The Federal Reserve left interest rates near zero and signaled it would hold them there through at least 2023 to help the U.S. economy recover from the coronavirus pandemic.

The Federal Open Market Committee “expects to maintain an accommodative stance of monetary policy” until it achieves inflation averaging 2% over time and longer-term inflation expectations remain well anchored at 2%, the central bank said in a statement Wednesday following a two-day policy meeting.

The statement reflects the central bank’s new long-term policy framework in which officials will allow inflation to overshoot their 2% target after periods of underperformance. That shift was announced by Chair Jerome Powell last month at the central bank’s annual Jackson Hole policy conference.

“This very strong, very powerful guidance shows both our confidence and our determination,” Powell told a press conference following the decision. “We’re strongly committed to achieving our goals and the overshoot.”

Treasuries were little changed, with the 10-year yield steady at about 0.69% as investors digested the news. Stocks gained.

The vote, in the FOMC’s final scheduled meeting before the U.S. presidential election on Nov. 3, was 8-2. Dallas Fed President Robert Kaplan dissented, preferring to retain “greater policy rate flexibility,” while Minneapolis Fed President Neel Kashkari dissented in favor of waiting for a rate hike until “core inflation has reached 2% on a sustained basis.”

Powell and other Fed officials have stressed in recent weeks that the U.S. recovery is highly dependent on the nation’s ability to better control the coronavirus, and that further fiscal stimulus is likely needed to support jobs and incomes.

The Fed on Wednesday committed to using its full range of tools to support the economic recovery. The central bank repeated it will continue buying Treasuries and mortgage-backed securities “at least at the current pace to sustain smooth market functioning.” A separate statement on Wednesday pegged those amounts at $80 billion of Treasuries a month and $40 billion of mortgage-backed securities.

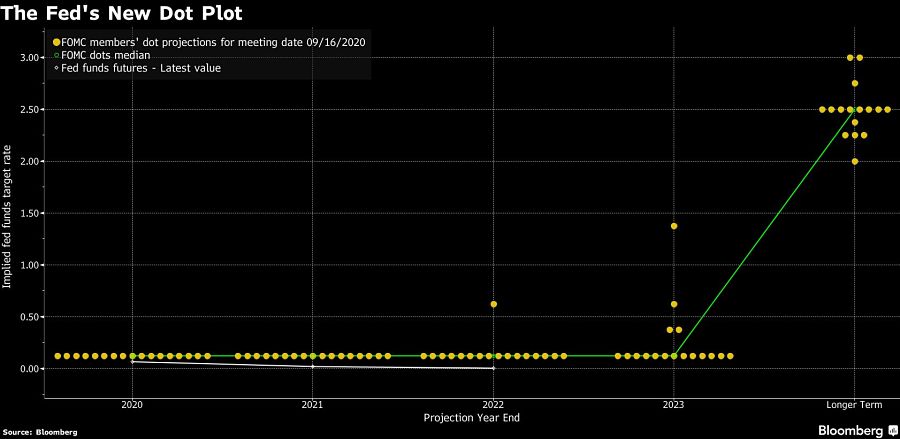

Officials see rates staying ultra-low through 2023, according to the median projection of their quarterly forecasts, though four officials penciled in at least one hike in 2023.

In other updates to quarterly forecasts, Fed officials see a shallower economic contraction this year than before, but a slower recovery in the coming years.

“The recovery has progressed more quickly than generally expected,” Powell said, while cautioning that the pace of activity will likely slow and “the path ahead remains highly uncertain.”

In addition to slashing borrowing costs in March, the central bank has pumped trillions of dollars into the financial system through bond purchases and launched a slew of emergency lending facilities to keep businesses afloat.

The economy has partly recovered from the steepest downturn on record and some sectors such as housing are doing well, but COVID-19 continues to kill thousands of Americans each week, unemployment remains high and industries like hospitality and travel are depressed.

Moreover, temporary extra jobless benefits are running out and the political stalemate over a new round of stimulus threatens to set back the economy. Uncertainty could hang over government policies at least until the outcome of the presidential and congressional elections is clear. Republicans including President Donald Trump -- who trails challenger Joe Biden in national polls -- have proposed a smaller package of aid than Democrats have.

Powell said that fiscal measures taken early in the crisis were a big help and more was probably needed.

“The overwhelming majority of private forecasters who project an ongoing recovery are assuming there will be additional substantial fiscal support,” he said, noting around 11 million Americans remain out of work and will require further assistance.

Here are some highlights from the Fed’s latest forecast:

As $84 trillion prepares to change hands, advisors who treat estate planning as peripheral are quietly building a sieve, not a book.

Traders will be able to connect their own third-party AI agents to the brokerage platform.

The bank's outspoken CEO says it's scanning for deal targets even as geopolitical risks and elevated asset prices cloud the outlook.

Virtual family office platform Strad and Ai-native CRM slant are also supporting centralization for advisors with newly inked partnerships.

Meanwhile, Raymond James' employee arm welcomes a $550 million advisor from JP Morgan, and LPL attracts another advisor trio from D.A. Davidson.

As $84 trillion prepares to change hands, advisors who treat estate planning as peripheral are quietly building a sieve, not a book.

In volatile markets, the advisors who win aren't the ones with the best calls - they're the ones whose clients stay the course.