The May edition of the latest in financial #AdvisorTech kicks off with the news that robo-advisor Betterment entered into a $9 million settlement with the Securities and Exchange for misrepresenting its tax-loss harvesting practices in its client agreements and marketing materials compared with its actual practices (e.g., only checking client portfolios for tax-loss harvesting every other day, after having advertised daily checks). This is a first for the SEC in scrutinizing an RIA, not for failing to execute its investment promises to clients, but for failing to execute tax-loss harvesting promises instead. This may raise questions for other RIAs (including smaller firms) who promote their tax-loss harvesting practices as part of a tax-efficient investing strategy about whether their own practices and the technology they use to implement it really align with what they claim to provide.

From there, the latest highlights also feature a number of other interesting advisor technology announcements, including:

Read the analysis about these announcements in this month’s column, and a discussion of more trends in advisor technology, including:

And be certain to read to the end, where we have provided an update to our popular Financial AdvisorTech Solutions Map and also added changes to our AdvisorTech Directory.

AdvisorTech companies that want to submit tech announcements for consideration in future issues, please submit to [email protected].

Traditionally, the main value proposition of investment managers has been managing investments themselves. Managers would seek to add alpha by picking the best stocks or bonds, or mutual fund managers, or manage along the investor’s efficient horizon to optimize their risk/return profile, or factor-tilt to take advantage of pricing inefficiencies over the long run. Whichever the method, the way the way the managers purported to earn their fee was in growing the market value of their client’s investments in some form.

But in a world where it’s harder to achieve alpha through investment decisions alone (or at least where it’s become much more widely known that most managers don’t outperform a broad-based index), investment managers have increasingly sought to demonstrate their value in other ways. One method that’s become popular in recent years has been trying to add not investment alpha, but “tax alpha,” in the form of both asset location and more commonly, via tax-loss harvesting (which rather than growing the nominal value of a portfolio seeks to avoid or defer capital gains taxes to grow the portfolio’s after-tax value).

In recent years, tax-loss harvesting has grown in prevalence among financial advisors as improvements in technology have made it easier to identify positions as a loss and trade into similar replacement securities. This is a trend that only accelerated as most broker-dealers eliminated trading fees, reducing the drag on performance that would otherwise result from frequent trading to harvest losses. It has allowed firms to implement tax-loss harvesting at scale. In practice, this means advisors at small or midsize firms can use portfolio management software like iRebal to incorporate tax-loss harvesting into their rebalancing processes for dozens or hundreds of clients at a time, while giant robo-advisors like Betterment employ proprietary algorithms to regularly harvest losses for hundreds of thousands of clients. As a result, RIAs both large and small often claim they’ll provide some tax alpha for their clients — backed by at least some research — by harvesting losses and at least in theory, reducing their tax bill.

While actual outcomes from investment managers are never assured — tax alpha, like investment alpha, will vary by whatever markets deliver and the skill of the advisor’s execution — regulators like the SEC do focus heavily on how investment managers represent themselves. This is to ensure that they don’t overpromise their capabilities via the results they advertise and at least really do execute the strategies they purport to use to achieve those results. Accordingly, if an investment advisor advertises its investment performance, it needs to be transparent about the methods it uses to calculate that performance and make it clear that the prior performance doesn’t constitute a guarantee of future results. If the advisor purports to use a certain strategy to choose investments or time its trades, it needs to prove that it actually does what it claims to do. All of that is fairly cut-and-dried when it comes to traditional ways of managing investments. But when the advisor’s investment strategy includes tax-loss harvesting, it hasn’t heretofore been clear whether regulators would also scrutinize the tax benefits that advisors claimed to provide (as they would any other investment strategy), and how effectively they implement those tax-loss harvesting strategies using their technology.

That question was least partially answered in April when the SEC settled with Betterment for a $9 million penalty relating to its tax-loss harvesting practices, specifically, regarding differences between what the robo-advisor claimed it was doing when executing its loss-harvesting strategy for its clients, and what it was doing in practice. The SEC’s complaint identifies three main issues in Betterment’s tax-loss harvesting practices spanning from 2016 to 2019:

In all, the SEC estimates that about 25,000 client accounts were impacted, or a little less than 10% of the 275,000 total accounts that have thus far opted into tax-loss harvesting. Betterment’s violations cost clients around $4 million in total tax benefits or about $160 per account in tax benefits that were lost.

On the surface this seems like an isolated event, with Betterment being a prominent target for regulators on account of its size and visibility. But in reality, the SEC’s actions have implications for anyone who does tax-loss harvesting, which is a practice that is hardly unique to robo-advisors. For one thing, the settlement stemmed from the fact that Betterment’s claims and disclosures about its tax-loss harvesting methods didn’t match what it did in practice.

