Although most Americans aren’t directly invested in individual stocks, more than half have some level of investment in the market — mostly in retirement accounts such as 401(k)s. After the coronavirus outbreak took hold in the United States, its economic implications may have left some clients rethinking how much risk they’re willing to take with their hard-earned savings even with the market recovering to pre-pandemic levels.

Thinking about risk differently

With that shocking market volatility still fresh in people’s minds, financial professionals have a valuable opportunity to learn about clients’ real risk tolerance. It’s one thing for clients to answer hypotheticals about saving and losing money, but watching their retirement account balances that have accumulated for years tumble in volatile market conditions sheds light on the real-world implications.

Asking clients how they felt about those stormy market conditions starts the conversation about how much risk they’re comfortable taking moving forward. From some — especially clients in or nearing retirement — you may hear a desire to dial back on portfolio risk. Two recalibration strategies worth considering include increasing fixed-income allocations or annuitizing a portion of the portfolio. Reducing exposure to volatile markets and capturing income guarantees may help clients feel more confident about staying on track for the long-term.

Finding comfort across the spectrum

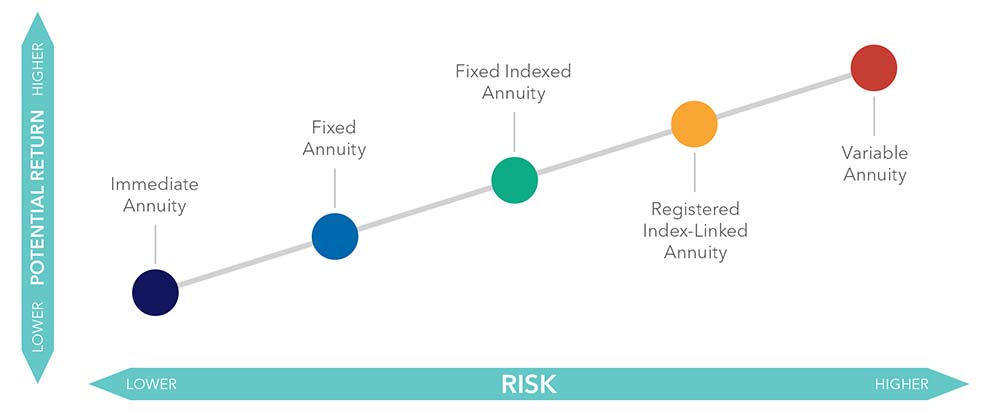

Annuities, which convert money into future income, could be a solution to help clients stay in their financial comfort zone. The chart below maps different kinds of annuities along a risk spectrum. The left side of the spectrum is the most conservative. Clients with the highest tolerance for risk may feel comfortable at the far right.

Diving deeper into annuity options

Depending upon your client’s risk tolerance, this may be the time to reassess your clients’ retirement plan and reallocate a portion of their savings in annuities to better protect their nest egg against future downturns. Given the uncertainty, the future is bright at Athene — a company built to weather market volatility with solid financial solutions geared to help people protect the retirement savings they’ve worked so hard for.

For financial professional use only. Not to be used with the offer or sale of annuities.

Guarantees provided by annuities are subject to the financial strength of the issuing insurance company. Guaranteed lifetime income is available through annuitization or the purchase of an optional income rider for a charge.

Fixed indexed and registered index-linked annuities are not stock market investments and do not directly participate in any stock or equity investments. Market indices may not include dividends paid on the underlying stocks, and therefore may not reflect the total return of the underlying stocks; neither an index nor any market-indexed annuity is comparable to a direct investment in the equity markets.

Athene Annuity and Life Company (61689), headquartered in West Des Moines, Iowa, and issuing annuities in 49 states (excluding NY) and D.C., and Athene Annuity & Life Assurance Company of New York (68039), headquartered in Pearl River, New York, and issuing annuities in New York, are not undertaking to provide investment advice for any individual or in any individual situation, and therefore nothing in this should be read as investment advice.

ATHENE ANNUITIES ARE PRODUCTS OF THE INSURANCE INDUSTRY AND NOT GUARANTEED BY ANY BANK NOR INSURED BY FDIC OR NCUA/NCUSIF. MAY LOSE VALUE. NO BANK/CREDIT UNION GUARANTEE. NOT A DEPOSIT. NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY. MAY ONLY BE OFFERED BY A LICENSED INSURANCE AGENT.

Merrill's latest hires span Colorado to Louisiana, even as industry-wide recruiting data suggests the firm is losing almost as many advisors as it gains.

The $36 million buy allegedly hid inflated books and a $50 million diversion.

“An award citing emotional distress is very unusual,” an industry executive said.

New EBRI research found workers who participated in employer financial education reported higher confidence, literacy and financial satisfaction.

Beyond operational excellence, the winning advisors of the future are the ones who can reach across multiple disciplines without discarding specialist skills.

Northern Trust’s Ken Lassner shows advisors how to convert volatility into after-tax portfolio gains

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income