The May edition of the latest in financial #AdviserTech kicks off with the big news that Orion Advisor Services is acquiring Redtail CRM, increasingly positioning Orion as the all-in-one solution to compete against Envestnet with its combination of financial planning (Advizr vs. MoneyGuide), performance reporting (Orion vs. Tamarac), and now CRM (Redtail vs. Tamarac CRM), paired with its back-end TAMP solutions (Brinker and Orion’s model marketplace vs. Envestnet’s PMC and its SMA platform). In the near term, it’s more likely that Orion and Redtail will simply focus on trying to cross-sell their respective services to the users of the other, given what was only a 20% to 30% overlap in existing advisers already using both while still respecting the majority of each user base that may not be looking to switch and will remain with their current CRM or portfolio management solution.

From a broader industry perspective, though, the real significance of the Orion-Redtail deal may simply be a sign of the ongoing bullishness of growth for AdviserTech more broadly. Redtail’s valuation was likely buoyed by Wealthbox’s recent Series B, and Orion’s potential initial public offering valuation in the future may be boosted by rumors that a PE firm may take Envestnet private. In other words, the Orion-Redtail deal may not necessarily be one of a great unified vision of a single all-in-one solution for all advisers — though few would likely object to seeing greater integrations between the two — but simply a financial opportunity to attempt to make the whole worth more than the sum of the parts.

From there, the latest highlights also feature a number of other interesting adviser technology announcements, including:

• Advyzon launches its Quantum Rebalancer to shore up its hold on small-to-midsize investment-centric firms that want to use Advyzon for everything (excluding financial planning).

• RightCapital launches a new one-page Financial Plan Snapshot feature that highlights the gap in financial planning solutions for clients after their initial plan is done.

Read the analysis about these announcements in this month's column, and a discussion of more trends in adviser technology, including:

• Vanguard launches a new partnership with American Express to pay the same 25 basis point promoter fees that have become common in the independent RIA channel as well, highlighting the ongoing extraordinary cost of lead generation.

• SimplyEasier launches a new fee-for-service billing solution as more advisers continue to explore non-AUM business models.

• Schwab gears up for the launch of its new Personalized Indexing solution at a 40-bps cost that may actually offset most or all of the tax-loss harvesting benefits it purports to generate.

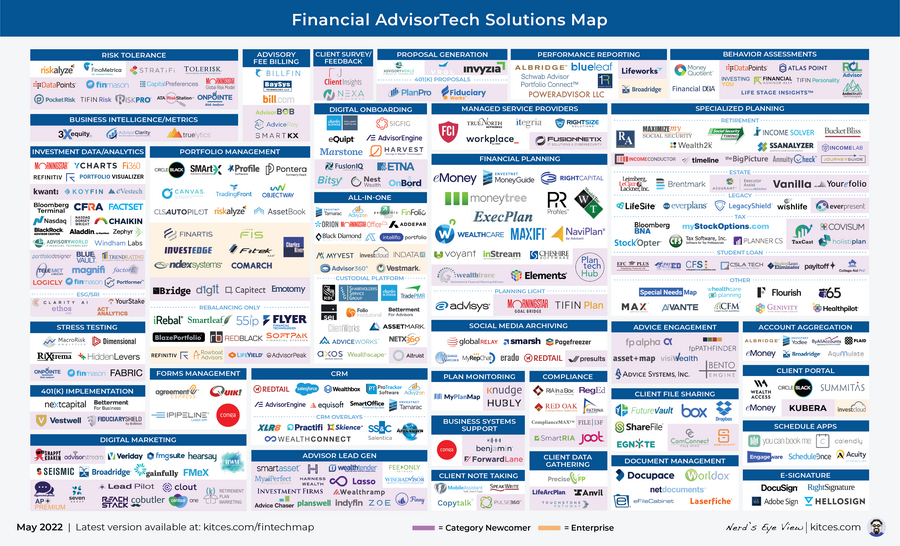

In the meantime, we’ve also launched a beta version of our new Kitces AdviserTech Directory to make it even easier for financial advisers to look through the available adviser technology options to choose what’s right for them.

Be sure to read to the end, where we have provided an update to our popular Financial AdviserTech Solutions Map!

AdviserTech companies that want their tech announcements considered for future issues should submit to [email protected]!

