The February edition of the latest in financial #AdvisorTech kicks off with the news that the financial monitoring software platform Elements has raised $5 million in a seed-extension funding round as it seeks to establish a foothold in the rapidly growing AdvisorTech category of advice engagement tools designed to draw clients further into the ongoing financial planning process.

As the focus of financial advice shifts from the plan that’s created initially and then only periodically updated every few years, to a year-round process of ongoing planning, the demand has grown for more tools that help advisors connect and engage with their clients more frequently while also giving them actionable information to engage about. In this area, Elements has positioned itself as an early leader that’s now gaining momentum.

The latest highlights also feature a number of other interesting advisor technology announcements, including:

Read the analysis of these announcements in this month's column, along with a discussion of more trends in advisor technology, including:

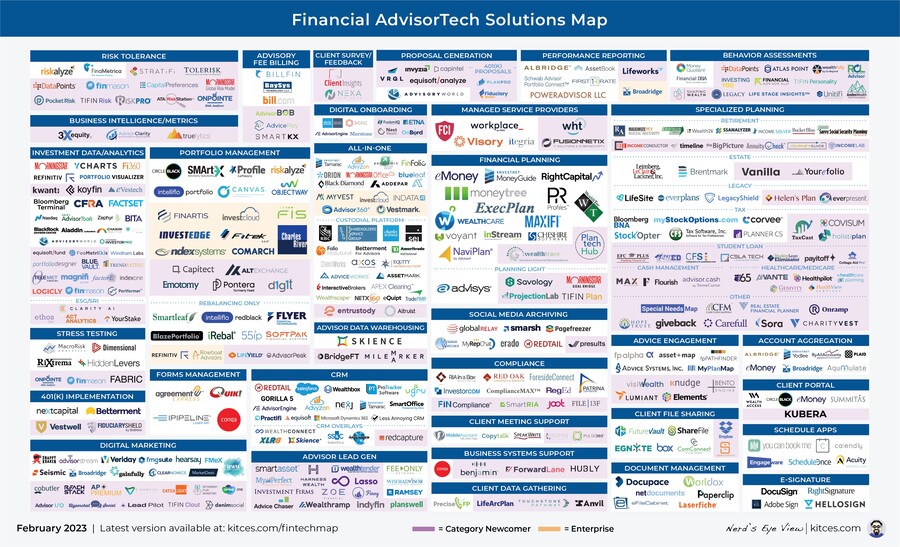

Be certain to read to the end, where we've provided an update to our popular “Financial AdvisorTech Solutions Map” and also added the changes to our AdvisorTech Directory.

AdvisorTech companies that want to submit their tech announcements for consideration in future issues, please send to [email protected].

Traditionally, financial planning software was designed around building the plan. Advisors would gather data from the client, run it through the software’s calculators, and produce a voluminous financial plan estimating the client’s ability to reach each of their various financial goals. This type of software was introduced at a time when much of financial planning revolved around the sales of investment or insurance products, with the plan being built and delivered just once — and often being provided for free upfront — as a way to identify a gap and demonstrate the client’s need for a particular financial product (which the advisor could then get paid a commission for selling to them).

As many advisors went from selling financial products on commission to managing diversified asset-allocated portfolios for their clients for an asset-based fee, financial planning software also evolved to reflect the shift from a transaction-based model of financial advice to an ongoing relationship-based one. At this point, financial planning software wasn’t just about identifying gaps and demonstrating needs that the advisor could sell in to, it was about making the client feel understood so the advisor could establish and deepen the client relationship. Furthermore, technology improvements made it easier to update plans as clients’ financial circumstances changed over the years of that relationship, and features like account aggregation made it possible for certain parts of the plan to be updated automatically. The software also evolved to become a hub of sorts for all of a client’s financial information — from balance sheets to investment holdings to tax returns and other financial documents — enabling advisors to have a deep understanding of their clients’ financial situations at all times.

