This feature is part of InvestmentNews’ April financial literacy series in observance of National Financial Capability Month.

Parents are beginning to realize that this chaotic time is a great opportunity to teach their kids about money. With the S&P 500 recently plummeting by as much as a third, it seems logical to give them a little homeschooling on this topic, too. But be careful. Parents might be tempted to jump right into a lesson about buying individual stocks.

That’s probably not the ideal place to start. Instead of educating your child to become a stock picker, think bigger picture. Most young adults won’t have time to become stock-picking pros. Learning to invest across all the asset classes in a diversified portfolio is a much more practical skill to have. Keep it simple out of the gates.

Step 1: Know your time horizon

This is a conversation of risk and reward. Understanding your time horizon might be the biggest factor in determining how you are going to structure your portfolio. Think about this in terms of a 529 college savings plan. The “age-based option” offers a portfolio that in Year 1 starts off aggressive, gradually becomes more conservative as one nears college. The less time between today and when that first college check needs to be cut, the less time you’ll have for a recoup should the market have a pullback. Make sure to explain the importance of being able to ride out the periodic financial storms.

Step 2: Understand risk versus reward

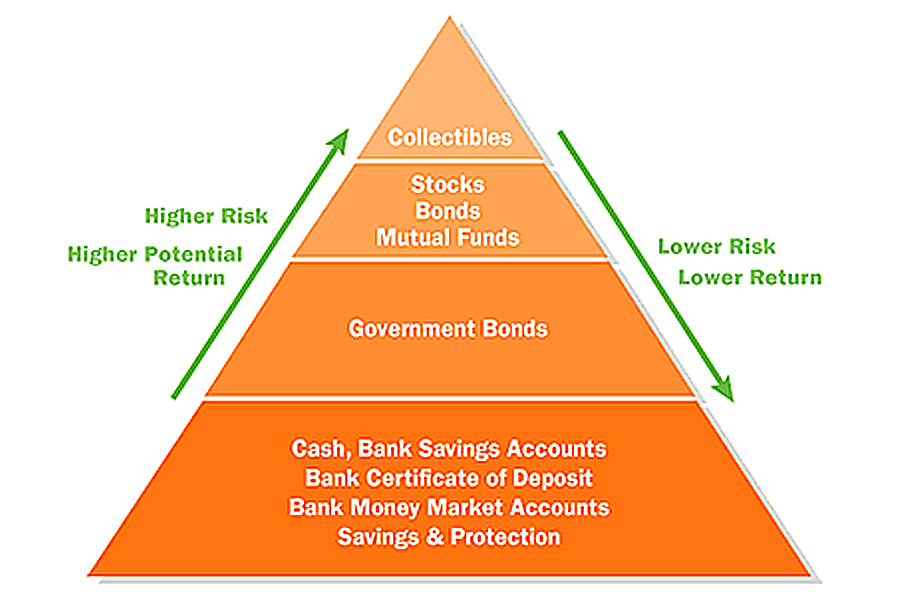

Kids can easily learn the phrase: Low risk, low return; high risk, high return.

Using this pyramid, you can illustrate how different asset classes fit that phrase’s model.

Lower risks assets, such as cash, CDs and money market accounts, are at the bottom of the pyramid (its foundation). Those stable assets typically experience lower returns.

At the top of the pyramid you see higher-risk assets, like stocks. While these asset classes historically provide higher returns (over the long run) they also are more volatile and riskier in the short run. That risk is what facilitates a higher return; however, taking on that risk is necessary to help your money keep up with inflation.

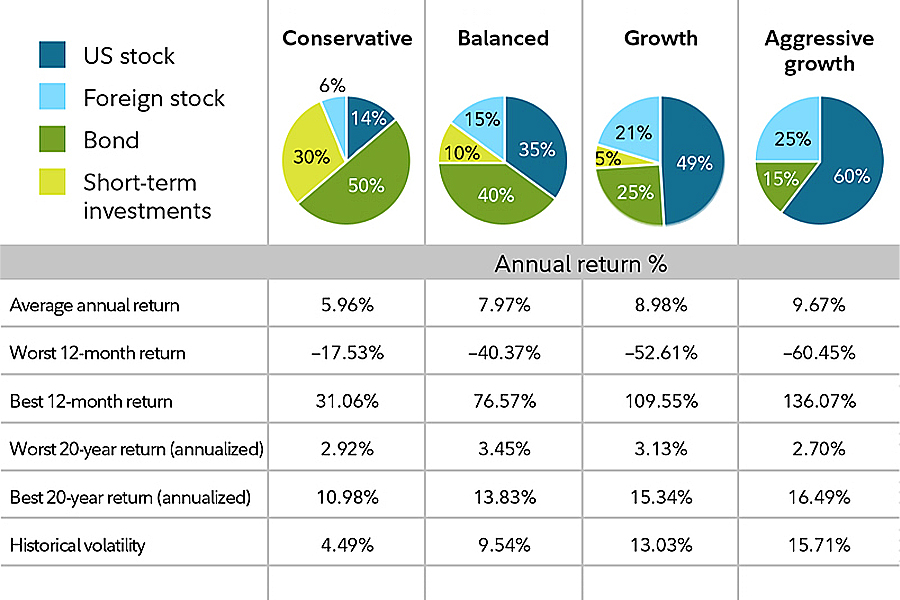

Step 3: Establish your diversification

It has been said that the single biggest determinant of investor returns comes from asset allocation, otherwise known as diversification. Try this chart from Fidelity on for size:

