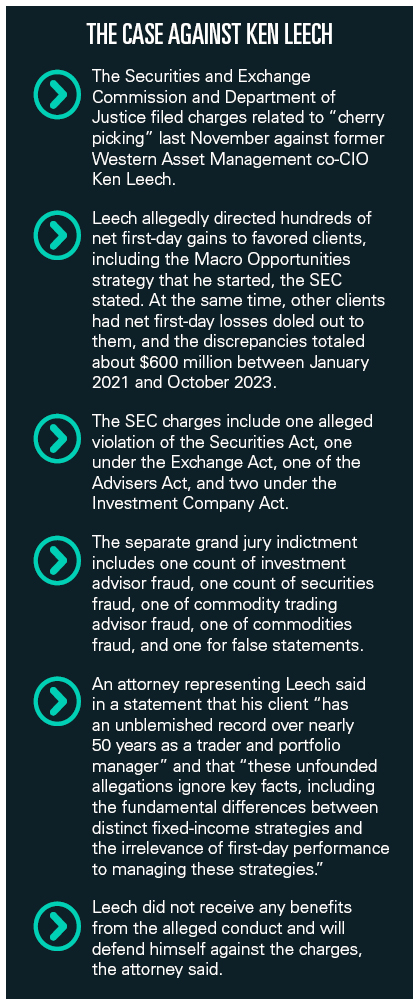

Franklin Resources has been dealing for several months with the fallout of former Western Asset Management Company co-CIO Ken Leech’s role in an alleged cherry-picking scheme.

Since Leech was charged in late November by the SEC and Department of Justice, clients have pulled tens of billions of dollars from Western, which Franklin acquired as part of its purchase of Legg Mason in 2020. For the quarter that ended December 31, 2024, there was a total of nearly $68 billion in long-term net outflows from Western, more than half of which happened in December alone, Franklin said in its recent quarterly report.

Since Leech was charged in late November by the SEC and Department of Justice, clients have pulled tens of billions of dollars from Western, which Franklin acquired as part of its purchase of Legg Mason in 2020. For the quarter that ended December 31, 2024, there was a total of nearly $68 billion in long-term net outflows from Western, more than half of which happened in December alone, Franklin said in its recent quarterly report.

That, however, was only since charges were announced. Since the company disclosed an SEC investigation last August, along with Leech stepping down, about $120 billion has been drained from Western, at least through January, executives said in an earnings call.

Despite being media shy, Leech, who was long renowned for his trading skills, was the star bond manager at Western – the face of its highly regarded aptitude in the fixed-income world.

That, of course, changed abruptly, and the consequences have been enormous. While Franklin has pledged to support Western’s operations while allowing its investment team to remain independent, the parent company has also announced a three percent cut to its workforce.

“In order to continue to invest in our long-term growth initiatives and evolve for the future, we need to find savings and remain focused on our effectiveness and efficiencies,” Franklin spokesperson Jeaneen Terrio said in a statement. “No investment professionals were impacted” by the layoffs, she noted. “While a workforce reduction is not easy, we believe these changes will make us even better positioned to serve clients in the future.”

Until very recently, “star” portfolio managers were a draw for fund companies, adding strength to their reputations and giving easy publicity to those that consistently outperformed.

Peter Lynch, manager of Fidelity’s Magellan Fund, delivered returns during the 80s that far surpassed the S&P 500. Legg Mason’s former CIO, Bill Miller, beat that index for 15 years straight, through 2005, as portfolio manager of the firm’s Capital Management Value Trust.

Pimco cofounder and former portfolio manager Bill Gross was once crowned “the bond king.” His contemporary, DoubleLine Capital founder Jeffrey Gundlach, has been bestowed with a similar title.

While having stars can give firms an upside, there are risks.

The firm at which Gundlach managed money – TCW Group – saw $25 billion in redemptions in only two months after it fired him in late 2009.

At Pimco, lagging performance in the Total Return Fund and Total Return ETF had caused investors to start pulling money before Gross exited the company in 2014 – but outflows were dramatic in the months and years following, with total assets in the mutual fund dropping to a reported $101 billion by August 2015, roughly a third of what they were two years prior.