But as the industry has continued to evolve, managing diversified asset-allocated portfolios on an ongoing basis has become more commoditized, and the pressure is growing on advisors to demonstrate more ongoing value than just the ongoing advisor-client relationship itself — which in turn has led to a push toward providing more year-round value through financial planning. Traditional financial planning software, however, is at its core still about the plan and its long-term projections of retirement scenarios. This is fine when a client comes in once a year for an annual review, but doesn’t bring much additional value when revisited throughout the year, since a financial plan with a 30-year-plus time horizon isn’t likely to see much change from one month (or often even one year) to the next.

As a result, there’s been increasing demand for tools that reflect the evolution of financial planning from a one-time or annual plan to a continuous process of planning. This involves not only giving advisors continuous and reliable information with which to provide recommendations, but also keeping the clients themselves engaged in the process and aware of the value it provides. Consequently, advice engagement technology — i.e., solutions that draw clients into the ongoing and continuous process of financial planning — has been one of the most rapidly-growing categories on the Kitces AdvisorTech Map in recent years.

Elements has been one of the early platforms that’s beginning to capitalize on this advice engagement boom. Originally developed by Reese Harper as a proprietary financial planning system for his own RIA, Dentist Advisors, Elements was launched as a stand-alone financial monitoring software in May 2022, and reportedly is now being used by around 300 advisory firms. Elements’ key innovation is distilling a client’s financial health into 12 separate vital signs, which creates a standardized set of metrics for each client that advisors (and clients themselves) can track and monitor over time via their financial dashboard. Another feature is its primarily mobile-app-based user interface, which make it far more compelling as a tool to easily check in with more regularly than traditional financial planning software (that requires substantive inputs to run a single update). In other words, by eschewing the often-overwhelming comprehensiveness of traditional financial planning software and focusing on a handful of simple but meaningful numbers, the Elements app leans into the notion that less is often more when it comes to getting clients to act on advice. This fact is amplified by Elements’ recruitment of Carl Richards, the foremost evangelist of pared-down financial planning, as its chief brand officer in June 2022.

Elements has kept the momentum going into 2023 with a new $5 million seed extension round led by tech venture firm Flyover Capital, which notably includes RIA entrepreneur Marty Bicknell as its general partner. The latest Elements funding round comes just over a year after its initial $4 million seed funding round in late 2021.

This latest $5 million round is projected to fund about 24 months of operating expenses, meaning that while Elements works to expand its footprint, it is still burning cash in its early growth phase. By Harper’s own estimates, Elements’ current annual recurring revenue is around $1 million, which would mean it will need to more than triple its current revenue just to break even and start turning a profit.

In a way, this makes it even more impressive that Elements has continued to raise funds, especially given the gloomy overall environment for venture capital fundraising. Clearly, investors see that there’s plenty of untapped demand from financial advisors for advice engagement tools — and given that one of the Flyover Capital partners who led this round was Marty Bicknell, chief executive of Mariner Wealth Advisors, some of that demand might come from enterprise-level RIAs that could provide a much quicker boost to Elements’ revenues.

As a relatively new and fast-growing software category, it’s difficult to predict how advice engagement will shake out in coming years. There’s certainly demand for tools that can help advisors provide value on an ongoing basis, but it’s too early yet to know which tools will become the most widely adopted by advisors, and there will almost certainly be new additions in the space before the dominant players emerge. Nonetheless, what’s clear now is that Elements is aggressively staking out a foothold for itself in the new space, before it gets even more crowded. This is important because the first movers that gain market share are often very difficult to displace later as they become established and accepted stalwarts in a no longer new AdvisorTech category.

TRADINGFRONT SHUTS DOWN BECAUSE MOST ADVISORS DON’T GROW FAST ENOUGH TO PAY FOR ONBOARDING SOLUTIONS

Robo-advisors experienced several years of rapid growth as direct-to-consumer platforms in the years following the 2008 financial crisis. This growth fueled speculation that robo-advisors could be a threat to financial advisors given their ability to provide automated asset management and an attractive, tech-friendly platform at a fee as low as 25 basis points — far less than the traditional 1% AUM fee of traditional human financial advisors. But by the mid-2010s the growth of direct-to-consumer robo-advisors had stagnated and it was clear that human advisors — at least those who focused on the personalized financial planning and advice that robo-advisors couldn’t automate — would be sticking around after all.

