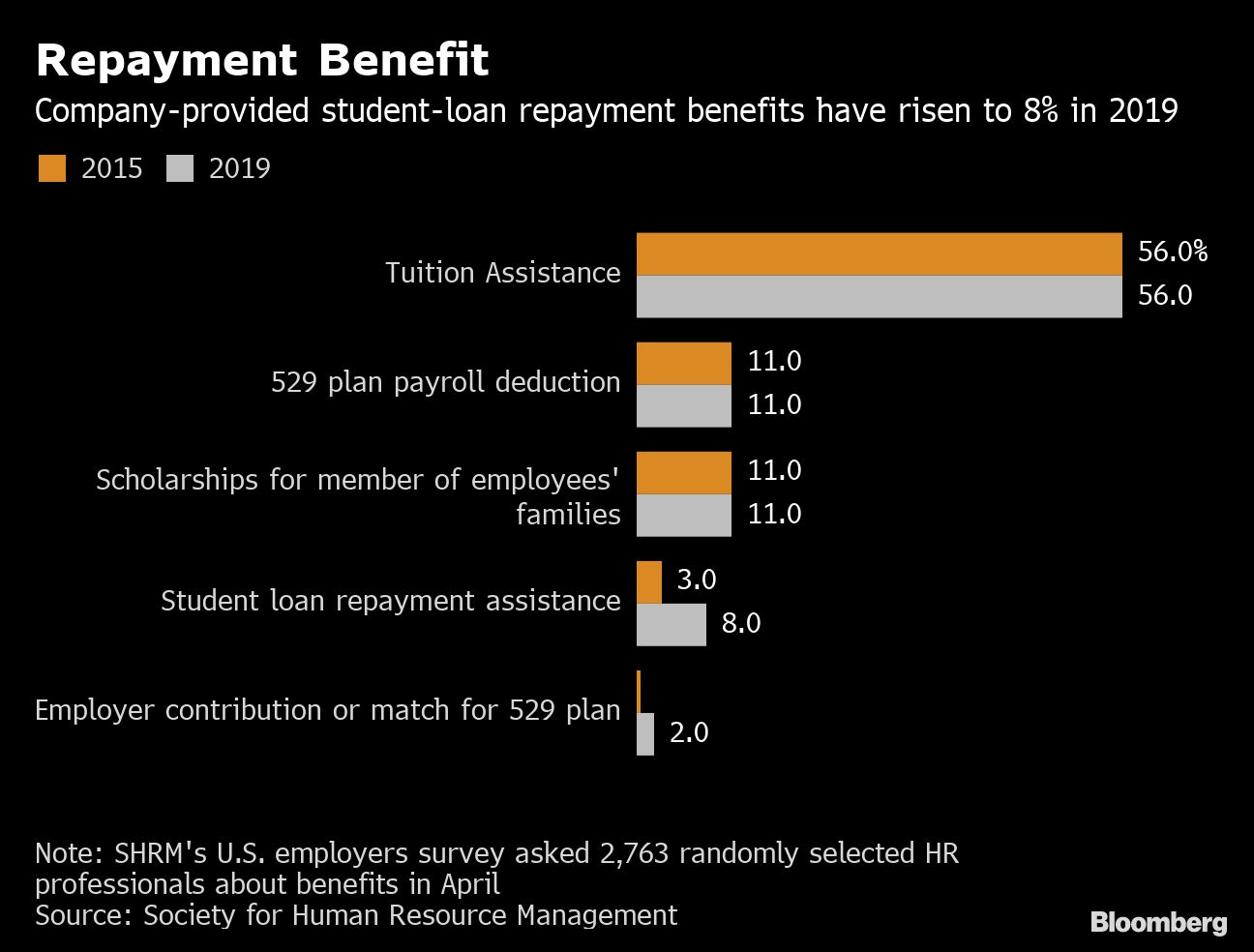

Another study by business adviser Willis Towers Watson found that 32% of firms are considering introducing a similar benefit by 2021.

"If you have a young demographic, offering benefits like student loan repayment could be the way to go," said Alex Alonso, chief knowledge officer for SHRM.

