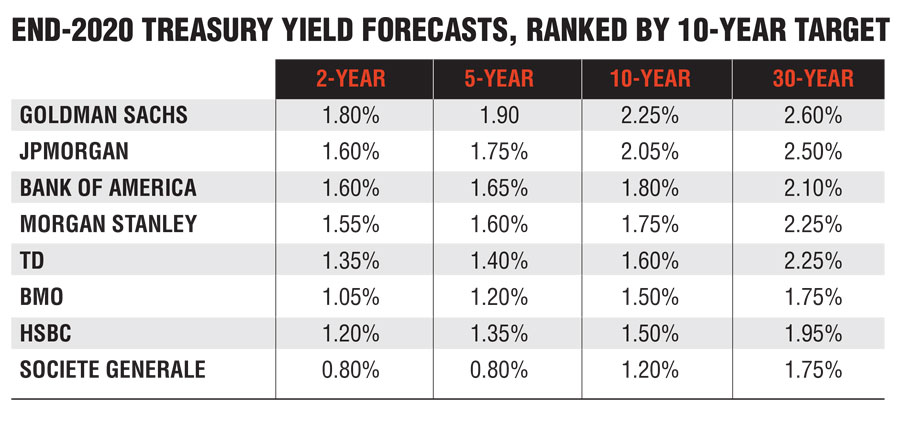

• Societe Generale (Subadra Rajappa, Nov. 29 report)

• U.S.-led economic slowdown and 100 basis points of Fed rate cuts "should keep yields close to bottom, or drive them there, in 2020"

• In U.S. markets, she suggests retaining "a long-duration bias outright and/or conditionally as we head into a possible recession in 2020." Advises investors to "overlay with tactical short-duration hedges to position for possible near-term trade deal euphoria," but reckons any sell-off should be modest

• Sees the U.S. yield curve steepening on Fed rate cuts and the euro-area's remaining directional, steepening in bearish moves and flattening in bullish ones

• Morgan Stanley (Matthew Hornbach, Dec. 1 report)

• U.S. 10-year yield will face upward pressure during first half from higher yields in Europe, especially the U.K., then return to around 1.75% in the second half

• Fed's reaction function means risks "skew asymmetrically to rate cuts over rate hikes"

• The expectation for the Fed target that's embedded in the 10-year yield is near 2.5%, which is in line with the median forecast of policy makers over the longer term, but "if the Fed remains on hold at current levels of policy for the next decade, the rate expectation embedded into the 10y yield will be 75bp too high"

• In a separate report on Dec. 3, Morgan Stanley's Guneet Dhingra said that the combination of presidential-election dynamics, a Fed that's on pause and stability of realized inflation leads the bank to forecast "relatively unchanged" levels in 10-year inflation breakeven rates; sees breakevens ending 2020 at 1.60% and real yields staying in positive territory, finishing next year at 15 basis points

• JPMorgan (Jay Barry and others, Nov. 26 report)

• Yields likely to decline early in 2020 as the Fed responds to lingering weakness by implementing one rate cut in the second quarter, then retrace in the second half "as U.S. and global growth returns above trend"

• The bar for the Fed to tighten policy next year is very high because core PCE inflation is likely to remain below 2%

• Outcome of Democratic presidential primary "could have a pronounced influence on rates markets"

• From a technical standpoint, 10-year yield has first support at 2.12%-2.18%, then 2.35%, with resistance levels at 1.60% and 1.52%, according to Jason Hunter

• Inflation breakevens should be stable into the first quarter "before widening over the balance of the year," according to Phoebe White, who sees 5-year and 10-year rates ending 2020 around 190 basis points and the 30 year at 195 basis points

• Goldman Sachs (Praveen Korapaty, William Marshall, Nov. 25 report)

• G-10 yields are likely to rise in 2020 "on account of the improved economic outlook and the removal of some tail risks" such as the trade war and Brexit uncertainty

[Recommended video: Ed Slott: Why you may not want to convert all your IRAs to Roths]

• With most central banks on hold, including the Fed, "higher bond risk premia should drive much of the yield repricing" that the bank is forecasting

• Yield curves "should trade with a steepening bias," especially markets that lack policy space

• Central bank balance-sheet expansion should bring lower volatility and steeper volatility curves, though in the U.S. the presidential election "could be a source of volatility around our projected path";

• Bank of America (David Woo, Carol Zhang, Nov. 19 report)

• Uncertainty around the trade war, Brexit and the U.S.-Mexico-Canada trade agreement "is likely to be resolved soon," and reflation trades should outperform in 2020; Fed likely sidelined, with U.S. presidential election raising the bar for a hike

• Best contrarian G-10 rates trade is 5-year to 30-year yield curve flattener: enter at 67 basis points, target 35 basis points, stop at 90 basis points

• While conventional wisdom suggests curve bear steepens on positive growth shocks, Bank of America sees it flattening because:

• Market needs to price out additional Fed cut

• Global yield grab will remain dominant theme in long end

• Stretched positioning in U.S. dollar duration "is likely more concentrated at the front end due to the expectation or hedging of Fed cuts"

• TD (Priya Misra, Nov. 22 report)

• The Fed will be forced to ease twice more in the first half of 2020 because of spillover from manufacturing to the consumer and low inflation

• "This should help lower rates and steepen the curve"

• Remains long January 2021 fed funds, 10-year Treasuries and in 5s30s steepeners

• BMO (Ian Lyngen, Jon Hill, Ben Jeffery, Nov. 27 report)

• Anticipates a bearish start to 2020 for Treasuries on economic optimism, although that will likely be short-lived, with data in the first two quarters driving yields lower

• 10-year yields will hold a 100-to-125 basis-point range around 1.50% or 2%

• Fed's next move will be a cut, following "a prolonged period of stable policy rates"