But Betterment is relatively rare among RIAs in that it actually does disclose its practices around tax-loss harvesting, which has tended to fall in a bit of a regulatory gray area between tax planning and investment management. Advisors are required to describe their investment strategies and the risks involved in each in Part 2A of in their Form ADV, but how many include their tax-loss harvesting practices in that description? Will the SEC begin to require more detailed disclosures for all advisors about how exactly they implement tax-loss harvesting across each and every one of their client portfolios?

Additionally, the SEC’s action raises questions for advisors who use software to implement their tax-loss harvesting. This is practically everyone who does tax-loss harvesting, given the software’s importance in scaling the strategy on a firmwide basis. What kind of liability might advisors have if they don’t implement the software properly, or even worse if the software they purchased doesn’t actually work exactly right 100% of the time for 100% of their clients? This is a more complicated question: Betterment’s issue here stemmed from two sources, (1) the initial coding error, and (2) the fact that it misrepresented the problem to clients after it found out. But if an advisor doesn’t catch a coding error while doing due diligence for its own software (or when outsourcing its investment management to a platform — like Betterment for Advisors — that uses its own software), it’s fair to wonder whether that could open the door to regulatory issues for the advisor, even if they can catch the issue and act quickly to resolve it. Yet at the same time, how many advisors are realistically able to perfectly vet every possible scenario of their third-party trading and rebalancing software in advance? For those that claim to have built their own proprietary algorithms to optimize tax-loss harvesting, will they even be willing to share the details of their own software methodology?

Ultimately, this tax-loss harvesting settlement seems to be a shot across the bow from the SEC to advisors who use and market themselves with tax-loss harvesting, emphasizing that the age-old adage, “Whatever you say in your marketing materials, you’d better do,” applies not just to investment management, but also to any tax-sensitive overlay that the advisor provides as well. And it applies not just to how the advisory firm executes its tax-loss harvesting using software, but also the potential that the software itself has coding errors (at least or especially if the advisory firm has created its own spreadsheets or other tax loss harvesting/trading tools) that causes its execution of tax-loss harvesting to conflict with the advisor’s advertised methods. Advisors who market their tax-loss harvesting capabilities may now wonder whether they will be subject to more disclosure around tax-loss harvesting, and the extent to which their claims will be scrutinized against any benefits they actually provide — and whether those benefits to clients, and any marketing boost it gives to advisors in differentiating their services, is worth the potential regulatory hassle.

As independent RIAs proliferated in the last 20-odd years, a group of predominantly retail-focused broker-dealers (including Fidelity, Charles Schwab and TD Ameritrade) sought to leverage their existing retail economies of scale by branching out to begin providing custody services to advisors, who needed a qualified custodian to hold their clients’ assets. These RIA custodial providers covered the core functions of custody itself, such as holding client assets and facilitating trades and money movement. But they didn’t provide everything that advisors needed to fully manage their clients’ portfolios. Advisors also needed tools for additional functions like rebalancing, especially with the rise of model portfolios, portfolio accounting and performance reporting. Another function is billing across multiple accounts for a client, multiple clients in a household and potentially multiple fee schedules. This ultimately spawned a new industry of portfolio management technology aiming to fill in the gaps left between the advisors managing client investments and the custodians that held them. This resulted in RIA tech stacks that usually consisted of the custodian as the foundation, with everything else the advisor needed to manage their clients’ portfolios purchased separately and layered on top.

What made this setup practicable for advisors was that they typically didn’t need to pay anything directly to the custodian for its core services. Their underlying broker-dealer infrastructure made their RIA custodial profits off of trade commissions, spreads on sweep account cash, payment-for-order-flow and fully-paid lending, all of which were paid either from client funds or from institutional traders paying for access to those funds. But for RIAs, the third-party portfolio management technology can add up to a substantial expense — often $10,000-plus per advisor just for portfolio management and performance reporting alone. This is in addition to the complexity of getting several independent software solutions to interface correctly with one another to complete the job of portfolio management. Still, this arrangement — and the expenses involved — was generally accepted as a cost of doing business, given how essential a functioning portfolio management process is to advisors who bill on assets under management. For many years, portfolio management technology was actually so lucrative it became the most crowded category of the Kitces AdvisorTech Map with more than 50 providers all competing for advisor attention.

Into this environment entered Altruist, which launched in 2018 as a “modern custodian built exclusively for RIAs.” Unlike other custodians, which had branched out from existing retail or institutional broker-dealers — who themselves often employed advisors to compete with the independent firms whom they served as custodians — Altruist was built specifically to serve independent RIAs. Altruist aimed to provide an end-to-end custody and portfolio management software package that included the rebalancing and model management, direct indexing, billing and performance reporting that advisors typically purchased from third parties.