Pronounced competition for talent and the elevated debt burden for a generation of Americans making their way into the workforce are driving the change. Millennials make up more than half of Live Nation's U.S. labor force.

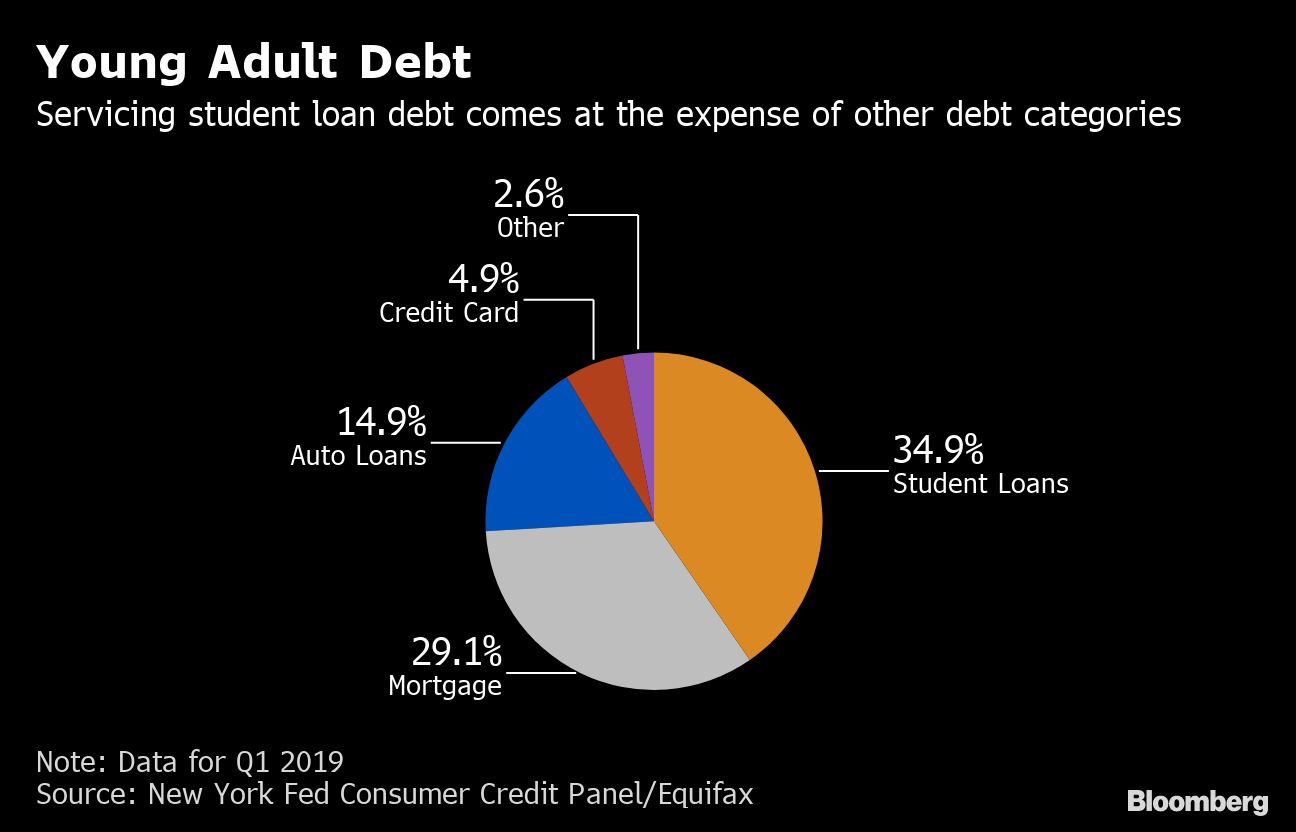

The balance on outstanding student loans reached $1.6 trillion at the end of the first quarter, and more than a quarter of that is held by people younger than 30. The effects reverberate through their social and economic lives, making it harder to start a family, buy a home or purchase big-ticket items, research shows.

Another study by business adviser Willis Towers Watson found that 32% of firms are considering introducing a similar benefit by 2021.

"If you have a young demographic, offering benefits like student loan repayment could be the way to go," said Alex Alonso, chief knowledge officer for SHRM.