As robo-advisors saw their growth numbers decline in the direct-to-consumer market, an increasing number of firms began to pivot their business model to robo-advisor-for-advisor solutions, and at the same time a new generation of startups emerged that offered solely B2B robo technology. Seeing a need from advisors to streamline their own technologies for client onboarding, electronic account opening, and efficient trading and rebalancing of model portfolios, these firms now saw themselves as a natural solution to provide back-office support for the human advisors they had previously positioned themselves to disrupt.

However, more recent years have been tough on B2B robos as well. After a few years of splashy acquisitions at high valuations for early players in the B2B robo space (e.g., BlackRock buying FutureAdvisor, Invesco buying Jemstep and Principal buying RobustWealth), the market for B2B robos has slowed significantly. Some robos have shut down entirely — as Principal did with RobustWealth in 2021 — leaving the B2B robo category, now simply dubbed digital onboarding, as one of the fastest-shrinking segments of the Kitces AdvisorTech Map.

At its core, the issue with most B2B robo advisors is that they exist as a third-party technology overlay on an existing custodial platform, either in an effort to modernize an existing legacy player or as an advisor interface/layer on top of the more technology-forward brokerage platforms such as Interactive Brokers or Apex Clearing. This means that to offer these solutions, advisors must either pay more to get an additional digital onboarding technology layer on top of their existing, free RIA custodian, or they must first move existing clients from their legacy custodian over to the new one with all the back-office work that entails. Then they pay the robo-advisor a percentage of their AUM to use the platform on top of any fees the RIA custodian itself charges.

But as it turns out, most advisors just aren’t interested in paying more and/or repapering client accounts just to get better onboarding technology. Instead, they would rather have their existing custodian provide — for free as part of its existing offering — the type of digital onboarding and automated asset management experience that B2B robos charge for. And given the reality that individual advisors don’t typically even onboard lots of new clients in any given year (e.g., the average annual new client growth rate for advisory firms was just 5.1% per the most recent Schwab RIA Benchmarking Study), the ability to streamline onboarding — one of the main selling points of B2B robos — didn’t actually solve a major advisor pain point to begin with. Stated more simply, most financial advisors aren’t actually growing enough and experiencing enough growing pains to make it worthwhile to pay a premium for a more efficient onboarding solution.

Last month, TradingFront — a white-label B2B robo advisor on the Interactive Brokers custodial platform — became another casualty of the inhospitable environment for B2B robos providing digital onboarding and related robo automation tools, announcing that it was shutting down its U.S. operations as of March 1. The explanation given for the news was that TradingFront’s parent company Tiger Brokers was winding down its introducing broker business, which is both what allowed TradingFront to offer its paperless account opening, trading and transactions features and also was necessary for TradingFront to get paid for those services. Going forward, Tiger Brokers will pivot its business focus to the Asian market and interestingly, TradingFront will continue to operate in Singapore, where it rolled out in 2018.

While the official explanation is that TradingFront had to shut down because its parent company pulled the plug on a core part of its business model, the part left unspoken is that shutting down wasn’t necessarily TradingFront’s only option. If Tiger Brokers had felt it had a successful business on its hands, it might have found a way to keep it operational, such as not winding down its introducing broker business to begin with. If it felt that TradingFront just didn’t fit in with the long-term business plan, it could have found a buyer willing to keep it going. Instead, TradingFront is simply closing its doors, suggesting that although the shutdown of its introducing broker may have been the immediate cause, deeper down was the fact that TradingFront just wasn’t seeing enough traction from advisors willing to pay for its digital onboarding (and other automation tools) to sustain its operations.

Luckily for advisors who used TradingFront, the news of its closing doesn’t necessarily mean that clients will need to be moved to a completely different custodial platform. TradingFront clients will remain on the Interactive Brokers platform, though without the white-label overlay that TradingFront provided. And as Interactive Brokers somewhat snarkily noted in its response to the announcement, “80% to 90%” of the functionality that TradingFront brought was simply an extension of what is already offered on the interactive brokers platform.