• HSBC (Lawrence Dyer, Shrey Singhal, Dec. 3 report)

• 10-year yields "are unlikely to sustain a move above 2%" in 2020 with the Fed on hold or likely to ease

• A range of 1.25% to 2.25% is predicted, with lower yields likelier than higher ones

• With the Fed likely to react to lower inflation or inflation expectations, TIPS breakevens have downside support in the 1.5% area

• Societe Generale (Subadra Rajappa, Nov. 29 report)

• U.S.-led economic slowdown and 100 basis points of Fed rate cuts "should keep yields close to bottom, or drive them there, in 2020"

• In U.S. markets, she suggests retaining "a long-duration bias outright and/or conditionally as we head into a possible recession in 2020." Advises investors to "overlay with tactical short-duration hedges to position for possible near-term trade deal euphoria," but reckons any sell-off should be modest

• Sees the U.S. yield curve steepening on Fed rate cuts and the euro-area's remaining directional, steepening in bearish moves and flattening in bullish ones

• Morgan Stanley (Matthew Hornbach, Dec. 1 report)

• U.S. 10-year yield will face upward pressure during first half from higher yields in Europe, especially the U.K., then return to around 1.75% in the second half

• Fed's reaction function means risks "skew asymmetrically to rate cuts over rate hikes"

• The expectation for the Fed target that's embedded in the 10-year yield is near 2.5%, which is in line with the median forecast of policy makers over the longer term, but "if the Fed remains on hold at current levels of policy for the next decade, the rate expectation embedded into the 10y yield will be 75bp too high"

• In a separate report on Dec. 3, Morgan Stanley's Guneet Dhingra said that the combination of presidential-election dynamics, a Fed that's on pause and stability of realized inflation leads the bank to forecast "relatively unchanged" levels in 10-year inflation breakeven rates; sees breakevens ending 2020 at 1.60% and real yields staying in positive territory, finishing next year at 15 basis points

• JPMorgan (Jay Barry and others, Nov. 26 report)

• Yields likely to decline early in 2020 as the Fed responds to lingering weakness by implementing one rate cut in the second quarter, then retrace in the second half "as U.S. and global growth returns above trend"

• The bar for the Fed to tighten policy next year is very high because core PCE inflation is likely to remain below 2%

• Outcome of Democratic presidential primary "could have a pronounced influence on rates markets"

• From a technical standpoint, 10-year yield has first support at 2.12%-2.18%, then 2.35%, with resistance levels at 1.60% and 1.52%, according to Jason Hunter

• Inflation breakevens should be stable into the first quarter "before widening over the balance of the year," according to Phoebe White, who sees 5-year and 10-year rates ending 2020 around 190 basis points and the 30 year at 195 basis points

• Goldman Sachs (Praveen Korapaty, William Marshall, Nov. 25 report)

• G-10 yields are likely to rise in 2020 "on account of the improved economic outlook and the removal of some tail risks" such as the trade war and Brexit uncertainty

[Recommended video: Ed Slott: Why you may not want to convert all your IRAs to Roths]

• With most central banks on hold, including the Fed, "higher bond risk premia should drive much of the yield repricing" that the bank is forecasting

• Yield curves "should trade with a steepening bias," especially markets that lack policy space

• Central bank balance-sheet expansion should bring lower volatility and steeper volatility curves, though in the U.S. the presidential election "could be a source of volatility around our projected path";

• Bank of America (David Woo, Carol Zhang, Nov. 19 report)

• Uncertainty around the trade war, Brexit and the U.S.-Mexico-Canada trade agreement "is likely to be resolved soon," and reflation trades should outperform in 2020; Fed likely sidelined, with U.S. presidential election raising the bar for a hike

• Best contrarian G-10 rates trade is 5-year to 30-year yield curve flattener: enter at 67 basis points, target 35 basis points, stop at 90 basis points

• While conventional wisdom suggests curve bear steepens on positive growth shocks, Bank of America sees it flattening because:

• Market needs to price out additional Fed cut

• Global yield grab will remain dominant theme in long end

• Stretched positioning in U.S. dollar duration "is likely more concentrated at the front end due to the expectation or hedging of Fed cuts"

• TD (Priya Misra, Nov. 22 report)

• The Fed will be forced to ease twice more in the first half of 2020 because of spillover from manufacturing to the consumer and low inflation

• "This should help lower rates and steepen the curve"

• Remains long January 2021 fed funds, 10-year Treasuries and in 5s30s steepeners

• BMO (Ian Lyngen, Jon Hill, Ben Jeffery, Nov. 27 report)

• Anticipates a bearish start to 2020 for Treasuries on economic optimism, although that will likely be short-lived, with data in the first two quarters driving yields lower

• 10-year yields will hold a 100-to-125 basis-point range around 1.50% or 2%

• Fed's next move will be a cut, following "a prolonged period of stable policy rates"

• HSBC (Lawrence Dyer, Shrey Singhal, Dec. 3 report)

• 10-year yields "are unlikely to sustain a move above 2%" in 2020 with the Fed on hold or likely to ease

• A range of 1.25% to 2.25% is predicted, with lower yields likelier than higher ones

• With the Fed likely to react to lower inflation or inflation expectations, TIPS breakevens have downside support in the 1.5% area

Regulators found Bank of America's monitoring software had a known flaw Merrill left uncorrected for years.

While AI has become a go-to research tool for affluent investors, new HSBC research suggests human advisors remain the deciding voice when investment decisions are made.

A 5-4 ruling preserves the Federal Reserve's independence for now, but the legal fight over presidential removal power is far from settled.

For years, large firms have been facing penalties and questions from regulators over interest rates for clients’ cash accounts.

Market volatility can be stressful, but it also represents opportunity for advisors and their clients.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.