The financial advice industry is a highly fragmented industry where even the largest enterprises that aggregate advisers (e.g., LPL Financial) have barely more than 6% market share of the nearly 300,000 financial advisers. “National” wirehouses have only 3% to 4% market share in terms of adviser head count, and the overwhelming majority of all advisers operate as solo practitioners or small firms with just a handful of employees. From the technology perspective, this means the buying preferences of advisory firms are similarly fragmented, as each operates on a slightly different basis, and wants or prioritizes slightly different features. That has both aided the proliferation of AdviserTech solutions (as 300-plus AdviserTech companies each find their own niche adviser segment to serve), but also the fragmentation of AdviserTech, as all those companies try to figure out how best to integrate to one another.

As a result, in recent years there has been an emerging trend toward AdviserTech consolidation — not just for the sake of business efficiencies and economies of scale, but also for the idea that when a platform has “the full suite” of adviser technology tools to offer under one umbrella, the tools can be more deeply integrated. This has led to a growing number of firms expanding their features into adjacent categories or outright acquiring other vendors in those areas to offer a growing number of “all-in-one” technology platforms for advisers.

This made it not entirely surprising that in April, Orion Advisor Services (the market share leader for portfolio management and performance reporting, according to the latest Kitces AdviserTech Study) announced the acquisition of Redtail CRM (the market share leader for adviser CRM in the Kitces AdviserTech Study). The blockbuster deal allows Orion to bring all three of the main components of the adviser technology stack — portfolio management, CRM and financial planning (thanks to Orion’s prior acquisition of Advizr) — under one roof, second only to Envestnet and its Tamarac (portfolio management and CRM) + MoneyGuide offering.

Yet, while many in the industry have viewed such consolidations as almost inevitable in an age of PE-funded mergers and acquisitions and the ongoing trend toward all-in-one platforms, in practice the Orion-Redtail merger is much more nuanced about what synergies, exactly, can be expected in the deal, and what may have really driven it in the first place.

For instance, the underlying premise of Orion bringing Redtail under its umbrella as a true all-in-one may not actually be so appealing. As Orion and Redtail themselves note, their current user overlap is “only” about 20% to 30% of shared firms, and on average advisers change their CRM systems not even once per decade. This means that for the foreseeable future, Redtail will have to actively support non-Orion users, and Orion will have to actively support non-Redtail users. Expect to see Redtail continue to be available on a stand-alone basis for a long time to come, and expect continued pressure on both Redtail and Orion to support outside integrations beyond just the connections to one another. This means advisers using other solutions, from Wealthbox to Salesforce CRM as Orion users, or Black Diamond or Tamarac as Redtail users, shouldn’t need to be worried about switching anytime soon. While Advizr was more directly rebranded and tucked into Orion, that was because it had a very limited adviser user base in the first place. Instead, Orion’s acquisition of Redtail is more akin to Hidden Levers, which already had a substantial non-Orion user base and continues to be available to them.

On the other hand, the fact that 70%-plus of each company’s user bases are not already using the other creates a more direct opportunity for cross-selling between the two, offering incentives for Redtail users to switch to Orion (e.g., from Black Diamond or Tamarac), and for Orion users to switch to Redtail (e.g., from Wealthbox or Salesforce). In fact, the 2021 Kitces AdviserTech study showed that advisers are more willing to leave their performance reporting tools than their CRM systems. This suggests that Orion may have a more direct growth path simply by getting an opportunity to market itself more directly to Redtail users if Orion can roll out a more scaled-back limited version of Orion at a lower price point to small Redtail users, and fend off the growing threat from Advyzon and its portfolio-management-plus-CRM solution.

At the same time, Redtail itself has primarily dominated the small-to-midsize adviser marketplace, including independent RIAs and the independent reps of broker-dealers who can choose their own technology, with more limited adoption in larger ensemble enterprises (i.e., mega-RIAs with dozens or hundreds of advisers with shared ownership), where Salesforce has the highest market adoption and Redtail’s one-database-per-adviser structure has been more challenging to manage, especially given that Redtail has also been more limited in building out its role- and permission-based functionality that larger more complex enterprises require (an area where Orion is stronger and may be able to help).