For the industry as a whole, this news highlights the continuing struggle B2B robos face to convince advisors that repapering their clients with a new, more digitally-savvy custodian and/or paying up with a basis-point fee for a more streamlined client onboarding experience is actually worth the cost. In part, though, this may simply be a cost structure issue, as notably most all-in-one platforms that now offer robo-like capabilities — such as Orion and Tamarac — do so for a flat per-account fee. This means that the potential hit to an advisory firm’s profit margins is reduced as a firm gets bigger, whereas the basis-point fees charged by platforms like TradingFront grow in tandem with AUM. Ironically, B2B robos were trying to sell scalability with a bps-fee structure that doesn’t actually scale as the firm grows larger, while all-in-one platforms that charge software fees do and at a comparatively smaller fee in the first place, as most advisors only spend 3% to 5% of revenue in total on technology, far less than the bps fees that most B2B robos sought to charge.

In the meantime, as traditional custodians like Charles Schwab continue to slowly improve their technology offerings for advisors, and as technology-first custodians like Apex Clearing (which once was designed only to build third-party platforms on top of) look to begin offering custodial services directly to advisors, the window for B2B robos to differentiate themselves will only narrow further. Furthermore, the problem that B2B robos were introduced and marketed to solve — that is, ugly and inefficient account opening and portfolio management processes at legacy custodians — is becoming less and less of a real problem for advisors as they find ways to solve those problems with the custodian they already have. This means we may be likely to see more B2B robo and other digital onboarding firms either pivoting again to a new business model or shuttering as TradingFront did.

ZOE LAUNCHES DIGITAL TAMP FOR SMALL CLIENTS TO COMPLEMENT ITS REFERRAL SERVICE FOR RIAS

In the mid-2010s, when robo-advisors that had previously used solely a direct-to-consumer business model began to reinvent themselves as tech-forward investment management platforms for advisors, one of the main sales pitches for the new generation of B2B robos was: “We’ll dramatically reduce the time it takes for you to onboard and serve clients by making it possible for new clients to sign up on your website, open an account and start investing with just a few mouse clicks, unlocking your ability to efficiently serve the next generation of clients (even if their accounts are smaller than your traditional minimums.”

It sounded revolutionary, but those well-intentioned predictions didn’t pan out in reality. For one thing, advisors who adopted investment management technology generally didn’t use it to serve a greater number of small-account clients. Instead, they used it to reduce the time they spent on manual investment management tasks and increase the breadth and depth of their financial planning for each client. Ironically, this often allowed them to go deeper, attract bigger, more affluent clients and charge higher advisory fees per client, contrary to the claims that robo technology would democratize financial advice for underserved populations by reducing its cost.

But even if advisors had opted to use those robo tech platforms to serve a wider range of clients, there was still one major problem that the technology didn’t solve for: How to actually bring potential next-generation clients to the advisor in the first place. After all, having a tech solution that makes it easy to sign up and invest on an advisor’s website means little if no next-generation prospects are coming to the website to begin with. For all their other features, B2B robos didn’t bring small clients to RIAs by virtue of their own existence. Advisors still needed to market to and sign on new clients, and to put it bluntly, it wasn’t good enough to put a “Millennials, sign up here” button in between the lighthouse and the Adirondack chairs on the RIA’s retirement-centric website and expect to get an onslaught of new next-generation-client assets. In the same way that “if you build it, they will come” didn’t work for direct-to-consumer robos for getting next-gen clients, it didn’t work for the B2B generation of investment management tech either.

One way to solve this marketing problem for financial advisors — particularly those with few resources or time to spend on marketing themselves — is by hiring an outsourced lead generation service to bring those next generation and other more traditional new clients. One such service that has gained traction in recent years is Zoe Financial. Zoe’s process for matching advisors with prospects — which includes a vetting process for advisors, a hands-on approach to interviewing and qualifying prospects, and a contingency-based fee model in which advisors pay only for leads who eventually convert to a client — has made it popular with advisors and clients alike, with (per Zoe’s website) over 4,000 advisors now being listed on Zoe’s network.

