiary designations and missed charitable distribution opportunities – that can otherwise cost families years of careful planning.

She does this with a deliberate neutrality she traces back to something close to a philosophy. “I’m not your Jiminy Cricket,” she says. “You can tell me what you want to give. Whether I like it or not is irrelevant. This is your money.”

After four decades, Mulcahy is finding, for the first time, a measure of balance. She works from home one day a week, a modest adjustment she describes as significant. She is still motivated by the same thing that drove her through a decade in which she raised a son alone, cared for aging parents, and held down a major institutional client while going back to school at night. “I look back now and say, how the heck did you do it?” she says. “But sinking was not an option.”

You’ve been in this industry since 1985. What has changed most in how you serve clients?

“The industry is completely different now than it was then. When I started, I didn’t know a bear from a bull. What I’ve learned is that every family has a unique situation. I’ve gone through 1987, the tech bubble, 2008, and 2021 – you go through all of this, and you realize we’re going to come out eventually. The key is knowing how to get through it in the smoothest, least complicated way possible.”

How do you think about helping clients navigate uncertainty?

“I use a three-pool strategy. I keep the money clients will need for the next 10 years pretty safe, so no matter what’s happening – geopolitically, tariffs, whatever – it’s not money they need right now. We’re not just setting it and getting it and hoping for the best. When sectors change, our investment committee goes and finds the next opportunity.”

What’s the most important thing you do for clients that they might not even realize?

“The beneficiary works. A named beneficiary supersedes a will and a trust. Once, I saw a former spouse get everything because no one had updated the paperwork, and the current spouse and children got nothing. So every year I go through a full review – not just what we have here, but everything. Do you have a 401(k) elsewhere? A life insurance policy? I want to see the whole picture.”

There is a common thread running through the careers of these honorees, and it is not the AUM, though those are impressive. It is something harder to measure: a particular quality of attention. The ability to read the room – to hear what is being said underneath what is being said – and to show up not just as a technically competent manager of money but also as someone clients turn to when life happens.

The industry is changing, slowly and unevenly. The CFP Board’s Accelerate & WIN initiative, launched in March 2025, represents a structured effort to build a more diverse pipeline – reaching into high schools, colleges, and career-change programs to find the women who might not have considered finance a viable path. The numbers, at roughly 24 percent female CFP representation, suggest the work is not finished.

But the women being recognized this year by IN – 108 of them, managing assets that span the full range of American financial life, serving retirees in Florida and millennials in Seattle – are not waiting for the pipeline to fix itself. They are building practices, acquiring books of business from one another, mentoring the next wave, and making the case through results that the thing their industry has too often undervalued is precisely the thing their clients most need.

As Ramnani puts it, the shifting demographics of wealth are finally forcing the industry’s hand. “Shifting client demographics are steering advisory firms to make this transition,” she says. Whether the firms follow the clients – or the clients force the issue themselves – the direction, at least, is clear.

What is the InvestmentNews $100M Club?

The IN’s $100M Club is an annual recognition program that identifies top female financial advisors in the US who individually manage at least $100 million in assets under management. Honorees are nominated by advisors, industry professionals, and clients, and all submitted information is verified by the nominee firm’s compliance department before inclusion. The award is based solely on AUM and does not measure investment performance or client outcomes.

How many female financial advisors are there in the US?

As of 2025, women represent approximately 24 percent of the roughly 326,000 personal financial advisors employed in the United States, according to July 2025 data from AdvizorPro, which analyzed more than 776,000 securities-licensed advisors. Among Certified Financial Planner (CFP) professionals specifically, women account for 23.8 percent of the 107,529 total CFP professionals – a share that has doubled over the past decade but has largely plateaued since around 2010, according to December 2025 data from the CFP Board.

What does it take to be recognized as a top female financial advisor in the US?

To be eligible for the IN’s $100M Club, a female financial advisor must individually manage a minimum of $100 million in assets under management. All nominee data must be verified by the advisor’s firm’s compliance department. Beyond the threshold, the honorees profiled in this report share several qualities: a commitment to continuous education, deep client relationships built on trust, a holistic approach to financial planning that includes tax strategy and estate planning, and the ability to navigate clients through financial and personal complexity.

Which women were recognized as top financial advisors by IN in 2026?

IN recognized 108 women as part of its 2026 $100M Club. Among those profiled in this report are Kristen Gratton of Gratton & Kerr Financial Group (Mars, PA), a specialist in tax planning and early retirement strategies; Lauree Harrison of Cascade Guided Wealth (Seattle, WA), who focuses on women investors and millennial clients; and Carol Mulcahy of Destiny Wealth Partners (Tavares, FL), a 40-year veteran specializing in elder care planning and estate transitions.

Why are female financial advisors important in the US wealth management industry?

Female financial advisors play an increasingly critical role as the demographics of US wealth shift. By 2030, women are projected to control $34 trillion in investible assets – up from approximately $11 trillion in 2020, nearly triple the amount they held at the start of the decade, according to 2025 research from McKinsey & Company and Citizens Bank. Research shows that female advisors often develop deeper client relationships, particularly with women navigating major life transitions such as divorce, widowhood, or inheritance. Yet women remain significantly underrepresented in the profession, making recognition programs such as IN’s $100M Club: Top Female Advisors an important signal of progress.

This award recognizes female financial advisors who demonstrate significant scale in their advisory practices as measured by assets under management (AUM). The list highlights advisors managing substantial client assets during the evaluation period.

To compile the annual list, InvestmentNews solicited nominations from advisors, industry professionals, and clients.

Eligibility requirements included:

Nominees must be female financial advisors.

Nominees must individually manage at least $100 million in assets under management (AUM).

All submitted information regarding nominees was required to be verified by the nominee firm’s compliance department before being accepted for consideration.

Population of nominees: 340

Number of recipients: 108

Percentage of nominees receiving award: 31.76%

Award is based on: Assets Under Management (AUM)

The final list was determined based on each eligible advisor’s individual AUM reported between January 1 and December 31, 2025.

Client testimonials or feedback

Investment performance history

Other factors unrelated to AUM levels

Only nominees meeting the minimum AUM threshold and completing the compliance verification process were considered for inclusion.

No fees were required for nomination or consideration for this award.

Any marketing or promotional opportunities related to the award are separate from the editorial selection process and do not influence award results.

This award reflects the stated methodology and criteria and is based on reported assets under management during the evaluation period. It does not measure investment performance, guarantee client outcomes, or represent a ranking of all financial professionals.

All nominee information must be reviewed and verified by the nominee firm’s compliance department before being accepted for consideration or publication.