Arguably, though, the biggest driver of the Orion-Redtail deal may simply be one of financial engineering. Earlier this year, CRM competitor Wealthbox announced its own $31 million Series B round at a valuation that was rumored to be as high as five times to six times revenue. This may have helped to peg Redtail’s valuation higher than it was in the past. At the same time, it’s also been rumored that Orion’s merger and acquisition wave of the past several years — from Advizr to Brinker to Hidden Levers and now Redtail — is positioning the company to IPO as an Envestnet competitor just as Envestnet is rumored to be entertaining bids to go private (at what again would be a premium to its current market-traded valuation). This means Redtail may be on a path to a rapid double-boost of its own valuation, lifted first by the hunger for adviser CRM, (per Wealthbox’s valuation), and then also by the potential of a valuation pop for an Orion IPO just as Envestnet may see its own valuation rise in a deal to go private. And it helps to explain why Redtail CEO Brian McLaughlin finally chose to sell after rebuffing acquisition inquiries for more than a decade, along with apparently choosing to take “a good part” of his Redtail sale in Orion shares.

In turn, the sheer financial and economic opportunity of Orion-Redtail may clarify why Redtail wasn’t acquired by Riskalyze as the two companies (and their CEOs) have long shared synergies, a common hometown (Sacramento, California), and even a common board (Redtail’s McLaughlin was on the Riskalyze board). However, Orion’s prospective path to an IPO exit likely put more buying power on the table for Redtail at a valuation that Riskalyze may simply not have been able to match. (And with the Orion deal, McLaughlin has now left the Riskalyze board altogether).

The key point, though, is simply to recognize that while there are clearly some interesting long-term potential synergies between Orion and Redtail to become more integrated over time, and some nearer-term cross-selling opportunities to attract the 70%-plus of each software’s users that don’t use the other, sometimes the biggest driver of industry mergers and acquisitions is simply the economics of rising valuations as private equity dollars continue to roll through the industry. Stated more simply, sometimes the most prudent thing to do is to get selling while the selling is good.

Over the past 20 years, the financial adviser business model has increasingly shifted from the sale of commission-based mutual funds and other financial products to the more holistic management of a fee-based portfolio. This has led to a fundamental shift in the technology that advisers use to support their investment activities, from investment analytics tools that reported on the performance of those pooled investment vehicles, where the report was the same for every client that owned the same fund, to solutions that can provide reporting on the individual performance of the client’s entire portfolio, thus necessitating household-level reporting that was different for each client.

At the same time, though, the shift to more client-specific individually managed portfolios began to de-scale the otherwise efficient model of mutual fund sales, spawning an entirely new category of software — “rebalancing” tools. This eventually became a broader “model management” solution to help advisers more scalably manage individual client portfolios by mapping them to a series of models (e.g., from conservative to aggressive) that the adviser could offer to clients, and then doing client-level reporting on each based on their individual portfolio, its own customizations, and the timing of the client’s specific cash flows in and out of the portfolio.

For nearly a decade, from the mid-2000s to the mid-2010s, the two ran in parallel, with rapid growth of both rebalancing and other portfolio management tools alongside the rise of performance reporting software. But in recent years, the two began to merge, as ultimately rebalancing and model management software has to pull its data from somewhere to know what needs to be traded or managed. The rising depth of integrations between the two somewhat inevitably led to their consolidation, as platforms from Orion to Tamarac to Black Diamond to Riskalyze to Panoramix to Addepar and more all built or acquired rebalancing tools to expand their performance reporting solutions.

Now, more recent upstart Advyzon has announced that it has built and rolled out its own Quantum Rebalance, pivoting itself from a performance reporting solution with an embedded CRM system into a more all-in-one portfolio-management-plus-CRM offering, as the stand-alone performance reporting category continues to shrink.

From the Advyzon perspective, the move makes sense — shifting from performance reporting to a broader portfolio management solution with a native rebalancer has already been the natural evolution of similar platforms. As more independent rebalancing tools have been acquired (e.g., AdvisorPeak, Blaze Portfolio, Portfolio Pathway, RedBlack, TradeWarrior and tRx have all been bought in the past seven years), most providers are now simply building their own rebalancers themselves as Advyzon did. In addition, having the adviser on Advyzon’s own trading tools ostensibly will make it easier for the adviser to transition to Advyzon’s recently launched investment management TAMP offering, providing a clearer pathway for Advyzon to further upsell its outsourcing solution.