Even with 4,000 advisors to choose from, however, there can still be a mismatch between the prospects who go to Zoe looking for a financial advisor, and the advisors who are actually on the network. Namely, if a prospect doesn’t have a certain level of assets or the income to pay for a monthly flat fee, they may not be able to find an advisor willing to work with them — especially since, as noted above, advisory fees and investment minimums have broadly gone up in recent years. Advisors must also generate enough in client fees to cover Zoe’s marketing costs, too. Yet as Zoe’s popularity increases via word-of-mouth and mainstream press attention, along with its own marketing efforts to attract more prospective clients, that backlog of prospects who aren’t able to meet traditional advisor minimums only grows — with each prospect representing a lost opportunity for new revenue for Zoe as long as they aren’t matched with an advisor.

In that context, it’s notable that Zoe announced the launch of its new Zoe Wealth Platform. a TAMP-like solution exclusively for advisors on its network, which was announced in January. The platform includes many of the standard TAMP features such as digital account opening, automated rebalancing, preloaded investment models, and a client-friendly dashboard. But unlike similar TAMPs that have struggled or faded away in recent years, Zoe Wealth Platform actually comes with a way for prospective clients to find their way to the advisors using it, in the form of Zoe’s already popular lead generation service.

In other words, while historically the digitally-savvy robo-TAMP solutions struggled to help advisors actually scale up with next-generation clients because the advisors couldn’t get those clients in the first place, Zoe’s offering is unique because their challenge is that the platform was already generating those leads but didn’t have a way to refer and monetize them. Whereas with Zoe Wealth Platform, the company will handle the bulk of the onboarding and implementation process while allowing RIAs in its network to get paid to just be the advisors that overlay Zoe’s TAMP offering.

What remains to be seen is how advisors on Zoe’s network will use the new TAMP, or whether they will do so in numbers significant enough to justify Zoe’s investment in yet another investment technology platform. Although advisors have proven willing to pay a high price — 25% of their ongoing advisory fee or more — for Zoe’s core service of referring quality prospects, they historically haven’t been willing to pay a significant basis-point fee for a third-party investment technology solution.

Still, the news of Zoe’s expansion from lead generation service to small-client TAMP highlights how successful the company has been at generating leads for advisors, to the point that it’s making further investments to monetize even more of its prospective client lead flow. That further signals that despite naysayers’ questions about whether it’s really worthwhile to pay a percentage of revenue for lead generation, Zoe is still seeing more than enough demand from advisors willing to pay for a scalable growth channel to further invest into its lead flow. And ultimately, even if the TAMP doesn’t meet expectations, there are no signs that Zoe’s core lead generation service is slowing down. In fact, given that Zoe recently raised an as-of-yet undisclosed amount of capital from several of its own client firms, it seems that RIAs are not only willing to pay good money for reliable lead generation — they are also willing to invest in the platform that provides it.

Advisor360 began life as a proprietary advisor technology platform of the independent broker-dealer Commonwealth Financial Network, existing to provide CRM and other business workflow support to Commonwealth’s network as it grew to more than 2,000 advisors. But as the platform grew and became more complex in scope, it got so costly to run that even with Commonwealth’s ongoing growth in advisor head count, the market of only Commonwealth advisors wasn’t big enough to sustain it and amortize its development costs.

So in 2019, Commonwealth made a big splash by licensing Advisor360 to MassMutual and its network of over 9,000 insurance broker-dealers, instantly increasing its potential user base by over five times, from 2,000 to 11,000-plus. Simultaneously, Commonwealth spun off Advisor360 into its own stand-alone tech company, sacrificing the platform’s exclusivity with Commonwealth advisors for the ability to reach a much broader market of broker-dealers. Furthermore, in 2020, Advisor360 hired a new chief executive with a background in enterprise-scale technology, signaling the newly independent company’s ambitions to position its software as a solution for large-scale enterprises.

In the years since then, however, Advisor360 has yet to announce any additional partners of the likes of MassMutual. This highlights two points: First, it shows just how difficult it is to get a foot in the door with large enterprise clients — for whom the costs of migrating thousands of reps to an entirely new, multifaceted technology platform can be immense. Second, it suggests that the risks that were brought up at the time of Advisor360’s spinoff — that a technology platform developed solely for Commonwealth’s own advisors might not generalize across the industry — might prove founded after all.