Pronounced competition for talent and the elevated debt burden for a generation of Americans making their way into the workforce are driving the change. Millennials make up more than half of Live Nation's U.S. labor force.

The balance on outstanding student loans reached $1.6 trillion at the end of the first quarter, and more than a quarter of that is held by people younger than 30. The effects reverberate through their social and economic lives, making it harder to start a family, buy a home or purchase big-ticket items, research shows.

The federal government is considering giving companies a break for helping employees with their debt.

The Employer Participation in Repayment Act, introduced in the House and Senate in February, would provide tax relief to firms that do so. It has bipartisan sponsors, including Democratic presidential candidates Seth Moulton and Amy Klobuchar.

Other Democratic contenders, like Senators Bernie Sanders and Elizabeth Warren, have proposed more sweeping fixes that include writing off loans.

"Helping employees get out of debt faster is a win-win, both for the employee and for our productivity," said Katie Wandtke, director of human resources at Cybrary, a cyber-security firm based in College Park, Maryland.

It's not just smaller shops adopting the benefit. Larger companies, including professional services powerhouse PricewaterhouseCoopers, are catching on too.

(More: What advisers need to know about working with student loan debt)

Live Nation began offering the benefit in early 2017 and has helped employees save over $4 million. More than 80 of the company's workers have been able to completely pay off their loans, according to Live Nation.

The event organizer works with startup Tuition.io, which specializes in helping companies set up such programs and has clients including Fidelity Investments and Staples. There are other platforms in the market too, including Goodly, which works with Cybrary, and Gradifi, used by PwC since 2016.

Paying an extra $30 a month more than the minimum, like Ms. Read says she does with her employer's help, makes a difference.

For example, for a 10-year loan of $50,000 at 5%, it would save close to $1,000 in interest payments over the life of the loan – allowing the borrower to clear the slate eight months early.

"Jobs in the entertainment industry like this one, they're not high-paying jobs necessarily," said Ms. Read. "So this kind of helps offset that wage difference and it's really helpful for people like me."

The federal government is considering giving companies a break for helping employees with their debt.

The Employer Participation in Repayment Act, introduced in the House and Senate in February, would provide tax relief to firms that do so. It has bipartisan sponsors, including Democratic presidential candidates Seth Moulton and Amy Klobuchar.

Other Democratic contenders, like Senators Bernie Sanders and Elizabeth Warren, have proposed more sweeping fixes that include writing off loans.

"Helping employees get out of debt faster is a win-win, both for the employee and for our productivity," said Katie Wandtke, director of human resources at Cybrary, a cyber-security firm based in College Park, Maryland.

It's not just smaller shops adopting the benefit. Larger companies, including professional services powerhouse PricewaterhouseCoopers, are catching on too.

(More: What advisers need to know about working with student loan debt)

Live Nation began offering the benefit in early 2017 and has helped employees save over $4 million. More than 80 of the company's workers have been able to completely pay off their loans, according to Live Nation.

The event organizer works with startup Tuition.io, which specializes in helping companies set up such programs and has clients including Fidelity Investments and Staples. There are other platforms in the market too, including Goodly, which works with Cybrary, and Gradifi, used by PwC since 2016.

Paying an extra $30 a month more than the minimum, like Ms. Read says she does with her employer's help, makes a difference.

For example, for a 10-year loan of $50,000 at 5%, it would save close to $1,000 in interest payments over the life of the loan – allowing the borrower to clear the slate eight months early.

"Jobs in the entertainment industry like this one, they're not high-paying jobs necessarily," said Ms. Read. "So this kind of helps offset that wage difference and it's really helpful for people like me."

Commonwealth Financial joins a number of firm that have recently cut jobs.

A slow drip of disclosures, an executive exit, and a stock that fell hard before the suit landed

New research finds unpaid caregivers are more likely to struggle with debt, lower savings and diminished retirement confidence than non-caregivers.

Large broker-dealers and registered investment advisors have, since 2020, been developing or sticking to strategies and tactics to combat the pain of intense, short-term market volatility

Centaurus Financial touts its independence as a key selling point at a time when many firms are being swallowed up.

Northern Trust’s Ken Lassner shows advisors how to convert volatility into after-tax portfolio gains

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income