And that's optimistic. Social Security income is based on wages earned during one's working years. According to the GAO report, the median annual income of households with no retirement savings and no pension was $18,932 in 2013. That's a fraction of the median household income of $53,585 that year, according to the Census Bureau, which is likely to mean that those households' Social Security benefits will be well below average, too.

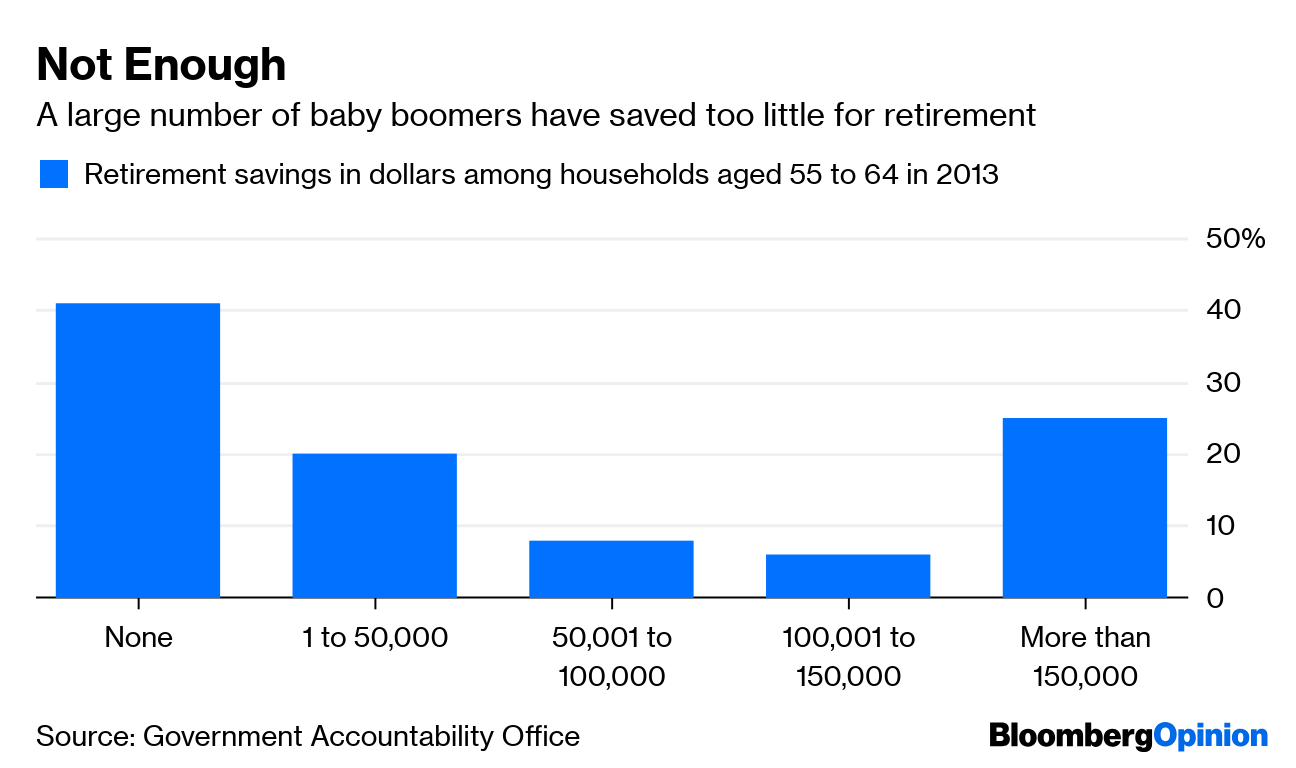

With that little income, those households are fortunate to save at all. According to the GAO, they had a median net worth of $34,760 and financial assets of just $1,000 in 2013. But even better-paid workers struggle to save because the median household income is well below the cost of living. Roughly three-quarters of households aged 55 to 64 had $150,000 or less in retirement savings in 2013. That isn't nearly enough, and unless wages rise, younger workers won't be any better prepared for retirement.

(More: Top reasons to file a tax extension)

Workers once had brighter retirement prospects, if not higher wages. What's changed is that over the last four decades, a growing number of employers replaced their pensions with 401(k) and other defined contribution plans, shifting the responsibility of saving for retirement to employees. According to the Employee Benefit Research Institute, 28% of private sector workers who participated in an employment-based retirement plan were enrolled in a traditional pension in 2014, down from 84% in 1979.

It's hard to blame employers. Pensions are difficult and costly to manage, as any number of underfunded corporate and government plans can attest. Workers also move jobs more often than they used to, so employers may not feel as responsible for their futures. But employers have no doubt saved a fortune by abandoning pensions, and given that real wages have hardly moved over the last four decades, there's little indication they passed those savings on to workers.

It wouldn't cost employers much, however, to give workers some retirement security again. By my calculation, it amounts to $2.64 an hour.

Here's how I get there: According to the Economic Policy Institute, the cost of living for a single person in, say, the Chicago metro area, is $38,600 a year. Assuming an average Social Security benefit of $17,500, the shortfall is $21,100.