After several years of building out its product and gaining a foothold in the competitive RIA custodial market (particularly among newer and smaller RIAs, who face fewer hurdles in switching clients over from one custodian to another when they’re just getting started), Altruist has made several big moves so far in 2023 to position itself to compete more directly for established advisors with the likes of Fidelity and Schwab. Earlier this year, Altruist announced it would become its own self-clearing broker-dealer, and almost immediately thereafter acquired rival custodian Shareholders Service Group (SSG). In April, Altruist made news again by announcing a $112 million Series D fundraising round as it continues to ramp up its growth.

In a nutshell, the theme of this fundraising round seems to be about going upmarket from Altruist’s original core user base of smaller and newer RIAs, and expanding its capabilities to serve bigger, more established advisors and thereby accelerate the growth in its on-platform assets. Bigger RIAs have more complex needs. They require more account types, more asset classes and more portfolio models in order to serve more firms in the mid- to large-size range of $100 million to $1 billion AUM. Altruist needs the capital to further build out its technology beyond what was good enough for smaller startup RIAs.

The challenge for Altruist is that, for established RIAs, switching custodial providers (which Altruist’s existing small or startup RIAs didn’t have to do because they may have just started with Altruist in the first place) represents an enormous investment in time and resources to repaper accounts, port over and clean up historical data, and retrain staff and then adjust processes and workflows around the new technology. 2023 represents a unique opportunity in that regard given that many advisors are already switching custodians in the transition from TD Ameritrade to Schwab. This likely explains the timing of Altruist’s moves as it seeks to peel away some of those advisors during the transition period. Yet after this year, it will remain an uphill battle for Altruist to entice them to depart from their current custodians.

However, the fact that Altruist isn’t just a custodial platform, but rather an all-in-one solution with performance reporting and billing on top of its core custodial services, means that it can’t really be thought to be in competition solely with existing custodial providers, In reality, it’s competing with advisors’ entire custodial-plus-portfolio-management tech stack. If Altruist can demonstrate that advisors don’t really need to pay for third-party technology like Black Diamond or Tamarac on top of their custodial platform — and that its $1-per-account-per-month platform fee represents significant hard-dollar savings compared to the cost of advisors’ existing tools — it creates a strong selling point and an opportunity to make advisors reconsider whether it isn’t really worth switching after all. Or stated more simply, it’s not just about Altruist versus Schwab/Fidelity/Pershing, it’s about Altruist versus one of those custodians plusOrion/Tamarac/Black Diamond. If Altruist can save a midsize firm as much as $50,000 to $100,000 in portfolio management software fees with its all-in-one solution, it’s a powerful financial incentive for RIAs to go through the hassle of switching custodians.

Of course, Altruist may have less appeal for advisors who would prefer to build their custodial and portfolio management tech stack from individual third-party solutions themselves, rather than commit to an all-in-one platform. Some simply would rather have the ability to pick and choose the best solution for them, while others would rather go with a single provider with seamless integration between all its components. This is similar to why some people prefer to buy iPhones and live in Apple’s walled garden while others would rather have the customization potential of Google’s Android. So while Altruist’s approach might not be for everyone in the long run, the platform that it’s building shows that it’s clearly aiming to be the go-to custodian for advisors who do prefer their gardens to have walls and just want a platform where everything just works well enough right out of the box.

When an advisory firm manages investments for its clients, it needs a way to systematize the investment management process as it accrues more clients, accounts and assets. As the AUM model has grown over the last 20 years, there has also been increasing demand for tools that can streamline or automate the process surrounding investment management, such as trading and rebalancing, performance reporting and billing.

The need for solutions to manage client portfolios at scale has led to a plethora of portfolio management tools on the market, making it one of the most crowded categories on the AdvisorTech map. Advisors have been willing to pay for the technology. After multiplying the platform’s per-account fee by the total number of client accounts for each advisor, it isn’t uncommon for RIAs to pay $10,000 to $15,000 per advisor every year on portfolio management solutions (e.g., $40/account × 3 accounts/client × 100 clients = $12,000). Despite being one of the largest single technology expenses for an advisory firm, this has generally been considered worthwhile as a cost of doing business since the greater efficiency allowed by systematizing the investment management process means that advisors can generate more than enough extra AUM revenue to make up for the platforms’ substantial cost.