For every comfort level of risk, there is a corresponding asset allocation to diversify assets to align with that risk tolerance. It’s an art, not a science. Choosing a mix of stocks, bonds, alternatives and cash are the major buckets one uses to help construct these portfolios. The longer time horizon you have to ride out the ups and downs of the market’s volatility, the more comfortable you can move to the right on the risk scale, provided this very important point: Only take on a risk level that you won’t get overly emotional with when the market goes down, causing you to act on abandoning the plan. Diversification only works if you stay the course in both up and down markets, keeping those shorter-term dollars in more stable asset classes so the money will be there when you intend to use it.

Step 4: Choose Your Investments

With all the choices in the financial marketplace today, picking which stocks, bonds, mutual funds, ETFs or money managers will be used to execute each part of your well-diversified portfolio is not easy to do. Your preference might be to stick with index funds (as they give broader diversification than just one individual stock) that are low in fees and serve as a starter kit for kids to understand filling “buckets of diversification.”

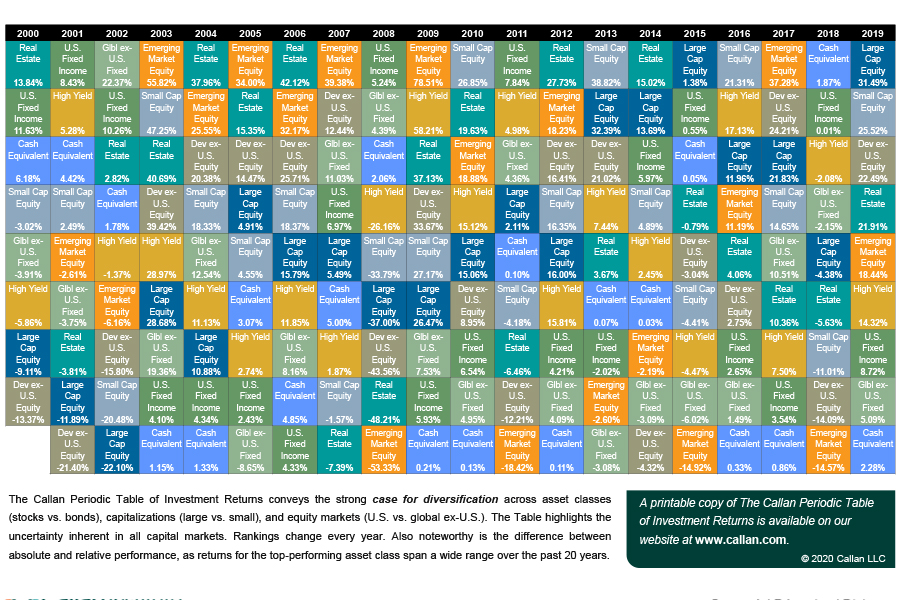

Step 5: Maintain your course

A set asset allocation may need to be tweaked. Monitor it from time to time, rebalancing every so often. This is a good lesson for the youngsters just beginning. By the time they get there, computers might have taken over this entire process and will do the monitoring and rebalancing for them. The Periodic Table of Investment Returns below helps to explain varying returns and the importance of staying the course. It also warns about rebalancing based on what’s happened within the last year in certain asset classes.

You are looking for coachable moments — opportunities that pop up in the flow of ordinary life, enabling you to teach your child in a way that is natural to their environment. Show them an account statement when it arrives in the mail. Ask at the dinner table, “Did you happen to see what happened in the stock market today?” When they show some interest, attempt a deeper dive. If they don’t show an interest, find a way to get it on topic anyway.

While they might not appreciate it today, they certainly will later.

Thomas J. Henske is a partner with Lenox Advisors in New York.

Elsewhere in Utah, Raymond James also welcomed another experienced advisor from D.A. Davidson.

A federal appeals court says UBS can’t force arbitration in a trustee lawsuit over alleged fiduciary breaches involving millions in charitable assets.

NorthRock Partners' second deal of 2025 expands its Bay Area presence with a planning practice for tech professionals, entrepreneurs, and business owners.

Rather than big projects and ambitious revamps, a few small but consequential tweaks could make all the difference while still leaving time for well-deserved days off.

Hadley, whose time at Goldman included working with newly appointed CEO Larry Restieri, will lead the firm's efforts at advisor engagement, growth initiatives, and practice management support.

Orion's Tom Wilson on delivering coordinated, high-touch service in a world where returns alone no longer set you apart.

Barely a decade old, registered index-linked annuities have quickly surged in popularity, thanks to their unique blend of protection and growth potential—an appealing option for investors looking to chart a steadier course through today's choppy market waters, says Myles Lambert, Brighthouse Financial.