Still, Advisor360 has ground on, looking for new ways to expand its capabilities, and more importantly to get its technology in front of potential new enterprise clients. In March 2022, it introduced a strategic partnership with State Street’s Charles River Development, a managed account platform for enterprise wealth management firms. In June 2022, it rolled out new capabilities for viewing and reporting on beneficiaries for clients’ insurance products, representing a doubling down on features that would primarily appeal to insurance brokers after its MassMutual success. And last month, it announced its first-ever acquisition of another software company, the digital onboarding technology firm Agreement Express.

In terms of how the acquisition will impact Advisor360’s technology offering, it serves to deepen its digital onboarding capabilities by adding Agreement Express’ integrations with multiple RIA custodians and CRM software, allowing Advisor360 users to, for instance, auto-populate multiple types of brokerage account applications using client information directly from the advisor’s CRM fields. But given that Advisor360 already has digital onboarding capabilities, and almost certainly has the resources to develop them further in-house to bring them to the level that Agreement Express offers, the question is why Advisor360 decided at this juncture to acquire a separate firm, rather than investing to improve its own solution.

This brings us to the other thing that Advisor360 will be getting in this acquisition, along with the Agreement Express technology itself: the list of Agreement Express’ existing enterprise clients, who are coming along with the company. While there isn’t any indication yet of who’s on that list, given how Advisor360 has continually doubled down on features and partnerships that would make it appealing to enterprise clients, including both insurance and investment account applications, one has to imagine that there are some (insurance-broker-dealer) enterprise names that Advisor360 would like to get in front of.

Notably, existing clients of Agreement Express won’t automatically become clients of Advisor360 — it will continue to operate as a stand-alone firm for the time being. However, simply gaining the opportunity to cross-sell Advisor360’s solutions to Agreement Express’ clients could prove highly valuable, particularly if the main issue over the last few years has been Advisor360’s challenge in just getting its foot in the door with the types of enterprise firms it seeks to work with more holistically.

Overall, Advisor360’s acquisition of Agreement Express serves as a reminder that while the bulk of advisor head count (and therefore, revenue and growth opportunities for advisor tech firms) is in larger enterprises, it’s incredibly difficult for technology platforms to get in front of enterprise-level clients. With its apparent struggles to sell its technology on the open market following the initial coup of landing MassMutual, Advisor360 has taken a new tack, first demonstrated by its Charles River Development partnership, and now more substantively with its acquisition of Agreement Express. By partnering with or acquiring firms with complementary offerings that have their own roster of enterprise clients, Advisor360 can not only improve its own offering, but also gain access to an established list of enterprise clients that have proven elusive to it so far.

In the early days of portfolio performance reporting, advisors would download custodial data each day to their in-office servers, then manually clean up and reconcile that data to be able to calculate clients’ portfolio performance — a process that took up a huge amount of back-office resources. It also meant that every single firm needed to download what was essentially the same asset price and transaction data, and make the same adjustments for itself (e.g., allocating basis to shares in the case of stock splits or company spinoffs, properly classifying corporate restructuring events, etc.). Eventually, outsourced back-office solutions arose to perform the data reconciliation process for several firms at once on a somewhat-more-centralized basis, but it still made for an inefficient one-database-at-a-time process.

With the rise of the internet and cloud computing, however, firms like Orion, Black Diamond, Tamarac and Addepar were able to streamline the process of data reconciliation immensely. They could essentially download all of the custodial data to one centralized database in the cloud, clean it up themselves, and create tools such as performance reporting or billing automation for their clients that were built off of the data they stored. This meant thousands of downloads and reconciliations by each firm were consolidated down into one single centralized process on their behalf. Furthermore, all this custodial data was now kept on the cloud by a firm specifically entrusted with its safekeeping, rather than on local service in an advisor’s office, significantly reducing the risk of a flood, theft or some other misfortune wiping out all of the firm’s financial data.

But for everything that cloud-based reporting solutions did to streamline advisory firms’ back-office requirements, they did have one potential downside — the RIAs no longer directly owned and controlled their own custodial data. As such, they were limited to whatever tools the third-party reporting platform made available to them to access and utilize that data. If an RIA wanted to build anything such as a customized client dashboard off that data, they had little choice other than to keep downloading data directly from custodians and warehousing it themselves.

