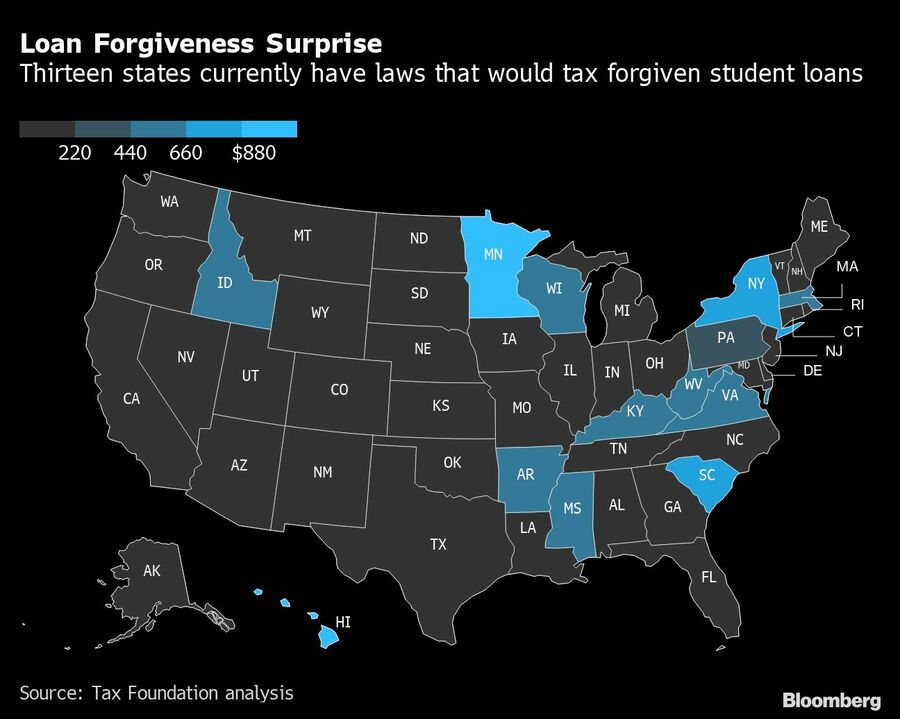

Residents of New York, Virginia and 11 other states could end up with a surprise tax hit of hundreds of dollars next year on forgiven student loans.

President Joe Biden’s announcement that the government would forgive some student debt for individuals earning less than $125,000 was welcome news to many carrying large loan balances. But 13 states have laws that treat this forgiven debt as income, meaning that it’s subject to state levies on earnings.

That means that taxpayers in those states who have $10,000 in debt forgiven could end up owing a few hundred extra dollars -- or in Hawaii more than $1,000 -- on their state tax returns next April.

Student borrowers who received a Pell Grant as an undergraduate, which the White House estimates is about 60% of borrowers, can get up to $20,000 in loans forgiven. Individuals with the full $20,000 cancelled would pay double the tax amounts.

The federal tax code also generally treats forgiven debt as income, but in 2021, Congress included in the American Rescue Plan a measure that would temporarily exempt canceled student debt from taxation.

It’s possible that some of the 13 states where the laws would tax these forgiven student loans will revise their rules before the taxes are due next spring. Depending on the state, that could come in the form of an administrative change from the governor or state tax department, or may require the state legislature to pass a new law.

Jared Walczak, a vice president at the Tax Foundation focusing on tax policy, calculated the maximum tax hit for $10,000 in forgiven loans in various states. His figures are based on the highest tax rate filers who qualify for loan forgiveness are likely to pay in their state. His tabulations found that residents of Pennsylvania are likely to pay the lowest amount, with Hawaiians paying the most.

| State | Maximum Likely Tax Liability |

|---|---|

| Arkansas | $550 |

| Hawaii | $1,100 |

| Idaho | $600 |

| Kentucky | $500 |

| Massachusetts | $500 |

| Minnesota | $985 |

| Mississippi | $500 |

| New York | $685 |

| Pennsylvania | $307 |

| South Carolina | $700 |

| Virginia | $575 |

| West Virginia | $650 |

| Wisconsin | $530 |

Walczak said that states will need to act with “some urgency” if they want to change how their tax laws treat student loans in light of Biden’s changes. He added that it isn’t likely to matter whether the state is led by Republicans or Democrats. Since the change has already been made at the federal level, there will be some pressure on states to reduce tax burdens for their residents, he said.

“It’s time for an economic reset,” wrote the California governor, in a post on X.

Masterworks was launched in 2017 but its RIA, Masterworks Advisers, is just three years old.

One 2017 form, no broker license, and a $42 million gap they say surfaced on a webinar.

Fewer than half of Americans in their peak earning years feel on track for retirement, while many say limited financial knowledge and access to professional guidance are holding them back.

Meanwhile, Wells Fargo hauled advisors overseeing $825 million in the West Coast, while Wedbush has welcomed a seasoned professional from Stifel in California.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.