However, despite the high amount of revenue per advisor that portfolio management technology can generate, it isn’t necessarily easy being a software provider in that market today. First, the lucrative opportunity presented by portfolio management technology has lured a large number of competitors into the space — peaking at more than 50 simultaneous competitors in the portfolio management category. This puts pricing pressure on all providers as they seek to gain market share. Second, custodial platforms like Altruist, Schwab and Fidelity are increasingly building out their own technology offerings that integrate seamlessly with their own custodial services that advisors are already using at little or no extra cost, increasing the pressure on stand-alone investment management platforms to offer more tools (and further reduce prices) to differentiate themselves and justify their value. Third, once RIAs reach a certain level of size and scale, they often have the resources, and the incentive, to build their own in-house technology, which eliminates the need for a third-party option.

Two platforms that have found ways to differentiate themselves in this competitive environment are GeoWealth and First Ascent Asset Management. Both platforms are essentially turnkey asset management platforms (TAMPs) aiming to streamline asset management for financial advisors, but they approach the task in slightly different ways. GeoWealth, which was created as a homegrown tech solution originally built to serve one large advisory firm, largely used its technology as its own selling point. It offers an open-architecture TAMP platform through which advisors could implement either third-party model marketplace portfolios or the advisor’s own model portfolios. But by building its own in-house technology, GeoWealth has positioned itself as being a lower-cost provider than traditional TAMPs that have to layer their own costs on top of relatively expensive third-party portfolio management software.

First Ascent, on the other hand, leaned into portfolio management by offering its own suite of model portfolios — and perhaps more notably, became one of the only TAMPs to offer flat per-account pricing rather than a basis-point-based fee. This made it particularly appealing to advisors charging flat fees (e.g., subscription fees) themselves, whose bps-based TAMP costs for investment management alone could eventually eclipse their own flat advisory fee altogether if their clients’ affluence and accounts grew high enough.

In this context, it’s notable that the news broke that GeoWealth acquired First Ascent, representing a marriage between GeoWealth’s homegrown TAMP technology and open-architecture investment model and First Ascent’s investment- and service-oriented model.

From GeoWealth’s perspective, the deal expands the offerings it can provide beyond its TAMP technology and access to model portfolios by integrating First Ascent’s investment expertise and concierge investment consulting services. GeoWealth also adds experienced TAMP leadership to its ranks with First Ascent CEO Scott MacKillop, who has worked in leadership roles for various investment management technology platforms going back to the late 1990s. For First Ascent, the main benefit of the combination is to bring in GeoWealth’s in-house technology to allow it to better scale its own high-touch offering and keep its costs down by eliminating third-party portfolio management tools. This is especially important given its flat-fee model that stays capped even as assets on the platform grow such that big clients can’t cross-subsidize smaller clients. So First Ascent has to stay tech- and cost-efficient and profitable on every client it serves.

The press release announcing the deal states that First Ascent will continue to operate as an independent subsidiary of GeoWealth. First Ascent’s services and flat-fee pricing will still be available for its advisor clients, who will also now have access to GeoWealth’s technology platform. Firms on GeoWealth’s platform will presumably have access to First Ascent’s in-house investment models, and if they decide the flat-fee approach of First Ascent makes more sense for them, they could make the switch with minimal disruption given that both platforms are now based on the same technology.

Even before the deal, GeoWealth was a strong up-and-comer in the investment management technology category, with about $7.5 billion in assets under management and $20 billion in total assets on its platform. Presumably, this represents a mix of assets managed directly by GeoWealth’s TAMP and those managed by advisors using GeoWealth’s technology. The deal adds another 80 advisors and $1.4 billion in AUM from First Ascent though First Ascent’s flat-fee model makes it unclear how much revenue that additional $1.4 billion of AUM supports.

Ultimately, though, the real significance of the deal may be more both the ongoing trend of TAMPs and RIA custodians to in-house their own portfolio management technology (presenting an ongoing threat to third-party portfolio management tools), and also the future opportunity it represents in offering a combination of basis-point and flat-fee models built to scale on the same technology. This leaves GeoWealth and First Ascent uniquely positioned among TAMPs to serve a wider range of advisors who may see advantages in either model, particularly as increasing numbers of advisors are themselves adopting subscription, retainer and other flat-fee models.

The earliest financial planning software was built as a retirement projection tool for people still accumulating savings during their working lives. The software could calculate an estimate of a client’s retirement savings picture based on their current trajectory versus where they needed to be to reach their goals and demonstrate any gaps. The advisor could then sell them a product (e.g., a mutual fund or life insurance policy) to help make up the shortfall. While further iterations of financial planning software grew more sophisticated over time — for example, by incorporating cash flow-based planning and Monte Carlo analyses to provide more realistic retirement planning scenarios — the software still tended to focus primarily on projecting the growth of retirement portfolio values over time. Other aspects of the client’s retirement picture were painted with a fairly broad brush, using rough assumptions for elements like Social Security income and tax rates on retirement withdrawals with few tools to actually improve them.

