If you start claiming Social Security benefits before reaching full retirement age (FRA), your earnings may be subject to an annual limit. Exceeding this threshold could reduce your monthly retirement checks.

Not everyone, however, retires at the beginning of the year. If you retire around mid-year, there’s a chance that you’ve already earned more than the yearly income limit. This begs the question: Would exceeding this threshold reduce my first year of Social Security benefits?

To provide you with the answer, we’ll delve deeper into the Social Security first year of retirement rule in this client education guide. We’ll discuss who is affected, how the earnings limit is calculated, and how the rule changes after the first year.

We also talked to a Social Security expert to provide insight into this special rule.

If you’re planning on retiring in the middle of the year and wondering how this could impact your monthly benefits, this guide can help. Keep reading and gain the knowledge to help you make informed decisions on your financial future.

The Social Security first year of retirement rule is designed to address the annual income limit for those who retire midyear. Generally, the Social Security Administration (SSA) considers you retired once you start collecting benefits. This is regardless of whether you continue working or not.

“The first-year retirement rule is part of the Social Security retirement earnings test (RET),” explained Martha Shedden, president and co-founder of the National Association of Registered Social Security Analysts (NARSSA).

“[It] applies to individuals who file for retirement, spousal, or survivor benefits before reaching FRA – for most retirees, age 67 – and those who continue working and earning income over the RET limits (annual or monthly).”

Shedden added that if the rule applies to you, then a certain amount of your Social Security check will be withheld based on RET limits. For 2025, the annual limit is $23,400 or $1,950 each month. A dollar is withheld for every $2 you earn above the limit.

However, the Social Security first-year rule excludes any pre-retirement income earned in the calendar year you start receiving benefits. This means that even if your earnings exceed the annual limit, you can still get the full amount you’re entitled to if you retire mid-year.

You can find out more about how the Social Security earnings test works in this guide.

If you retire before FRA and your retirement date falls in the middle of the year, the earnings limit works slightly differently under the Social Security first year of retirement rule.

Essentially, the income threshold switches from an annual limit to a monthly limit. This means that regardless of how much you earn during the first year of retirement, you can receive the complete checks for any month that you earn less than the monthly limit.

“The first-year retirement rule is used for those who start collecting benefits in the middle of the year,” Shedden said. “In these cases, the monthly earnings test (MET) is used if the individual has one or more non-service months (NSM).

“An NSM is a month in which the worker did not have earnings from employment that are more than the monthly exempt amount. A benefit is paid monthly for each month that the earnings are equal or less than the monthly limit.”

The first year of Social Security rule is designed to protect those who retire midyear. It ensures you can still receive benefits even if you earn more than the annual income limit before retiring.

Here are some of the SSA guidelines to take note of:

If you begin collecting benefits before reaching FRA, only the income you earned after retirement counts against the limit. This means that if you retire on July 31, only your earnings starting August onwards will be considered.

Instead of an annual limit, your earnings will be subject to a monthly limit. This year, the monthly cap is $1,950.

If your earnings in any given month exceeds the monthly limit, you will not receive a Social Security retirement check for that month. This means that even if you earn just $1 over the cap, you will not receive any benefits for the month.

Once the year ends, the earnings cap will transition to an annual limit. It’s important to note that the first year of Social Security does not mean 12 months. Instead, this refers to the calendar year.

If you claim retirement benefits but regret the decision, you may get a chance at a Social Security do-over. Find out how this option works in this guide.

The monthly earnings limit is calculated as 1/12 of the annual income limit for the year. For 2025, the monthly cap is $1,950 or $23,400 divided by 12.

Under the Social Security first-year retirement rule, if your earnings for any given month are below the monthly limit, you will receive your full retirement check for that month. If you earn even $1 above the limit, your benefits will be withheld.

The earnings restriction, however, applies only to the income you earn from a job. The following are exemptions:

This means that even if you have additional income sources, you can receive the full Social Security benefit you’re entitled to. This is as long as your job-related income does not exceed the monthly earnings limit.

Once the calendar year when you started claiming Social Security benefits has ended, there are changes to the first-year rule that come into effect:

The annual earnings limit now applies. The SSA reduces your benefit amount if your income exceeds the threshold. As mentioned, the 2025 income limit is $23,400.

Your Social Security benefit is reduced by $1 for every $2 above the annual earnings limit. Let’s say your income is $400 above the cap. This means $200 will be withheld from your benefits.

If you’re self-employed, only your net profits are considered when calculating your earnings against the yearly limit.

The year you reach full retirement age

The annual income limit nearly triples. For 2025, the yearly earnings cap increases to $62,160.

The SSA reduces your benefit amount by $1 for every $3 exceeding the yearly threshold. So, if your job-related earnings are $600 above the limit, then your benefit is reduced by $200.

Your benefit increases to account for any withheld benefits. This means that if you have 12 months of benefits withheld because your earnings exceeded the limit, your benefits will be adjusted accordingly.

“At FRA, the benefit amounts are adjusted to account for the amounts withheld due to earnings and the beneficiary will receive a larger check from that time forward,” Shedden explained.

"If the first year of collecting Social Security benefits is after reaching the month of FRA, the earnings test rules no longer apply,” Shedden said. “Beneficiaries can work and earn as much as they would like, and it will not affect their benefit amounts. In fact, if those earnings are high enough, they may increase their benefit.”