BridgeFT has been around for several years as a lower-cost performance reporting competitor to the bigger players like Orion, Black Diamond and Tamarac, providing streamlined billing and client reporting through its core product, dubbed Atlas. But in January, it announced a major new offering, called WealthTech API, that will offer client firms access to the underlying custodial data that BridgeFT uses to power its Atlas tools, so that advisory firms or even other AdvisorTech firms can build their own tools on top of centralized and fully reconciled custodial data.

Simply put, if an advisory firm wants to build a software tool based off of custodial data — client portals, billing tools, practice management dashboards — without needing to download and warehouse all the data themselves, they can now plug into WealthTech API’s application programming interface for a direct feed to that data, while BridgeFT handles the downloading and warehousing of the data itself.

What’s interesting about this news is that while BridgeFT’s original Atlas product is primarily used by smaller firms given its lower price compared to more robust offerings like Orion, its WealthTech API seems more geared toward larger-sized RIAs and even some midsize to large broker-dealers. After all, a firm would need to be fairly sizable to have the resources to invest in building a middleware software layer that could run off of BridgeFT’s data to begin with. This is a sharp contrast to the typical firm that would be using BridgeFT’s other product, the low-cost Atlas reporting platform. This means that BridgeFT may effectively be starting from scratch in finding a market for WealthTech API although given the fairly small market share of Atlas among financial advisors — only 1.2% in the 2021 Kitces Report on Financial Advisor Technology — that may be an intentional shift in strategy toward bringing in more firms with deeper pockets than Atlas was able to attract.

Either way, with WealthTech API’s introduction, BridgeFT joins a small but growing group of platforms specializing in managing and integrating custodian and other financial data, a group that also includes MileMarker, Skience and Wealth Access. The expansion of this category of AdvisorTech reflects the growing need for solutions for advisory firms to manage data across their own expanding tech stacks. It also presents an opportunity to provide solutions for firms that want more control over their data to be able to build their own custom software layers as a way to differentiate themselves. Against this backdrop, BridgeFT might have better luck standing out from the crowd as an outsourced data warehouse and integrator of data than it did as an outsourced performance reporting platform.

KWANTI EXPANDS ITS FOCUS ON ADVISORS MANAGING MODELS WITH NEW SCREENING TOOL TO HELP ADVISORS FIND NEW MODEL ADDITIONS

Morningstar has long been the dominant player in investment research and analytics for financial advisors with its Morningstar Direct platform. It established its foothold in the 1980s and 1990s by providing performance data and ratings for mutual funds, back when the typical financial advisor was paid a commission to sell those funds and needed a useful tool for comparing one fund to another and nudging clients toward a decision related to why the mutual fund they were offering was better than what the prospect or client already had.

As the industry shifted away from sales of individual funds and toward creating diversified asset-allocated portfolios, however, the tools that advisors need to analyze investments also shifted from individual fund analysis to a more holistic portfolio analysis, which in turn required a different set of more portfolio-centric analytics tools. For instance, the style box or star rating of an individual fund might matter much less to an advisor than how it contributes to the diversification, asset allocation and average expense level of the entire portfolio.

In more recent years, many advisors’ needs for investment analytics have narrowed even further. Many advisors now use model portfolios to systematize their investment management process across all clients of the firm, with some even outsourcing the creation of those models to institutions like Vanguard, Fidelity and BlackRock. And although such advisors may have little need for tools to facilitate individual security selection, they do need tools to help them compare existing client portfolios to the advisor’s own models, and to find new potentially better investments that they might add to their model portfolios.

This shift has led a growing number of startups to try to chip away at Morningstar’s dominance by providing more focused investment analytics solutions. Although Morningstar may have one of the most robust analytics suites out there, many of today’s advisors don’t necessarily need — or even want — everything that Morningstar offers. By offering just the tools that advisors need — and none of the ones that they don’t — it’s possible to sell a valuable product to advisors at a lower price point than Morningstar’s across-the-board platform.