As financial planning grew more advice-centric and less product-centric, there was increased demand for planning tools that could accomplish what traditional financial planning software couldn’t, particularly in the domains of Social Security optimization and tax-sensitive portfolio drawdowns. These are two ways in which advisors found they could add value by demonstrating to clients how they could boost their retirement income by choosing the right Social Security claiming strategy and by reducing the taxes paid on their retirement assets by managing their tax brackets (e.g., by making strategic Roth conversions to fill up lower tax brackets).

One of the early leaders in providing these specialized planning tools was Retiree Income, founded in 2008 by Bill Meyer and Dr. William Reichenstein. With Reichenstein’s academic research and Meyer’s experience in software product design, they built tools to easily model relatively complex Social Security claiming strategies for both single retirees and couples, and to demonstrate withdrawal strategies incorporating Social Security as well as optimized asset allocation and sequence of withdrawal methods. Notably, the company developed both an advisor and a consumer version of its tools, releasing SSAnalyzer and Income Solver for financial advisors. It is mainly geared toward analysis of different strategies, with the advisor left to recommend and implement the strategies themselves, with Social Security Solutions and Income Strategy as direct-to-consumer tools with an option for advice on top of the analytical tools for DIY-preferring clients.

It's notable, then, that news came out in March that parent-company Retiree Income was being purchased by asset management giant T. Rowe Price. The deal is somewhat surprising given that Retiree Income’s tools are well-known and popular among advisors, with Kitces Research on AdvisorTech showing SSAnalyzer and Income Solver having the highest adoption rate in their respective software categories. T. Rowe Price is primarily known for its roots selling direct-to-consumer mutual funds and managing employer retirement plans — meaning that in all likelihood, it’s the consumer versions of Retiree Income’s tools that T. Rowe price is targeting through this deal, rather than its highly regarded advisor tools. As T. Rowe Price’s own press release of the deal highlights, “the software will be an important part of our [T. Rowe Price] strategy to build personalized retirement income solutions and services for our [T. Rowe Price] clients.”

To that end, it seems likely that T. Rowe Price will use the heft of its resources to invest in Retiree Income’s consumer tools and distribute them via its direct-to-consumer channels and very possibly its employer retirement plan services as well. From the advisor standpoint, while SSAnalyzer and Income Solver reportedly will still be available, it’s hard to imagine that T. Rowe Price will direct the same level of attention and investment their way as the consumer tools. After all, as a $1.3 trillion asset manager, a B2B tech solution for advisors won’t grow T. Rowe Price’s revenue in any substantial way, at least compared to the ability to reach literally millions of consumers who already use T. Rowe Price directly through its newly acquired retirement income software tools for consumers.

So while it’s good to see the successful exit of an AdvisorTech provider — particularly one that built not one, but two sophisticated and well-regarded solutions in the advanced planning domain — the acquisition ultimately raises the question of how much adoption specialized planning tools can expect among advisors before they need to find other channels for growth. While SSAnalyzer and Income Solver may have led their categories in adoption rate in our Kitces AdvisorTech Research, the reality is that only so many advisors will choose to employ specialized tools beyond their existing financial planning software, which leaves specialized tools only so much room to grow. Retiree Income was fortunate in also developing direct-to-consumer versions of its tools that caught the eye of a giant asset manager interested in investing to distribute those tools further but most specialized planning tools don’t have a feasible direct-to-consumer path.

Strategically, then, the T. Rowe Price acquisition of SSAnalyzer and Income Solver highlights how specialized planning tools either need to find a way to be more directly integrated to financial planning software so advisors don’t have to make an either-or choice, sell themselves to a financial planning software provider or face the risk that an acquirer comes in and repurposes their software to its own goals. In the end, it’s very challenging to develop such a great specialized tool that advisors are willing to adopt it on top of the other financial planning software they already use.

Advisory firms have a natural tendency to grow. Client retention rates for a typical firm average well over 90%, meaning that once a firm gets over the initial hurdles of growing to a point where it can sustain itself, even a relatively modest growth rate thereafter can lead to needing multiple advisors and support staff to attend to all the needs of the firm’s clients over time.

But as a firm grows, its operations can get messy. With more clients, accounts and employees, there are more processes that must get handed back and forth between multiple staff members, bringing the potential for hangups and miscommunication when everyone isn’t on the same page. With the independent RIA model having taken hold in the last 20 years or so, many firms that have seen steady growth over that time — which may originally have run lean solo practices — are now increasingly in that messy middle stage of learning how to coordinate workflows and handoffs across multiple employees serving clients as a team.