From the overall industry perspective, yet another performance reporting solution expanding into the all-in-one category isn’t necessarily notable. It’s a trend that has been underway for many years but should help cement Advyzon’s position among its niche of small-to-midsize independent firms that historically had to rely on their custodian’s or broker-dealer’s own platform tools and should appreciate a more deeply integrated solution directly within Advyzon (especially given that Advyzon was already a strong up-and-comer in the recent Kitces AdviserTech study. with one of the highest scores in both the CRM and performance reporting categories).

When robo-advisers first launched a decade ago, they pledged to eradicate the human financial adviser by constructing client portfolios at just one-fourth of the going rate charged by financial advisers, offering a diversified asset-allocated portfolio for just 25 basis points with far-lower minimums than the typical adviser. Yet in the decade since, nearly all the robo-advisers are gone, while human financial advisory firms have continued to grow. In the end, it turns out that the real reason financial advisers charged a 1% fee wasn’t because it was so expensive to build and manage client portfolios, but because it’s so expensive to get those clients in the first place.

In fact, more recent Kitces Research on adviser marketing has shown the average financial adviser spends $3,119 to acquire a single client through a combination of hard-dollar marketing costs and the time investment made by the adviser. This means advisers “have to” set minimums like $250,000 of assets and charge a 1% AUM fee, just to come close to breaking even on their acquisition costs after the first year. Even then, it will take three to five years for the relationship to actually be profitable given typical advisory firm margins. This means robo-advisers effectively brought an operations solution to a lead generation/client acquisition problem. That’s why most weren’t actually able to attract a sufficient number of clients to scale up, even with the outside capital of venture capital or PE firms.

This dichotomy of the cost to service clients versus the cost to acquire them was brought into stark relief when Vanguard and its Personal Advisor Services announced a stunning client acquisition partnership with American Express, for which Vanguard will discount its standard rate of 30 bps for access to its human CFP advice solution down to just 25 bps as an incentive deal for American Express customers. AmEx itself will charge an additional25 bps as a promoter fee for facilitating the introduction. In other words, AmEx will effectively be reselling Vanguard’s 30 bps human financial advisers for 50 bps, for which AmEx will receive half the fee just for the introduction.

From an overall economics perspective, the 25-bps revenue-share to American Express is remarkably similar to the going rate for client referrals in the RIA channel, where 25 bps was historically the fee that RIA custodians charged to RIA for referrals. A growing number of third-party lead generation platforms have similarly been charging 15 bps to 25 bps as a revenue-sharing fee for new clients. Although for the typical adviser, that 25 bps comes out of an aggregate fee of 1%, amounting to 25% of the fee, while in Vanguard’s case the 25 bps solicitor fee doublesthe cost of advice for AmEx customers.

This helps to highlight just how dramatic the impact of client acquisition costs really are when it comes to the cost of financial advice, and how robo-advisers charging just 25 bps all-in failed to account for how client acquisition costs were the real limiter on access to financial advice. The Vanguard-AmEx deal also emphasizes how, notwithstanding the meteoric rise of Vanguard’s Personal Advisor Services platform — which in barely eight years has grown to more than $250 billion of AUM — Vanguard has still grown almost entirely by converting existing Vanguard clients into clients of its adviser services platform. Now, when Vanguard has to look beyond its existing client base to grow, its costs are suddenly rising significantly just to account for the impact of client acquisition costs. Also Vanguard, despite the power of its brand, is still paying more or less the same rate for lead generation as any other independent financial adviser.

In the end, though, the key point is simply to understand how dramatic a role client acquisition costs really play in the cost of financial advice. The Vanguard-AmEx deal further emphasizes why “lead generation” services like SmartAsset, Zoe Financial, IndyFin, WealthRamp and the like have become one of the hottest categories of AdviserTech growth. After all, the average financial adviser spends barely 12% of their time actually managing client portfolios, but nearly 20% of their time trying to find new clients. Advisor technology has spent the past 20 years making the delivery of financial advice and the management of client portfolios more efficient and less costly to deliver, but has made remarkably little progress on bringing down the cost of generating new clients in the first place.

The process of analyzing a client’s long-term financial trajectory, whether they’re on track for their goals or not, and what actions they need to take, or not take, to stay or get on track, is complex. This is why comprehensive financial planning software was one of the first technology tools to be developed with the rise of computers in advisory firms nearly 40 years ago. Over that time, planning software has gone through several iterations, from more in-depth cash flow modeling, to more straightforward goals-based projections, to pulling in real-time data updates via account aggregation, but all with the same output — “the comprehensive financial plan” — a document that was often dozens of pages long and could be delivered to the client with a hearty thunk as it was placed on the table.