Asset managers understand that, just as easily as assets can be attracted by stars, they can also be lost to them.

The institutional investing world has favored team management on funds for a long time; they want to be assured that, should one portfolio manager leave, things can be expected to continue as usual, said Craig Kilgallen, director of relationship development at Fuse Research Network.

That line of thought eventually permeated wealth management, and today, it’s less common to see asset managers emphasize single managers.

“You still see named PMs retire or change firms covered in the financial press, but asset managers have worked hard to emphasize with the marketplace that returns are driven by the team approach or the investment process rather than one individual. That said, PR is impactful and having a manager who is sought after and viewed as an expert can be quite valuable,” Kilgallen said in an email. That is “particularly [the case] in the wealth channel, where the increase of passive investing is consistently highlighted. Active managers do deliver alpha, and that story needs to be told. Firms just need to balance that visibility with the overall impact of the team on delivering results to investors.”

Indeed, advisors are not all sold on active management.

Filip Telibasa, owner of Benzina Wealth, calls it “a thing of the past” and that odds of trying to pick the best manager are slimmer than betting on horse racing.

“The star fund managers essentially ended with the downfall of Cathy Woods from ARK. I believe most of the industry (including clients) is embracing efficient market theory and utilizing index funds to diversify portfolios,” Telibasa said in an email. “We realize low fees paired with a focus on goals/values to utilize tax efficient accounts gets you further ahead than trying to pick the best manager from last year (who may or may not repeat next year).”

Another opinion comes from an advisor who is also the portfolio manager of a recently launched active fixed-income ETF.

“Active management is making a comeback. I think one of the things that the last three years have really highlighted is that there is real value that an active manager can bring, especially on the risk-management side,” said Leibel Sternbach, founder of Yields4U.

“For those of us who are taking income from their portfolios, time is a luxury we don’t all have, and so active management can help reduce volatility and reduce the chance of compounding those market losses when we take our income.”

“Over the past few years, you’ve seen less and less of fund companies propping up star managers or solo managers,” said Max Curtin, manager research analyst at Morningstar Research Services.

That is no coincidence, he said, with fund providers recognizing key-person risk, or the likelihood that if a face leaves, money can as well.

“At Western, it wasn’t as cut and dry. Leech spent time and grew the business from nothing and received all sorts of accolades – and deservedly so,” Curtin said. Leech wasn’t the only manager on the funds he oversaw, with the exception of the now-liquidated Macro Opportunities Fund that he started, as Western emphasized a team approach, Curtin noted.

Also complicating that are outflows that started well before the SEC’s investigation was known – those were performance-related, as the funds struggled in 2022 through 2024, he said.

“The outflows have been egregious since this news broke. But these funds – Core and Core Plus – were in very heavy outflows prior to any of this becoming publicly available.”

It’s difficult to show how much fund companies truly rely on teams, rather than individuals, as marketing a team approach gives some confidence to clients that strategies won’t suffer if a person leaves, Curtin said. Fund prospectuses often list large teams, even if only a couple of people do most of the work managing the money.

Because of that, it’s hard to show with any reliable data how the average size of management teams has changed over the years.

“One of the biggest challenges is sifting through marketing spin,” he said.

At Franklin, the team approach helps develop talent, Terrio said.

“Movement within our investment teams creates opportunities for some of our strongest talent, including promoting talent into leadership and portfolio management roles,” she said.

“Western Asset’s team-based approach ensures that the departure of any one professional – or even of several professionals – does not impact the investment management process. Our experienced team will continue to provide the continuity and outstanding investment expertise our clients expect.”

Five low-cost index ETFs to anchor Trump Accounts as advisors weigh options against 529 and UTMA plans for clients

A bipartisan proposal aimed at aligning advisor compensation rules with modern business structures is headed to the full House.

Vanilla is extending its estate planning tech to Callan Family Office's ultra-high-net-worth business, while WealthFeed's organic growth engine will now be available to roughly 100 advisors at The Mather Group.

“We are helping families take an important first step toward building a financial foundation for the next generation,” said Franklin Templeton CEO Jenny Johnson

Richard Brothers Financial Advisors joins the fee-only RIA, adding its first Maine office and $240 million in client assets

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.