In that context, there has been increasing demand for tools that can help advisory firms manage their multistaff, multisystem workflows as they increase in scope and complexity. To some extent, CRM software has stepped in to fill that need, with providers such as Redtail and Wealthbox launching workflow capabilities within their platforms that leverage the client information already housed within their software. Larger advisory firms are increasingly migrating toward Salesforce, which has long had deeper workflow and automation capabilities, at least for the advisory firms that can budget enough for Salesforce consultants or overlays to program the platform to their firm’s specific workflow needs. But most providers of CRM software, which traditionally served as a digital Rolodex built primarily for handling sales opportunities, haven’t yet treated workflow management as a core function of their products (or in the case of Salesforce, haven’t done so in a manner that is cost-effective for small to midsize advisory firms), and so have largely failed to provide tools that can handle the increasingly complex workflows and task management functions needed for a modern, multi-employee (but not huge enterprise) advisory firm.

As a result, workflow support has been an emerging and growing category of the Kitces AdvisorTech Map in recent years, with tools such as Docupace, Hubly and Cognicor providing various forms of solutions that overlay and integrate with advisors’ existing CRM platforms to streamline back-office functions. Such functions include opening accounts, moving money and scheduling meetings, as well as increasingly supporting middle- and front-office functions like drafting meeting agendas, reviewing planning items, flagging topics for review, and managing all the documents that go with the process along the way.

In this context, it’s notable that Benjamin, one of the early entrants into the emerging workflow management category, announced in March that it was shutting down operations. Launched in 2019 after being developed in-house at the RIA firm of its founder, Matt Reiner, Benjamin was relaunched in 2020 as “the world’s first AI assistant created for advisors by advisors.” But despite garnering industry media buzz for its pioneering AI tools — winning a Wealth Management Industry Award for business support systems and receiving an initial round of seed funding plus additional investments from the Scratchworks fintech accelerator competition — Benjamin apparently found itself unable to achieve substantive traction with advisors themselves, ostensibly resulting in a struggle to achieve breakeven cash flow after nearly four years and shutting down after not being able to find additional capital to otherwise keep itself going.

As the overall growth of the workflow management category shows, Benjamin’s demise likely isn’t the result of a lack of desire among advisors for workflow support. The growth of both workflow capabilities in CRM systems like Redtail and Wealthbox, and more substantively the rising traction of platforms like Hubly, shows that advisors are increasingly even willing to pay to improve their workflow capabilities as their needs grow above and beyond what their CRM can provide. Ironically, this is often at a cost that’s higher than the underlying expense of the CRM software itself, suggesting that CRM providers may still be under-investing in workflow support if competitors can charge more than they do for just one key feature.

At its core, however, it appears that Benjamin’s demise may be less about advisor desire and willingness to pay for a workflow support engine, and more about advisor resistance to how Benjamin leaned heavily into marketing the AI that drove its technology. On one hand, it makes it ironic that Benjamin had to shut down just as the recent buzz around AI reached a high point, but on the other hand, it illustrates how the newness of AI still creates some hesitancy in advisors who don’t yet trust the technology enough to hand over the keys to their operations to it. So as other providers like Cognicor and FP Alpha emphasize their AI-driven tools, it remains to be seen whether doing so is really helping their sales pitch to advisors, or whether advisors really just want a tool that solves their problems while being less interested in how the technology actually works. In other words, while advisors may jump at a solution that automates workflows and assigns tasks automatically, they might be less eager if they find out the solution uses AI to perform those functions. Not to mention that while AI-based chatbots may be a hot topic of conversation, it’s not actually clear whether a chatbot interface actually improves the user experience for advisors over one that focuses on how advisors already prefer to use their technology and manage their workflows as Hubly has done.

Benjamin notwithstanding, however, there are clearly opportunities today for technology that can augment the workflow capabilities of advisors’ CRM platforms, and in the long run it seems inevitable that elements of AI will weave their way into the technology as well. Still, the core question when it comes to workflow support in particular is whether the rising demand for tools will spur CRM providers themselves to step up their capabilities (either by building the tech themselves, or by acquiring one of the increasing number of workflow support providers out there) to save advisors the often substantial cost of a third-party overlay — or whether workflow support will become a standard and necessary stand-alone tool for advisors as they grow in size and scale.

