The demise of an exchange-traded note is often accompanied by accusations, investigations and heavy losses. Rarely, if ever, has it involved the year’s best-performing product and assets well north of $1 billion.

The shocking decision by Credit Suisse Group to drastically slash its ETN business, delisting nine securities worth nearly $3 billion, is the most powerful display yet of the existential crisis engulfing this corner of America’s $4.4 trillion market for exchange-traded products.

The move -- which the Swiss bank says is to better align its products with growth plans -- comes as the coronavirus-fueled turmoil throws a harsh new light on ETNs. They frequently use derivatives to amplify returns, making them vulnerable to extreme market events. Already this year issuers including UBS Group and Citigroup Inc. have liquidated products.

The scale of the Credit Suisse move has sent a shock wave through the industry, however. Unless investors redeploy their cash into similar notes, the $10.8 billion ETN market is about to shrink by more than a quarter.

“That would not seem to portend especially well for them being a central part of the industry going forward,” said Jeffrey Ptak, global director of manager research for Morningstar Inc.

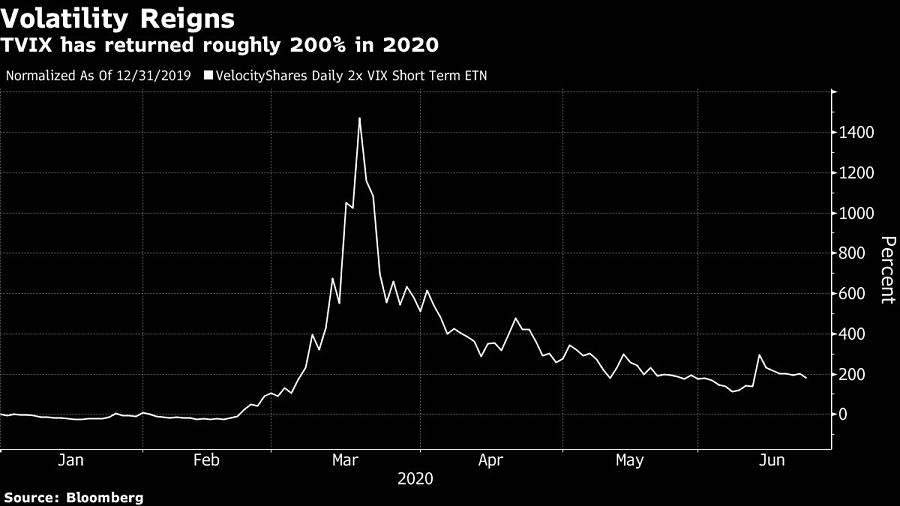

The highest-profile loss will be the VelocityShares Daily 2x VIX Short-Term ETN (TVIX), one of the most popular notes for betting on volatility in U.S. stocks. At the time of this week’s announcement, it boasted $1.5 billion of assets and year-to-date returns of more than 200% -- the best performance among almost 2,400 ETPs in the U.S.

A spokeswoman for Credit Suisse declined to comment further on the reasons for the delistings, and it remains to be seen how the disappearance of products such as TVIX will impact the assets they track.

But for the ETN ecosystem, it’s the latest dramatic twist in a year of reckoning, with analysts increasingly questioning the viability of such products even as the ETF industry continues its astronomical growth.

Unlike ETFs, ETNs are unsecured debt obligations issued by banks that are backed by the issuer rather than the assets the product is linked to. They’re often used as a way to get leveraged exposure to asset classes that may not fit into the confines of a traditional fund -- a practice coming under increased scrutiny from regulators.

“ETNs are quintessentially niche and, at this point, are not the first name in reliability,” said Ptak.

The notes earned a black eye after a massive spike in expected stock volatility blew up multiple products in February 2018, with a feedback loop emerging that saw ETNs exacerbate the damage.

Even before that, TVIX was no stranger to controversy. At one point in 2012, the VIX-linked note plunged by 50% in two days. Credit Suisse had frozen new share creation, citing internal limits on the size of the product, and when it started issuing shares again the price of the ETN crashed.

The bank’s decision to finally pull the plug is a warning sign about the ETN space as a whole, said CFRA Research’s Todd Rosenbluth.

“That certainly sends a signal to investors that perhaps these products don’t have the viability,” said Rosenbluth, CFRA’s head of ETF and mutual fund research. “The delisting risk is something people tend not to pay attention to, and they really should.”

TVIX has emerged as a go-to vehicle for individual investors looking to wager on the stock market’s swings.

The number of users holding the note on trading platform Robinhood climbed to 26,000 this month, according to Robintrack, a website unaffiliated with the site that uses its data to show trends in positioning. That compares to under 3,000 at the beginning of February.

It seems likely this factored into the Credit Suisse decision. Leveraged ETNs can significantly outperform over short periods, but they experience huge deviations from the assets they track in times of turbulence and underperform over the long term thanks to daily price adjustments.

In other words, such ETNs will trend toward zero if purchased as a buy-and-hold investment, according to Nate Geraci, president of investment advisory firm the ETF Store. Renewed regulatory scrutiny and the risk that retail investors don’t fully appreciate those nuances may have pushed banks away from the space, he said.

“Do some of those investors understand the risk? Sure. Do they all? There’s no question that they do not,” Geraci said. For issuers, “it’s reputation risk, it’s their ability to hedge the underlying exposure, and to a certain degree, some of these banks may just want to clean up their balance sheet.”

TVIX had gained 204% this year through Friday, but an investor who bought at the start of 2019 and sold at the end would have lost almost everything. The product has also regularly conducted reverse share splits -- a practice of reducing the number of shares outstanding in order to increase their value, usually to avoid delisting.

Still, thanks to its expense ratio of 1.65%, the ETN was undoubtedly a good earner for Credit Suisse. That may be one reason the bank hasn’t killed the products outright -- instead it says the nine notes can still trade on an over-the-counter basis after their delisting next month.

Meanwhile, analysts are split about what happens next.

As Credit Suisse and other banks retreat from the market, Ptak reckons it’s unlikely that other issuers will step up to fill the void, while Rosenbluth expects the number of ETNs to continue to dwindle over the next five years.

But TVIX’s popularity could motivate other issuers to launch similar volatility-linked products, says Ken Monahan of Greenwich Associates. Demand is still robust: The $1 billion iPath Series B S&P 500 VIX Short-Term Futures ETN (VXX) absorbed its largest one-day inflow since March as stocks extended their surge.

“My guess is that someone will pick it up,” said Monahan, a senior analyst covering market structure and technology. “The difficulty is that a firm like Credit Suisse starts out with a huge advantage because it has a huge distribution network. But my guess is the independent shops will try.”

Orion and RFG Advisory tackle account-opening delays with new updates as custodial integrations reshape how fast advisors can move client assets.

The deal extends the acquisitive mega-RIA's rapid 2026 expansion as industry consolidation hits record levels nationwide

As recent Middle East tensions put the Strait of Hormuz back in focus, a structured process with purpose can help protect investors against their natural self-sabotaging tendencies in choppy markets.

ESG-focused Longwave Financial, approaching $1B AUM, acquired Seattle-based MG Financial and hired a client services manager from an LPL-affiliated firm.

Tokenization goes mainstream with regulators watching prompting some firms to take a proactive approach.

Northern Trust’s Ken Lassner shows advisors how to convert volatility into after-tax portfolio gains

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income