This article has been produced in partnership with Advisors Capital

The 401(k) millionaire class is growing: according to Fidelity, the number of its participant accounts with balances over $1 million blossomed to 537,000 in 2024, a year-over-year increase of 27%. The median account balance for this cohort stands at about $1.4 million.

With employees who save in a 401(k) now expecting it to be their main source of retirement income, it’s clear there is a lot at stake. But far too commonly, plan participants end up in default investment options rather than a tailored strategy that will help them achieve their vision for a comfortable retirement, largely because they don’t have the time, investment acumen or help to do better.

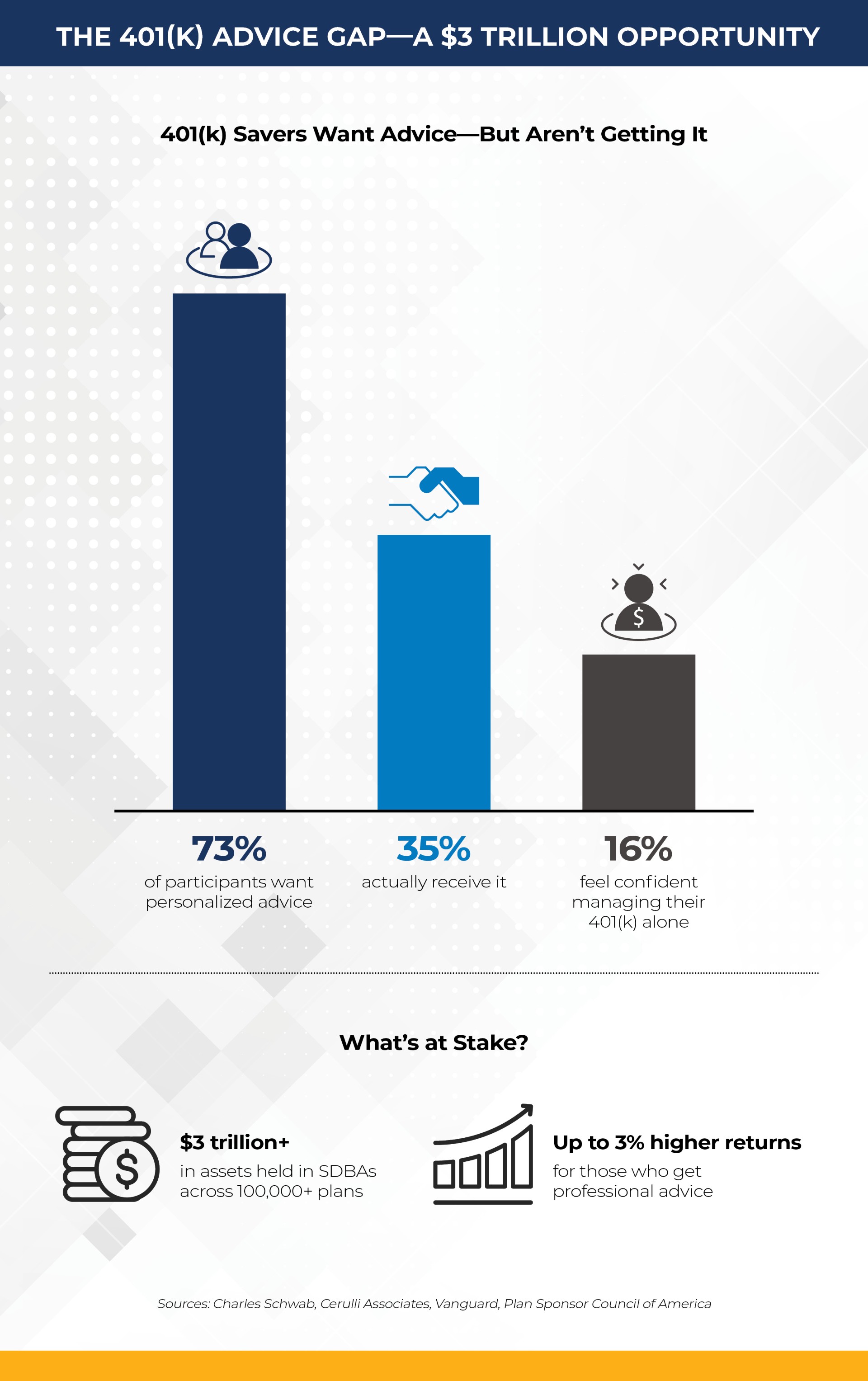

In fact, just 35% of 401(k) participants in a Schwab survey reported receiving advice from a professional financial advisor. It’s not for lack of desire: about three-quarters (73%) of 401(k) savers say they would like personalized investment advice for managing their workplace retirement savings, and just 16% are confident in their ability to manage these investments on their own.