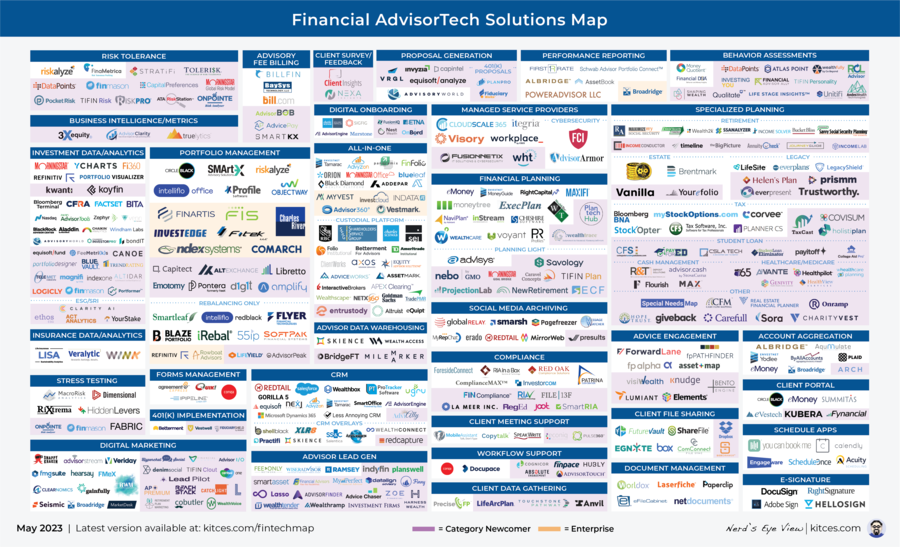

Five years ago, a boom was emerging in advisor technology. Robo-advisors had arrived a few years prior and, while they didn’t disrupt the human advice industry as many feared, they did leave a legacy by demonstrating how clunky and old a lot of advisor interfaces had become. This spurred a major cycle of investment from advisor platforms that suddenly felt a renewed sense of urgency to catch up. Additionally, in those years the rise of fintech — and PE firms that invest into it — began a wave of AdvisorTech acquisitions, including, among many others, Principal Financial acquiring RobustWealth, Franklin Templeton acquiring JemStep, Northwestern Mutual acquiring LearnVest and perhaps most notably, Fidelity buying eMoney for nearly $250 million. This demonstrated an opportunity for founders to build in the AdvisorTech space with the possibility of a successful financial exit as industry incumbents increasingly sought to acquire and bring new technology in-house. Adding more fuel to the fire, persistent low interest rates further amplified the amount of venture capital money looking to invest in the next big fintech acquisition.

As a result, by the mid- to late 2010s there was a plethora of new startups emerging, while mergers and acquisitions activity combined other providers or absorbed newer solutions back into established incumbents. This led to a challenge for advisors who wanted to take advantage of all this new technology: how to keep track of all of the new technology coming out, navigate which tools solved different pain points in various ways, and figure out how to fit all of the tools together so that managing the proliferating advisor technology choices didn’t become a separate job unto itself.

In an attempt to create a high-level overview of the tech landscape and make sense of who all the players were, we launched the Financial AdvisorTech Solutions Map (originally called the Financial Advisor FinTech Solutions Map) in April 2018 and have updated the map every month since. The purpose of the map was twofold:

This second point was becoming increasingly necessary in an environment where more and more software providers were providing additional features and capabilities to their tools and trying to do everything for everyone, which made it hard to get a sense of what they really did as their core capability. For instance, although many software solutions included a client portal or document-sharing vault, few advisors would buy them just for the portal function. Similarly, eMoney offered advisor-branded marketing tools, but few would use eMoney for marketing unless they first used it for financial planning. Orion acquired Advizr to offer financial planning software, but few would use Orion Financial Planning unless they first used Orion for portfolio management to begin with.

The original AdvisorTech Map from April 2018 had 188 different software solutions, reflecting how overwhelming the range of options in AdvisorTech was already becoming at that time. Fast forward to April 2023, and there are now 409 different software solutions crammed into the one-page map. To be fair, some additions to the map are likely a result of companies we missed in the initial launch and added in the months thereafter. The overwhelming bulk of the additions simply reflect the continuing boom in AdvisorTech itself, with the total number of solutions more than doubling. The more-than-doubling of different solutions itself understates the amount of new software that has come along during that time, since many tools have either disappeared or been folded into other companies during that time as well. In fact, the map itself became so dense with company logos of increasingly small size that were harder and harder to click, that we last year launched our Kitces AdvisorTech Directory to provide an even more navigable interface to find new solutions and help advisors build their own AdvisorTech stack.

