Matt Wion did not set out to specialize in the annuities business, let alone end up leading the retail unit of one of the biggest providers in the country.

“Circumstance really brought me to annuities,” said Wion, who in March became the head of New York Life’s retail annuities business, succeeding Todd Taylor, who was appointed the company’s head of life insurance solutions. “Coming out of college, I was an actuary … I worked for Prudential right out of school.”

He started in the industry three decades ago after graduating with a Bachelor of Science in mathematics from Pennsylvania State University, including a 10-year stint at Ernst & Young after leaving Prudential in 1999. He landed at New York Life in 2009 and has since been racking up responsibilities at the company across product and finance roles. Prior to his promotion this year, he was chief financial officer in the retail and institutional life and annuities businesses.

He cut his teeth in the business at Ernst & Young. At the time, variable annuities, especially products coupled with riders offering generous guaranteed benefits, were taking off.

“I was using my financial and actuarial background to help companies determine how you price product, how you manage the risk,” he said. “There was a lot of evolution of VA products, a lot of development.”

New York Life was fortunate compared to competitors who offered richer guarantees on products leading up to the 2008 financial crisis, he said. In the years following, it was common to see costs rise on products, benefits decrease, and investment restrictions implemented in conjunction with certain benefits riders. Some carriers offered contract buyback or exchange offers to help get the older VAs off their books.

“Part of the lesson was that these guarantees do carry risk and have to be priced for it,” Wion said. “The risk is not only with respect to the equity market; the risk is also with respect to the bond market.”

In joining New York life, he wanted to apply his consulting experience with insurance companies to help build something. That work was intellectually stimulating, he said.

“I wanted to help a company develop a strategy around these types of products.”

“I wanted to help a company develop a strategy around these types of products.”

Demand for annuities is expected to rise as a wave of baby boomers has been heading into retirement, and the need for guaranteed income has become apparent, he said.

That is coupled with greater needs for generational wealth transfer, which concerns financial advisors, Wion said. Although the profession has generally warmed to annuities, particularly with fee-based products now much more common, there may be a bias against annuities on the part of younger advisors.

“The reality is that newer advisors may not be as open to annuity solutions as they should be,” he said. “The percentage of advisors who are selling annuities is still really light, and part of it is that the annuity process and ability to buy an annuity really need to evolve.”

Despite efforts to ease that process, applications can take a long time, and moving money between accounts isn’t always straightforward, according to Wion.

“You get into situations where even if the advisor is pro-annuity and has a client who is interested, and you get to the application process – it’s cumbersome, and it takes a long time,” he said. “If that is not seamless and transparent, then you’re going to lose potential clients.”

And in no small part, that is because of the “Amazon and Uber effect,” which has led people to expect transactions to be quick and easy, he said. It also means that the insurance business needs to up its game in terms of ease of claim filing, something that Wion believes could help it improve perception among advisors and consumers.

“We’re still as an industry dealing with some of this in real time today.”

“Over the years, we’ve seen much more of an evolution of and innovation in categories like registered index-linked annuities, where there is still the ability to participate in the market, but more of the downside risk is shared with the consumer.”

Those products, called RILAs for short, have quickly become the fastest-selling subcategory of VA in the business.

Those products, called RILAs for short, have quickly become the fastest-selling subcategory of VA in the business.

But consumer preferences for different products change, as do the appetites providers have to offer bells and whistles on variable annuities. A benefit to New York Life’s business model is diversification, Wion said.

That applies to both the range of products it sells as well as the variety of channels through which it sells them, including its captive agency, as well as broker-dealers and banks, he noted.

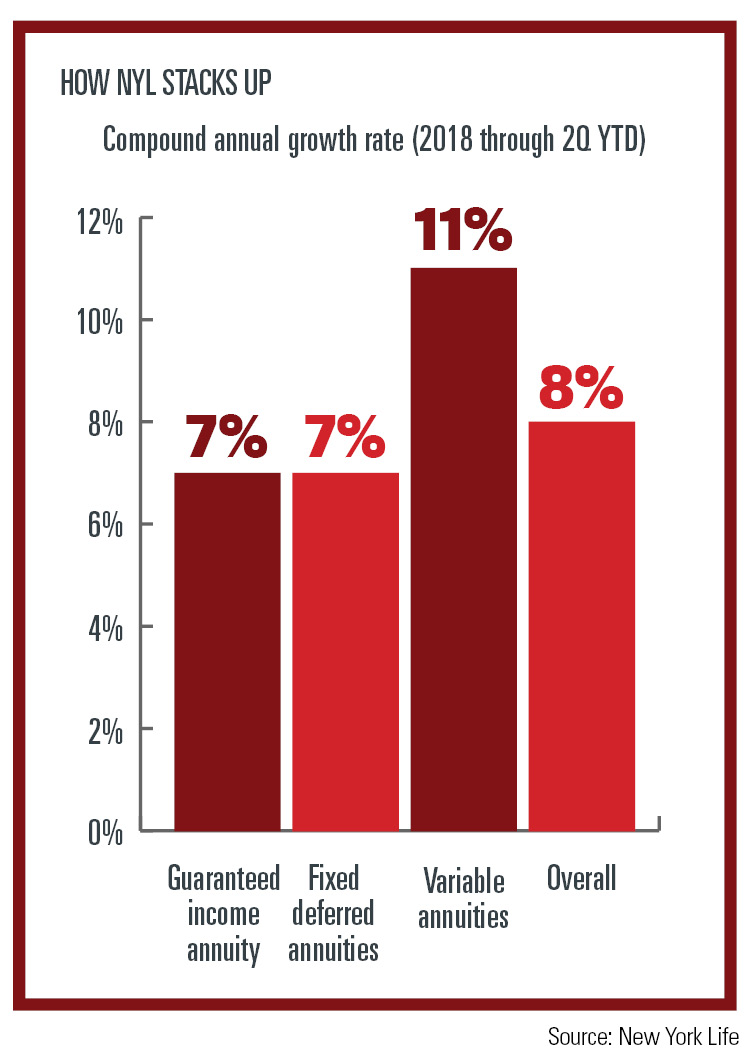

The company is one of just three to be among the top 10 sellers in both the fixed and variable annuity categories, data from LIMRA show. The other two are Allianz and Nationwide.

“We’ve been the number-one provider of income annuities for years,” Wion said, citing a 30 percent market share of the single premium immediate annuity and deferred income annuity segment.

Diversification has helped the company weather different economic environments, he said.

“We’re in this for the long term, which I think is comforting to clients.”

Luke Lee launched the company in 2016. It eventually issued $1.2 billion high-risk investments.

The company aims to bring Quicken's budgeting and investment tool tracking to its 20,000-plus advisor network

Americans may feel better about retirement, but new research suggests confidence and preparedness aren’t always the same thing.

A $2.97 million commission haul and rolled-over retirement money sit at the center.

He sold "safe" notes on his radio show. The SEC says he was never licensed.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.