The lament from the adviser community, though, has been that while we all produce such thorough comprehensive financial plans — for which clients may willingly pay several thousand dollars — the spine of the plan is rarely cracked again after it’s first delivered. For many clients, the plan is so long it can’t even be fully delivered in a plan presentation meeting without clients’ eyes glossing over. As advisers, we typically rationalized that even if the client didn’t want to read the entire plan, they still needed to see that the planning analysis had been done in order for the adviser’s recommendations to be deemed credible in the first place. Viewed another way, while clients may ultimately just focus on the action items and recommendations captured on only one or two pages of the plan, it was hard to imagine the client would really pay the entire financial plan fee for just those one or two pages.

Yet the fact that the client may be presented with the whole comprehensive plan in the initial planning meeting and then never view it again arguably just highlights the disconnect between the upfront financial plan process, and the ongoing delivery of financial planning in the months and years that follow, where the focus is more on the incremental milestones — how has the financial situation changed since the last meeting, what’s been done and what should be done next?

In that vein, over the past year, there’s been a renewed focus on creating a one-page financial plan for clients, not necessarily to replace the initial upfront plan, but as a tool for periodic check-ins with ongoing clients to demonstrate the adviser’s ongoing value. The reality is that it may really take a lot of detail to do those initial financial planning projections and account for all the relevant factors. However, an incremental look at “what’s changed since our last meeting” really is more conducive to a single-page summary to ensure the client remains on track.

So it was notable that financial planning software maker RightCapital debuted a new Financial Plan Snapshot page that allows financial advisers to select from a series of financial planning widgets, along with customizable text boxes, to capture their own One Page Financial Plan snapshots for their clients.

RightCapital isn’t the first to try to produce a single-page summary of the financial plan, as most other financial planning software providers have a similar document available among their options for output that can be printed for the client. eMoney has long been popular for its client portal that leverages account aggregation to give clients a real-time-updated snapshot of their current financial situation.

Instead, what arguably makes the RightCapital Snapshot unique is its ability to incorporate the non-numerical aspects of the financial plan, from writing out the client’s core values or their statement of financial purpose, to capturing their recent to-do’s and upcoming action items to work on. In other words, it’s not about a one-page financial plan as a singular one-page deliverable for the upfront plan, but its use as a tool to facilitate client accountability in the ongoing planning process that makes it unique.

From the competitive perspective, though, it’s notable that it wasn’t MoneyGuide or eMoney that developed such an immediately popular one-page financial plan feature, but RightCapital, which includes a core feature of customizable text boxes that has long been a common request of independent financial advisers. Kitces Research shows the majority of advisers are having to use Word and/or Excel to supplement the limitations of their financial planning software. It’s something that independent broker-dealers have long objected to as adviser-level customizations create concerns from centralized compliance departments that don’t want to have to review each adviser’s individual text boxes. This means RightCapital may be starting to out-iterate MoneyGuide and eMoney on new features by staying closer to the end adviser community, while the latter have road maps that are increasingly beholden to the less innovative demands of broker-dealer enterprises that are still trying to catch up in the products-to-advice shift.

The key point, though, is simply to recognize that what has historically been called financial planning software is really more of an “upfront financial plan” creator, while the true needs of ongoing financial planning to support the next 29.5 years of a 30-year client relationship after the first six months of crafting and delivering their financial plan are different. RightCapital’s focus on what actual advisers are doing to demonstrate value to their ongoing clients is allowing it to iterate on the features of true financial planning software faster than their competitors.

Over the past 20 years, the advisory business has experienced a fundamental shift in its business model, with the ongoing wind-down of commission-based sales of mutual funds and insurance, and the rise of the assets-under-management model and its AUM fee. But the reality is that the shift in the adviser business model of the 2000s and 2010s was driven by a preceding shift in technology in the 1990s — when Schwab Advisor Services launched the first RIA custodial platform that made it possible to bill a client’s advisory account for an AUM fee. This eventually was mirrored by other platforms, including Fidelity and Ameritrade and later Pershing, fueling the rise of the RIA, and more recently, fee-based brokerage, by that AUM-billing technology.