But even as use of our AdvisorTech Directory has grown, the Kitces AdvisorTech Map has become a thing unto itself. It’ a navigational aid for advisors to find technology, the punchline to a joke about the dense proliferation and sometimes overwhelming number of choices that advisors now have and a visual statement of the evolution of the AdvisorTech itself as the monthly updates of the map document changes to the landscape. Some highlights of these AdvisorTech evolution trends over the past five years include:

The shifts in the AdvisorTech landscape also reflect the ways in which advisory firms themselves are evolving: the increase in depth and breadth of advice to deepen the advisor’s value proposition beyond just portfolio management; the challenges of marketing and growth in a competitive environment where it’s no longer sufficient to differentiate solely on being a fiduciary or offering comprehensive financial planning; the workflow and management challenges that arise as firms grow and accrue clients, assets, revenue and staff and need to become more efficient to scale further; and the relative diminishment of investment-related tools — which, while still present in most advisors’ tech stacks, have undergone a wave of consolidation and are continuing to experience the greatest pricing pressure as the cost of providing asset-allocated portfolios (and willingness to pay for tech to support it) has plummeted in the robo-advisor era.

Looking forward, we expect to see a few of these trends continue. Advice engagement and workflow support tools will likely continue their growth as relatively new categories with plenty of room for new adoption, along with other emerging categories that could see further growth include data warehousing (as larger advisor enterprises seek to not only integrate their cross-system workflows but centralize all of their business and client data), and client meeting support (particularly as AI tools such as ChatGPT pick up steam and present the opportunity to automate many of the time-consuming tasks surrounding client meetings, like writing follow-up emails and assigning tasks for next steps). On the other side, investment management technology seems likely to consolidate further as custodial platforms like Altruist gain share with their own in-house technology, with other custodians potentially following suit. Other waves of consolidation may follow such as in the Risk Tolerance category, where no one has yet managed to dislodge the now dominant Riskalyze (now Nitrogen). There’s the Behavioral Assessments category where, despite research showing evidence of the benefits of behavior-based advice, few advisors have been willing to wade very far beneath the surface of client behavior and psychology or to pay for solutions for doing so.

But whatever the path that the evolution of AdvisorTech takes from here, we’re committed to continuing to help advisors navigate the choices and in the process, document its ongoing progress and evolution. It’s been exciting to see the Kitces AdvisorTech Map pop up in other contexts, such as corporate strategy presentations and even in venture capital pitch decks — and to appreciate that what started out as a navigational aid, and branched out into a directory as the map itself got crowded enough to test the eyesight of its readers, has become a kind of visual commentary on the AdvisorTech landscape itself. This becomes all the more apparent when watching the evolution of the map in its 60 monthly iterations over the last five years, as illustrated below.

In the meantime, we’ve rolled out a beta version of our new AdvisorTech Directory, along with making updates to the latest version of our Financial AdvisorTech Solutions Map with several new companies, including highlights of the Category Newcomers in each area to highlight new fintech innovation.

So what do you think? Should the SEC scrutinize RIAs’ advertisements of their tax-loss harvesting practices in the same way as any other investment strategy? Would you rather be able to choose the individual portfolio management solutions that you like the most, or live in a walled garden where the choices are fewer but everything is built to just connect and work all by itself? Would you trust an AI-driven solution to handle your core business processes and pay to do so? How far do you need to zoom in on the AdvisorTech Solutions Map to be able to read it all?

Michael Kitces is the head of planning strategy at Buckingham Strategic Partners, co-founder of the XY Planning Network, AdvicePay and fpPathfinder, and publisher of the continuing education blog for financial planners, Nerd’sEye View. You can follow him on Twitter @MichaelKitces.

Ben Henry-Moreland is senior financial planning nerd at Kitces.com, where he researches and writes for the Nerd’s Eye View blog. In addition to his work at Kitces.com, Ben serves clients at his RIA firm, Freelance Financial Planning.

Eliseo Prisno, a former Merrill advisor, allegedly collected unapproved fees from Filipino clients by secretly accessing their accounts at two separate brokerages.

The Harford, Connecticut-based RIA is expanding into a new market in the mid-Atlantic region while crossing another billion-dollar milestone.

The Wall Street giant's global wealth head says affluent clients are shifting away from America amid growing fallout from President Donald Trump's hardline politics.

Chief economists, advisors, and chief investment officers share their reactions to the June US employment report.

"This shouldn’t be hard to ban, but neither party will do it. So offensive to the people they serve," RIA titan Peter Mallouk said in a post that referenced Nancy Pelosi's reported stock gains.

Orion's Tom Wilson on delivering coordinated, high-touch service in a world where returns alone no longer set you apart.

Barely a decade old, registered index-linked annuities have quickly surged in popularity, thanks to their unique blend of protection and growth potential—an appealing option for investors looking to chart a steadier course through today's choppy market waters, says Myles Lambert, Brighthouse Financial.