Let’s start with the obvious: We’re in a low-interest-rate environment, and according to the Fed, we’re going to be here for a number of years. With 10-year Treasuries yielding about 0.75%, building an efficient retirement income portfolio is harder than ever.

Typically, I would place income annuities into the risk management category rather than the investment category. No one ever asks what the internal rate of return, or IRR, is on a liability policy or a homeowner’s policy. They buy those policies to protect against risk. Similarly, income annuities are designed to eliminate, or at least reduce, both longevity risk and sequence-of-returns risk. However, in this interest rate environment, income annuities find themselves in the unique position of also being a competitive investment tool.

People typically believe that the lower interest rates go, the worse annuities are as investments. When you lock in a lifetime income rate based on interest rates, why would you invest when rates are low? In fact, for years now, I’ve read that even some of the biggest annuity supporters have suggested people were best served by waiting for rates to rise before locking in any lifetime income guarantees.

Setting aside the fact that it could be a very long wait, it’s important to understand that interest rates aren’t the only factor in determining the income amount. In fact, when rates are this low, it isn’t even the main factor. The lower interest rates go, the more the return hinges on the mortality credits built into the pricing. Mortality credits are essentially the transfer of income payments at the insurance company level from policyholders who die early to those who live to or beyond their life expectancy.

One of the key benefits of adding a lifetime living benefit to an annuity is that it provides a known amount of income in the future no matter what happens to the value of initial purchase. Therefore an indexed annuity with a living benefit is essentially a liquid deferred income annuity. And as backwards as it may seem, it’s this very liquidity that often allows insurance companies to guarantee more future income with an indexed annuity than a deferred income annuity. When an insurance company issues a deferred income annuity, it must assume the policyholder will eventually start getting the income (unless they die). However, with an indexed annuity, the insurance company can assume that some of the policies will lapse before the income start date.

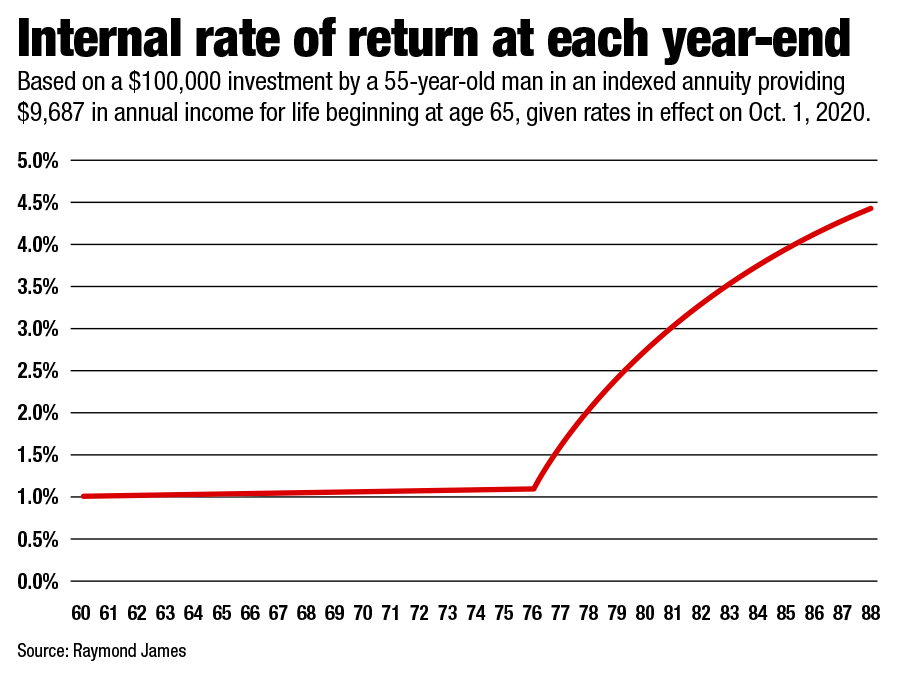

With this in mind, let’s take a look at a 55-year-old man who expects to begin taking income at age 65 using an indexed annuity with a living benefit. A popular indexed annuity would currently guarantee $9,687 in income for life beginning at age 65 based on a $100,000 investment. Given the current cap rates on indexed annuities of about 3.5%, I’ve conservatively assumed that the account value will grow on average by 1% per year, net of the living benefit rider fees.

Clearly, a 1% annual return will not get anyone excited, but the picture starts to change dramatically once the income starts paying out. Remember, since we are buying an annuity with a living benefit rather than an immediate annuity, the remaining account value is always available to the policyholder (or paid to the beneficiary if the owner dies).

Until the income starts paying out, the IRR on the annuity would obviously be just the 1% that we are assuming is credited to the account each year. However, with each and every $9,687 income payment, the IRR grows.

A 55-year-old man is expected to live to 83. Therefore, the expected IRR at the time of purchase is roughly 3.5%. However, a 65-year-old man is expected to live until 87. Therefore, assuming the client lives long enough to start the income, the expected IRR climbs to roughly 4.25%. And keep in mind, these life expectancies are based on the total U.S. population. Individuals with significant investible assets typically live three to five years longer than the overall average.

Yes, we are talking about a very long-term investment. It doesn’t get much longer than over one’s lifetime. But what other investment can provide principal protection, an income for life and an expected annual return of 4% or more? And don’t forget, by building a protected lifetime income stream into the retirement plan, you will have far more flexibility on how you invest the client’s other assets.

Annuities can serve as an attractive alternative to bonds or other fixed-income investments, especially in this rate environment. While we’ve made the comparison to other fixed-income solutions throughout this article, there are a few things to in mind before investing:

Scott Stolz is president of Raymond James Insurance Group and author of “Unlocking the Annuity Mystery: Practical Advice for Every Advisor.”

A new proposal could end the ban on promoting client reviews in states like California and Connecticut, giving state-registered advisors a level playing field with their SEC-registered peers.

Morningstar research data show improved retirement trajectories for self-directors and allocators placed in managed accounts.

Some in the industry say that more UBS financial advisors this year will be heading for the exits.

The Wall Street giant has blasted data middlemen as digital freeloaders, but tech firms and consumer advocates are pushing back.

Research reveals a 4% year-on-year increase in expenses that one in five Americans, including one-quarter of Gen Xers, say they have not planned for.

Orion's Tom Wilson on delivering coordinated, high-touch service in a world where returns alone no longer set you apart.

Barely a decade old, registered index-linked annuities have quickly surged in popularity, thanks to their unique blend of protection and growth potential—an appealing option for investors looking to chart a steadier course through today's choppy market waters, says Myles Lambert, Brighthouse Financial.