In recent years, a similar shift has begun with respect to the next adviser business model — the rise of charging stand-alone fees for advice services, from hourly to project to subscription or retainer fees. That’s similar to the RIA’s AUM model — which technically had been around for decades (back to the 1940s) but only accelerated in the 1990s after technology made scalable billing feasible. The fee-for-service model has similarly existed in some form for decades, with advisers at Garret Planning Network and the Alliance of Comprehensive Planners charging hourly and annual retainer fees, respectively, since the 1990s, but it’s now being catalyzed by the rise of technology platforms that make scalable billing possible for the first time ever.

Similar to the rise of RIA custodial platforms to enable AUM fees, the rise of technology platforms to facilitate fee-for-service payments have to navigate the unique compliance issues that arise with respect to advisers having access to clients’ accounts in order to bill fees. In particular, when advisers have direct access to client accounts, they can be deemed to have custody, which creates additional compliance and audit oversight obligations to ensure that client money is protected. In the case of RIA custodians, limitations on how and how much the adviser can transfer in fees help to protect client assets. In the case of fee-for-service payment systems, such as RightCapital’s RightPay feature in its financial planning software and the independent AdvicePay, it’s about ensuring the payment platform, and only the payment platform, has the information on and access to the client’s bank account or credit card number in the first place.

Now, as fee-for-service financial planning continues to rise in popularity, SimplyEasier is rolling out its own fee-for-service billing solution for RIAs, adapting what was originally a payment processing platform for insurance agencies into one that can be used by RIAs for their fee billing as well. Similar to others in the category, SimplyEasier will allow advisers to invoice clients for planning fees via credit card or ACH and schedule one-time or recurring payments. It facilitates clients entering their payment information directly into SimplyEasier so the adviser never touches it directly and therefore avoids custody. It also sends automatic reminders to clients whose credit cards may be lapsing to update their payment details.

From the adviser perspective, SimplyEasier’s functionality may be similar to others, though it is arguably better positioned than solutions like RightCapital’s RightPay, which is limited to only advisers using RightCapital, while independent solutions like AdvicePay or SimplyEasier can be used by advisers with any planning software. Its existing relationships with independent insurance agencies leave SimplyEasier well positioned to capture the ongoing rise of financial planning among annuity agents that have been adding their RIA registration in the years since the Department of Labor’s original 2016 fiduciary rule.

From a broader industry perspective, the greater significance of SimplyEasier’s entrance into fee-for-service billing is simply that it signals an ongoing rise in demand, or at least perceived demand, among advisers to have more technology solutions to facilitate fee-for-service billing. If the shift follows a similar path to the rise of the RIA custodial platform and the adoption of platforms like Schwab, Fidelity and (before-it-was-TD’s) Ameritrade, this may continue to be a nascent channel for several more years before it accelerates further in the second half of the decade as the technology moves further into the fee-for-service adviser mainstream.

The concept of direct indexing originated more than 25 years ago, when Parametric developed a specialized offering for ultra-high-net-worth clients that would allow them to replace a standard index fund like the S&P 500 with all 500 of the component stocks of the S&P 500. This improved the tax efficiency of the portfolio by making it possible for those investors to engage in tax-loss harvesting on the individual stocks. After all, if 200 stocks of the S&P 500 are down but the other 300 are up, such that the index in the aggregate is up, there is no opportunity to harvest losses on the S&P 500 itself at the end of the year. However, with direct indexing, it’s possible to harvest the losses on those 200 stocks that were down. For a high-net-worth investor in the top tax brackets, this can amount to a sizable capital loss to generate immediate tax savings.

For much of its history, the caveat to direct indexing was that there was still a trading commission for each stock trade, which across hundreds of stocks in an index could add up quickly. For example, a $19 stock trading commission in 1999 when the investor only needed a single $90 share amounted to a trading cost of over 20%. And because individual stock shares are bought in whole share units, for very small positions in the index, a nontrivial tracking error could occur if the investor tried to divide too few dollars across too many stocks, resulting in misallocations when bought in whole-share units. For example, the smallest weightings in the S&P 500 have an allocation of less than 0.01%, which means an investor allocating $100,000 should only hold $10 in the position, but if the stock trades for $90 a share, even just holding one whole share would result in a nine times overweighting in the position.

However, the rise of fractional share trading and the emergence of “ZeroCom” (zero trading commissions on stocks) have suddenly made it feasible to democratize direct indexing for investors of much more modest means, paying a single AUM fee for the offering while buying the exact allocation via fractional shares and without chewing up per-stock transaction charges.

