There’s a rich online history of millennials rooting, however insensitively, for a U.S. housing crash to finally give them a leg up at homeownership. Usually on Twitter. Presumably while brunching on avocado toast.

There’s some truth to the reality of their situation. The last time housing prices tanked, the median millennial was early in their career or just transitioning from college into a historically terrible job market, hardly in a position to take advantage. Since then, ever-rising home prices — a perceived engine of wealth in their parents’ generation — have tended to favor buyers with established home equity.

For example, as the median selling price of homes rose nearly 8% in 2022, the National Association of Realtors saw first-time homebuyers’ share of the market fall to a recent low of 26%, and the average age of first-time buyers rise from 33 to an all-time high of 36.

So the news in February that existing home prices had fallen 12% since their peak last June, combined with recent analyst predictions of more of the same through 2024, may have millennials salivating at a chance to climb onto what Americans tend to view as the first step to financial security. For planners working with them, the challenges will be managing expectations and keeping the process in perspective.

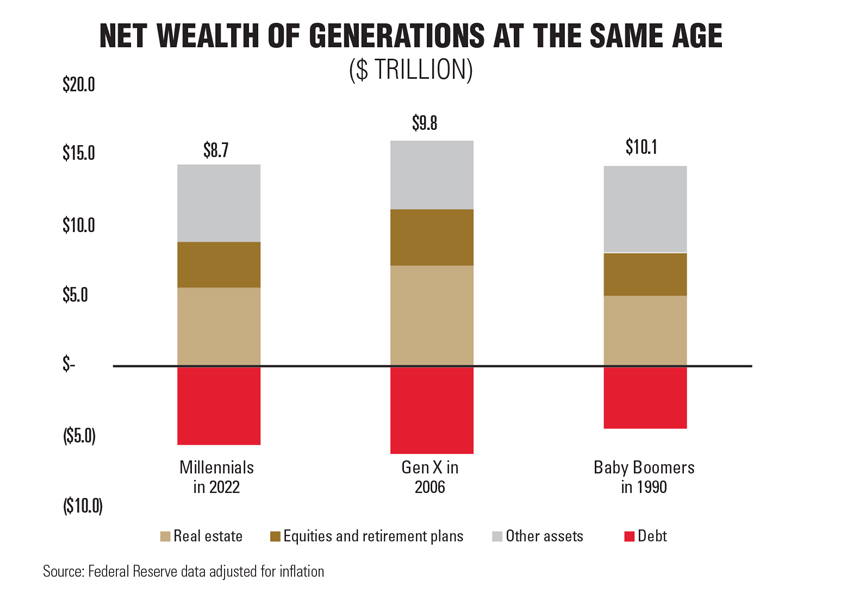

Millennials are, if only by default, in a better position than they were the last time home prices dipped. The generation had accumulated a total of nearly $8.7 trillion in net worth by the end of 2022, according to Federal Reserve data. That lags baby boomers at the same age after adjusting for inflation, largely because of higher debt loads. But the very real problem of high student debt may also be sustaining an economic narrative for the generation that no longer applies.

Jeremy Horpedahl, an economist at the University of Central Arkansas who writes frequently on generational wealth comparisons, notes that broken out per capita, millennials are tracking preceding generations, and that student debt distorts the picture “by overstating liabilities and understating assets.”

“Over their lifetime, that human capital will give them even greater earning potential,” he writes. “Much like Gen X basically tracked boomers until their mid-40s, until their student loans were paid off, and their degrees … really started to pay off in the labor market.”

So, despite a lower homeownership rate than prior generations had achieved at the same age, millennials have largely matched them in building wealth to this point, at least on average. It’s the rest of the trajectory where home equity would seem to play a role — in the years since boomers were the same age as millennials now, median home prices have risen 257%.

But if would-be millennial homebuyers are hoping for a housing crash to get that equity and appreciation kicking, they probably can’t count on their main point of reference. The last housing crash was a unique event, caused by structural problems in the real estate and banking industries that have largely been cleaned up.

“All the buyers that fought over the last couple years — whether they paid top dollar or not — they really had to prove their qualification to get that mortgage, and that’s the difference between now and 15 years ago,” said Dustin Hook, a real estate agent and investor who works primarily in Pittsburgh and Nashville, Tennessee.

“You need to have a longer-term perspective when buying real estate.”

Breanna Stott, Finwell Financial Planning

And per the NAR data, homebuyers are moving as much as three times further than they were just a few years ago. More movement in the remote work era may distort headline figures by changing the geographic composition of sales, resulting in the appearance of a national decline in prices even while some regional markets chug along. And declines from the white-hot market of the past two years will look less significant when zooming out the timeline.

“It’s still really competitive out there,” Hook said. “From what I’m seeing it’s a lot of misconception. Prices really haven’t come down. It’s still about supply and demand, and there are so many buyers out there that have been on the sidelines the last couple years.”

If prices do wind up dropping in the coming years, high mortgage rates will be a main culprit — hardly a boon for affordability.

So, while advisors should temper client expectations about the opportunity behind recent housing market headlines, those crafting financial plans for first-time buyers will also need to help keep the purchase in perspective.

The entrenched American idea of homeownership unlocking wealth, combined with the real opportunity to use leverage to obtain an appreciating asset, can tempt first-time buyers to overextend themselves, especially if they don’t situate the purchase within a financial plan.

“Just because you qualify for a certain purchase price doesn’t mean you should purchase at that price,” said Breanna Stott, a former realtor and current CFP who runs Finwell Financial Planning. “First-time homebuyers might not understand all the different costs that come into homeownership and how that can impact your overall lifestyle. That’s where they came up with the term ‘house poor.’ You typically don’t know what it feels like to own a home until you’ve owned a home.”

The financial benefits of homeownership are real. Building equity in a home is better than paying rent, and property ownership provides benefits ranging from tax advantages to long-term clarity if undertaken correctly. The key, Stott said, is working from a homebuyer’s current budget and making sure they’re committed enough to ride out market fluctuations.

“I think there’s a lot of emotion in buying your first home. It’s where you’re going to live. It’s one of the largest purchases you’ll make in your whole life. And therefore, there’s a lot of analyzing — but not around the right things,” Stott said. “You need to have a longer-term perspective when buying real estate.”

Asset-Map makes a bet on a partner ecosystem while VastAdvisor goes deeper on AI and CRM integration to help advisors grow.

The fintech firm's Iris agent arrives as other financial planning tech providers move quickly to incorporate AI into their workflows.

Also, a Fidelity veteran goes indie with Osaic OSJ Innovative Financial Group, and Citizens welcomes a sports and entertainment-focused trio previously overseeing $800 million from Morgan Stanley.

Former Osaic executive Shah has joined the self-described AI workforce company as managing director in charge of its engagement efforts with wealth firms.

The SEC enforcement division is reportedly digging into potential conflicts of interest, valuations, and disclosure in fast-growing fund manager-led transactions.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.