Check out this guide if you want to learn more about how Social Security benefits work.

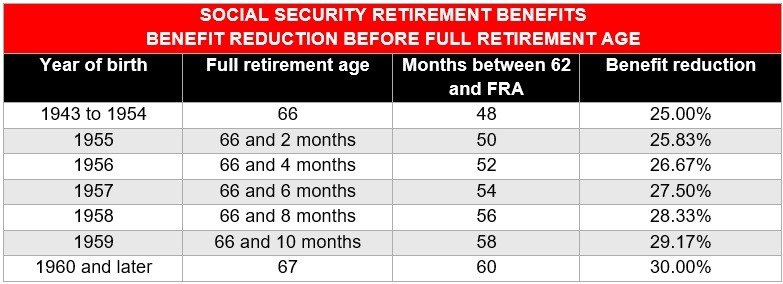

If you have worked at least 10 years and contributed to Social Security, you can collect retirement benefits as early as age 62. The FRA, however, is between ages 65 and 67, depending on the year you were born.

Here’s a summary of the full retirement ages based on the year of birth, according to SSA’s website.

Collecting your Social Security benefits early can be an enticing option. However, you must also consider how it will affect your Social Security benefits.

To calculate how much benefits you’re entitled to, SSA uses a formula based on the income in your 35 highest earning years. This amount is then adjusted for inflation. Early retirement can impact your Social Security payments differently, depending on the situation.

Here are some scenarios:

Your Social Security benefits will be permanently reduced by a certain percentage for every month before your FRA:

The reductions may seem small at first glance, but when they add up, the amount can be significant. Here’s how much early retirement can reduce your retirement benefits, according to SSA.

As mentioned, SSA calculates your retirement benefits on your 35 highest earning years. If you retire before reaching this, the years you did not work count as zeroes in SSA’s calculation. This can reduce your benefit amount by a lot.

Having 35 years of gainful employment, however, does not necessarily mean a higher monthly payout. Some of those years may be low-earning years, which can also affect your Social Security benefit amounts.

You can get an idea of how much retirement benefits you can receive by using SSA’s retirement estimator.

As discussed in the previous sections, you’re subject to the Social Security earnings test when you file for retirement benefits before FRA but continue to work. If your income exceeds a certain threshold, your monthly payouts can be reduced temporarily.

You can learn more about how early retirement affects Social Security benefits in this guide.

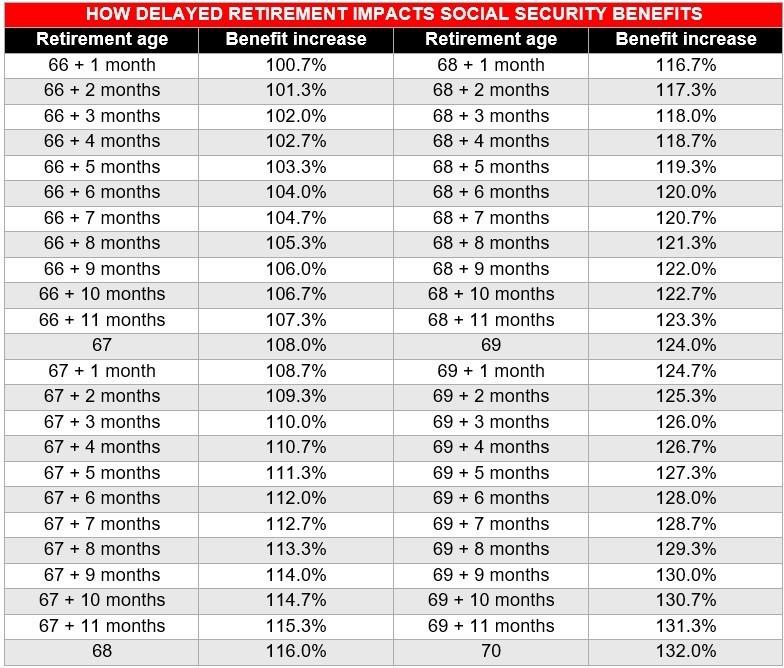

The best and most effective way to maximize your Social Security benefits is to delay retirement if you can. By doing so, you can earn an additional 8% in delayed retirement credits for every year after reaching full retirement age.

Let’s say your full retirement age is 67 and you hold off collecting benefits until age 70. That’s an extra 24% in monthly Social Security payments.

To give you an idea of how much your retirement benefits can increase for every month you delay retirement, we prepared this table based on SSA’s rules.

The Social Security first year of retirement rule allows you to receive the full benefits you’re entitled to if you retire midyear, no matter how much income you earn. By understanding the rules on earnings limits, you can make informed decisions to help maximize your Social Security payouts.

You can also visit our Retirement Planning News Section for more information about Social Security benefits. Be sure to bookmark this page to access breaking news and the latest industry updates.

A $141M judgment and a federal asset freeze collide over one shrinking pool

The firm's CFO and EVP of Wealth Management Solutions are the latest executives to exit the broker-dealer.

Clients are saying they would consider switching advisors if another professional offered estate planning services, according to a new Trust & Will survey.

CEO Laurel Taylor says the fintech's composable AI stack helps workers optimize dollars across Trump Accounts, 529s, 401(k)s, and other employee benefits.

The bank has swiped three private banking veterans from BNY as the city climbs the ranks of America's fastest-growing wealth hubs.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.