So why aren’t more plan participants getting help, and why aren’t more advisors offering it? Turns out, it’s not that simple. ERISA and the Internal Revenue Code offer strict guidance on how 401(k) advice can be offered to avoid conflicts of interest and to uphold fiduciary responsibility.

“While the need and opportunity are obvious, the reality is a bit more complex,“ says Kenneth Deane, Senior Vice President, Advisors Capital Management (ACM), who oversees ACM’s PathFinder platform. “In an effort to protect participants from biased recommendations, current regulations present a barrier to entry for advisors looking to provide retirement plan advice. Fortunately, there is a compliant, straightforward way in: the self-directed brokerage account.”

A self-directed brokerage account (SDBA) is a type of account offered within a qualified workplace retirement plan that gives participants access to a greater array of investment options than the typical menu. SDBAs are available in nearly 100,000 defined contribution plans, with combined assets approaching $3 trillion.

And it’s not just 401(k) plans within Fortune 500 companies and other corporate entities. Many 403(b) and 457 plans across not-for-profits, healthcare providers, educational institutions and municipalities offer this option. “These plans are in the backyard of virtually every advisor, and most of the major recordkeepers allow SDBAs,” Deane says.

For participants, SDBAs widen the universe of available investment options and open the door to help from a financial professional they know and trust. “To be clear, this isn’t about day trading clients’ retirement savings or getting them into esoteric asset classes,” Deane emphasizes. “SDBAs offer access to a greater array of mutual funds that align with investors’ risk tolerance, plus the guidance of a financial advisor who understands their goals.”

For advisors, SDBAs provide an opportunity to get qualified retirement plan accounts under management without having to be the representative of record on the plan, and to be compensated for the advice they provide. “You can help your client through their working years with one of their biggest investments—help them retire on time, and ideally with more money—and get credit for those assets under management,” Deane says.

Importantly, an SDBA exists in plan, simplifying tax considerations and keeping participants on track toward their savings goals.

Deane also points out that by helping clients with this important asset, advisors can deepen relationships and potentially their stickiness, as clients entrust them to advise on 529 plans, retirement plan rollovers, and more.

Many retirement savers are rightly aware of the impact of fees on their nest egg. Even if they want help, do they want to pay for it?

Consider this powerful statistic: participants who receive professional 401(k) advice see up to 3% higher returns on average, net, than those who don’t.

"Participants leave billions of dollars on the table by relying on default allocations that are not in their best interest,” Louis Harvey, founder of market research firm Dalbar Inc., told RIABiz.

Adds Deane, “Without advice, so many participants default to target-date funds, which only take into account their anticipated year of retirement. Target-date funds are better than nothing, but clients deserve better than better than nothing.”

For advisors looking to add retirement plan guidance to their practice via SDBAs, the process can be straightforward—with the right partner.

There are platforms, such as ACM’s PathFinder, that support advisors in identifying eligible plans, opening SDBAs, and seamlessly integrating a clients’ retirement accounts into holistic, tailored financial plans.

SDBA platforms offered through an RIA and fiduciary like ACM are designed to be secure, compliant with all applicable regulations, and up and running with minimal paperwork. After a quick onboarding process, advisors have a complete view of their clients’ retirement plan assets without any password sharing or data privacy concerns.

Taken together, the benefits of SDBAs for advisors and their clients are manifold: a greater variety of retirement options and outcomes for clients, deeper relationships and additional revenue sources for advisors, and a secure, compliant way to deliver valuable investment guidance to people who need it.

Adds Deane, “As financial fiduciaries ourselves, we want to ensure that clients are positioned to benefit from years of hard work and well prepared for a meaningful retirement—whether they have millions in their account or are just starting out. SDBAs offer a tremendous opportunity for advisors to help them get there, while growing their own practices and assets under management.”

For more information, click here.

Semi-liquid private credit funds are a clear example of both causation and inevitability.

Cerulli research shows advisor retirements and breakaway movement fueling record M&A demand across the wealth management industry.

“The father even shared office space with the son and used a Medallion Guarantee stamp on the client’s account statements,” an attorney said.

The investment banking arm of RBC is ramping up its hiring across the U.S., Canada, and Europe.

The 140-year-old firm catering to ultra-high-net-worth clients joins a growing roster of wealth managers and tech providers plugging Claude into advisor workflows.

As $84 trillion prepares to change hands, advisors who treat estate planning as peripheral are quietly building a sieve, not a book.

In volatile markets, the advisors who win aren't the ones with the best calls - they're the ones whose clients stay the course.