Accordingly, Charles Schwab announced that it is formally launching its Personalized Indexing solution, which will start with a series of three stock indices (the Schwab 1,000 large-cap index, a small-cap index based on the S&P SmallCap 600, and an ESG index based on the MSCI KLD 400 Social index), with automated tax-loss harvesting of the underlying stocks in the index, for a fee of 40 basis points. This means that of the four types of direct indexing solutions, it focuses primarily on the tax-focused version of direct indexing. However, it has pledged additional customization capabilities for clients to make their direct indexing portfolios even more personalized over the next 12 to 18 months.

What’s notable, though, is that tax-loss harvesting, in the end, doesn’t actually produce much in tax savings. When an investor harvests a loss, for example, by taking an individual stock that was originally purchased for $10,000 and selling it for $7,000, there is an immediate tax deduction of $3,000. At a 15% capital gains rate, this results in $450 of tax savings but the transaction also reduces the cost basis to$7,000. This means when the stock eventually recovers, there will be a new $3,000 gain if/when the stock is sold for $10,000-plus in the future, which at the same 15% capital gains rate, completely offsets the $450 of tax savings. As a result, the real benefit of tax-loss harvesting isn’t the $450 tax savings, but the fact that the investor gets to keep and invest the $450 during the interim, earning the growth on that $450. At a long-term growth rate of 8%, this would amount to $36 a year of actual economic benefit or a value of about $36 / $10,000 = 36 basis points of additional return from tax deferral.

Which is important, because Schwab’s Personalized Indexing has rolled out at a cost of 40 basis points, which would be more than the entire tax-deferral benefit on the stock that dropped by 30% in the first place. The economic value of the tax-deferral benefit would be higher for those in top tax brackets (20% long-term capital gains, plus the 3.8% Medicare surtax, plus potential for 10%-plus state tax rates on top, which would result in almost 80 bps of tax-deferral benefits on the same investment example). However, the reality is that only a subset of stocks is likely to be down in any particular year — such that the investor will only capture tax-loss harvesting benefits on a portion of the portfolio while paying the 40-bps fee on all of it. Once a stock’s loss is harvested and the cost basis is stepped down, there’s even less opportunity for tax-loss harvesting again in the future even as the direct indexing fee continues to toll.

Ultimately, the key point is that while direct indexing and the tax-loss harvesting it generates do have a real economic benefit, that benefit is limited — primarily by tax bracket, and also by the overall volatility of the market or lack thereof that creates loss harvesting opportunities. It also tends to diminish over time as all the holdings in the portfolio have either already been harvested down, or have risen so much they will never fall below their original basis in the future. This raises the question of whether Schwab’s 40-bps fee may be too much to pay for direct indexing in the long run, at least for a tax-focused solution, and whether that pressure will force Schwab, and other direct indexing providers, toward one of the other direct indexing approaches that may be less price-sensitive in the future.

In the meantime, we’ve rolled out a beta version of our new AdviserTech Directory, along with making updates to the latest version of our Financial AdviserTech Solutions Map with several new companies (including highlights of the Category Newcomers in each area to highlight new FinTech innovation).

So what do you think? Are you a Redtail user who wasn’t using Orion but might now? Are you an Orion user who wasn’t using Redtail but would consider it now? Do you like RightCapital’s new One Page Snapshot feature? And what would you pay for the tax-loss harvesting benefits of offering (Schwab’s) Direct Indexing to your clients?

Michael Kitces is the head of planning strategy at Buckingham Strategic Partners, co-founder of the XY Planning Network, AdvicePay and fpPathfinder, and publisher of the continuing education blog for financial planners, Nerd’sEye View. You can follow him on Twitter at @MichaelKitces.

“It’s time for an economic reset,” wrote the California governor, in a post on X.

Masterworks was launched in 2017 but its RIA, Masterworks Advisers, is just three years old.

One 2017 form, no broker license, and a $42 million gap they say surfaced on a webinar.

Fewer than half of Americans in their peak earning years feel on track for retirement, while many say limited financial knowledge and access to professional guidance are holding them back.

Meanwhile, Wells Fargo hauled advisors overseeing $825 million in the West Coast, while Wedbush has welcomed a seasoned professional from Stifel in California.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.