Assuming also that typical retirees will withdraw roughly 4% a year from their retirement savings, that shortfall can be generated with savings of $527,500. And if savings grow at a real rate of 4% over 40 years of employment — a more conservative long-term growth rate than the historical real return of 6% a year from a traditional 60/40 portfolio, given historically low interest rates and high U.S. stock valuations — employers can provide workers with the savings they need by contributing $5,500 a year to a retirement account on their behalf, or $2.64 an hour based on a 2,080-hour work year.

Many employers already contribute to 401(k)s by matching some portion of workers' savings, but the workers who can't afford to save are the ones who most need those contributions. The government can also do its part by excluding employers' contributions from tax, as well as the growth and eventual withdrawal of those retirement savings.

(Upcoming event: InvestmentNews Retirement Income Summit)

The flaws of 401(k) and other defined contribution plans are well understood, and more needs to be done to make them cheaper and simpler. But retirement plans are worthless if they can't be funded. After all, workers can't save what they don't make.

Nir Kaissar is a Bloomberg Opinion columnist covering the markets. He is the founder of Unison Advisors, an asset management firm. He has worked as a lawyer at Sullivan & Cromwell and a consultant at Ernst & Young.

And that's optimistic. Social Security income is based on wages earned during one's working years. According to the GAO report, the median annual income of households with no retirement savings and no pension was $18,932 in 2013. That's a fraction of the median household income of $53,585 that year, according to the Census Bureau, which is likely to mean that those households' Social Security benefits will be well below average, too.

With that little income, those households are fortunate to save at all. According to the GAO, they had a median net worth of $34,760 and financial assets of just $1,000 in 2013. But even better-paid workers struggle to save because the median household income is well below the cost of living. Roughly three-quarters of households aged 55 to 64 had $150,000 or less in retirement savings in 2013. That isn't nearly enough, and unless wages rise, younger workers won't be any better prepared for retirement.

(More: Top reasons to file a tax extension)

Workers once had brighter retirement prospects, if not higher wages. What's changed is that over the last four decades, a growing number of employers replaced their pensions with 401(k) and other defined contribution plans, shifting the responsibility of saving for retirement to employees. According to the Employee Benefit Research Institute, 28% of private sector workers who participated in an employment-based retirement plan were enrolled in a traditional pension in 2014, down from 84% in 1979.

It's hard to blame employers. Pensions are difficult and costly to manage, as any number of underfunded corporate and government plans can attest. Workers also move jobs more often than they used to, so employers may not feel as responsible for their futures. But employers have no doubt saved a fortune by abandoning pensions, and given that real wages have hardly moved over the last four decades, there's little indication they passed those savings on to workers.

It wouldn't cost employers much, however, to give workers some retirement security again. By my calculation, it amounts to $2.64 an hour.

Here's how I get there: According to the Economic Policy Institute, the cost of living for a single person in, say, the Chicago metro area, is $38,600 a year. Assuming an average Social Security benefit of $17,500, the shortfall is $21,100.

Assuming also that typical retirees will withdraw roughly 4% a year from their retirement savings, that shortfall can be generated with savings of $527,500. And if savings grow at a real rate of 4% over 40 years of employment — a more conservative long-term growth rate than the historical real return of 6% a year from a traditional 60/40 portfolio, given historically low interest rates and high U.S. stock valuations — employers can provide workers with the savings they need by contributing $5,500 a year to a retirement account on their behalf, or $2.64 an hour based on a 2,080-hour work year.

Many employers already contribute to 401(k)s by matching some portion of workers' savings, but the workers who can't afford to save are the ones who most need those contributions. The government can also do its part by excluding employers' contributions from tax, as well as the growth and eventual withdrawal of those retirement savings.

(Upcoming event: InvestmentNews Retirement Income Summit)

The flaws of 401(k) and other defined contribution plans are well understood, and more needs to be done to make them cheaper and simpler. But retirement plans are worthless if they can't be funded. After all, workers can't save what they don't make.

Nir Kaissar is a Bloomberg Opinion columnist covering the markets. He is the founder of Unison Advisors, an asset management firm. He has worked as a lawyer at Sullivan & Cromwell and a consultant at Ernst & Young.

Eliseo Prisno, a former Merrill advisor, allegedly collected unapproved fees from Filipino clients by secretly accessing their accounts at two separate brokerages.

The Harford, Connecticut-based RIA is expanding into a new market in the mid-Atlantic region while crossing another billion-dollar milestone.

The Wall Street giant's global wealth head says affluent clients are shifting away from America amid growing fallout from President Donald Trump's hardline politics.

Chief economists, advisors, and chief investment officers share their reactions to the June US employment report.

"This shouldn’t be hard to ban, but neither party will do it. So offensive to the people they serve," RIA titan Peter Mallouk said in a post that referenced Nancy Pelosi's reported stock gains.

Orion's Tom Wilson on delivering coordinated, high-touch service in a world where returns alone no longer set you apart.

Barely a decade old, registered index-linked annuities have quickly surged in popularity, thanks to their unique blend of protection and growth potential—an appealing option for investors looking to chart a steadier course through today's choppy market waters, says Myles Lambert, Brighthouse Financial.