Kwanti is one such tool that has emerged as a more focused alternative to Morningstar. Its core product is based around analyzing model portfolios, comparing them to existing client or prospect portfolios, and generating proposed recommendations for prospects to transition to the advisor’s recommended model. Even though there isn’t much more to it than that, advisors don’t seem to miss the bells and whistles of a broader feature set. In the most recent Kitces Report On Financial Advisor Technology, Kwanti actually received the highest satisfaction rating among all investment analytics tools, while also having among the lowest price of such tools on the market.

Considering the tight focus of its core product, it rates as newsworthy when Kwanti rolls out an additional feature — as it recently did when it announced a new investment screening feature, in keeping with the no-nonsense personality of the platform, Screener. Like the rest of the platform, the screener emphasizes utility over flashiness. It allows advisors to screen for funds based on one or more categories of their choosing, such as expense ratio, yield, trailing performance or asset levels; to sort funds by category within those results; and to compare several funds on any of these criteria. It also includes a tool to suggest similar funds to a selected fund, which could perhaps be a simple way for finding replacement securities when performing tax-loss harvesting. As shown in the demonstration video below, there isn’t much more to learn:

While it might seem strange that Kwanti, which has been so focused on its core function of analyzing and comparing model portfolios, has introduced an individual security analytics tool, the new feature more likely represents a modest enhancement to its capabilities than the start of a larger-scale shift in focus. As even advisors who rely almost exclusively on model portfolios know, sometimes the need for customization crops up, and it’s useful to have a tool that narrows down the enormous universe of fund options to the few that might work best in a client’s portfolio. In addition, finding potential new investments to add or use as improvements to existing holdings within the advisor’s model portfolio is very explicitly a screening-style process of deciding what kind of investment would incrementally add value, and then screening the universal of available investments to find a solution that best plugs that particular hole.

It will always be difficult, if not impossible, to match the breadth of Morningstar’s investment analytics. But as Kwanti has demonstrated, solving a specific need for advisors — such as facilitating the implementation of diversified asset-allocated model portfolios — and keeping narrowly focused on that need and being able to price accordingly, can be a very viable path to growth even in a crowded AdvisorTech category.

In the meantime, we’ve rolled out a beta version of our new AdvisorTech Directory, along with making updates to the latest version of our Financial AdvisorTech Solutions Map with several new companies, including highlights of the Category Newcomers in each area to highlight new fintech innovation.

So what do you think? Do advice engagement tools like Elements help you demonstrate ongoing value to your clients? Would your firm take on more small clients if a lead generation service like Zoe brought them to you and provided the software for you to serve them efficiently? Is it more appealing to have a focused, model-centric investment management analytics platform like Kwanti, or a more comprehensive platform like Morningstar Direct?

Michael Kitces is the head of planning strategy at Buckingham Strategic Partners, co-founder of the XY Planning Network, AdvicePay and fpPathfinder, and publisher of the continuing education blog for financial planners, Nerd’sEye View. You can follow him on Twitter @MichaelKitces.

Ben Henry-Moreland is senior financial planning nerd at Kitces.com, where he researches and writes for the Nerd’s Eye View blog. In addition to his work at Kitces.com, Ben serves clients at his RIA firm, Freelance Financial Planning.

The move to charge data aggregators fees totaling hundreds of millions of dollars threatens to upend business models across the industry.

The latest snapshot report reveals large firms overwhelmingly account for branches and registrants as trend of net exits from FINRA continues.

Siding with the primary contact in a marriage might make sense at first, but having both parties' interests at heart could open a better way forward.

With more than $13 billion in assets, American Portfolios Advisors closed last October.

Robert D. Kendall brings decades of experience, including roles at DWS Americas and a former investment unit within Morgan Stanley, as he steps into a global leadership position.

Orion's Tom Wilson on delivering coordinated, high-touch service in a world where returns alone no longer set you apart.

Barely a decade old, registered index-linked annuities have quickly surged in popularity, thanks to their unique blend of protection and growth potential—an appealing option for investors looking to chart a steadier course through today's choppy market waters, says Myles Lambert, Brighthouse Financial.