Everybody on Wall Street is constantly talking about uncertainty and its impact on returns and retirement. Tariffs, taxes, Trump’s tweets - the whole kit and caboodle. No matter where the conversation starts, it always comes back to uncertainty.

So let’s flip the financial script and totally switch things up – shall we?

For a change of pace, let’s chat about certainty – as in annuitized, consistently recurring income streams – because that’s what a whole lot of financial advisory clients want to talk about right now, anyway.

In the first quarter of 2025, US annuity sales reached $105.4 billion, which was 1 percent below the record sales of the prior year’s first quarter, according to LIMRA.For example, Jackson Financial reported retail annuity sales of $4 billion in the highly volatile first quarter of 2025, up 9 percent from the first quarter of 2024.

The S&P 500 index, for the record, experienced a negative return of 4.6 percent in the first quarter of 2025. The CBOE volatility VIX, or the market’s so-called fear index, meanwhile, nearly doubled from 15 to just below 30 over the first three months of the year before screaming past 50 post “Liberation Day” in early April.

And then sinking like a stone below 20 barely a month later.

Yes, when the bull market turns increasingly tenuous and nerves get rattled, more investors seek out the certainty of annuities. Or are at least open to the discussion of adding them to their portfolios to gain a sense of, yep, certainty.

According to a recent nationwide survey, for example, 91 percent of financial professionals agree annuities help their clients protect against market volatility, and 86 percent say annuities help them diversify portfolios.

“Annuities that provide a lifetime income guarantee can reduce the pressure to withdraw spending from an investment portfolio during a market decline. This helps reduce sequence of return risk while also providing lifetime income security,” Michael Finke, professor and Frank M. Engle chair of economic security at The American College of Financial Services, says.

Or, as Mallon FitzPatrick, head of wealth planning at Robertson Stephens, puts it more plainly: “When the market feels like a roller coaster, annuities might be the financial security blanket clients need.”

When a client seeks stability, as opposed to flexibility, FitzPatrick generally recommends low-cost fixed annuities with guaranteed withdrawal riders, as clients desire a reliable stream of guaranteed income. In his view, they are a good solution for clients fretful about inflation’s grip or performance sequence risk, or what he calls “the financial horror story of seeing your nest egg shrink early in retirement.”

“These annuities can be the sleepless-night antidote, focusing on steady income for peace of mind,” Fitzpatrick says.

Elsewhere, Scott Bowers, CEO of FIDx Markets, believes that if a client is concerned about equity risk within their portfolio, a registered index-linked annuity (RILA) is the best solution. A RILA, for the uninitiated, is a type of annuity that combines the potential for growth based on market index performance with a level of protection against losses.

If the concern is about rising interest rates, a fixed index annuity (FIA), where the interest rate is linked to the performance of a market index like the S&P 500, can help lower the risk in their fixed-income portfolio, according to Bowers.

“For clients approaching retirement who are concerned about longevity and sequence of return risk, the risk of receiving lower or negative returns early in retirement, variable annuities (VA) with a guaranteed income stream can help ensure they do not outlive their savings,” Bowers says.

To be sure, annuities are not the only financial instrument that provides certainty in a highly uncertain market and economic environment.

Timothy Smith, founder & CEO, Aurora Private Wealth, for example, often uses buffered structured notes, a fixed-income instrument with downside protection, tied to market index performance as a portfolio-calming alternative. Such vehicles avoid the elevated costs, limitations, and “lockup” of annuities, in Smith’s opinion.

“It doesn’t meet the guaranteed lifetime income need, and so it is generally for larger, conservative portfolios,” Smith says.

Terrell Dinkins, president and founder of OBN Wealth Advisors, says clients can simply sprinkle some US Treasuries into their portfolios to create a sense of ease and more flexibility than annuities. And because you can still find decent rates on market CDs, he believes those are still an option, as well as high-yield savings accounts and dividend stocks for income-seekers.

“All of these options provide more liquidity and flexibility than an annuity,” Dinkins says.

Still, Finke notes traditional investments simply cannot offer the same protection against longevity risk as an income annuity.

“For a risk-averse retiree, an annuity should allow you to spend about 30 percent more each year without the fear of running out in old age. In reality, people feel more comfortable spending from income than they do from investments,” Finke says.

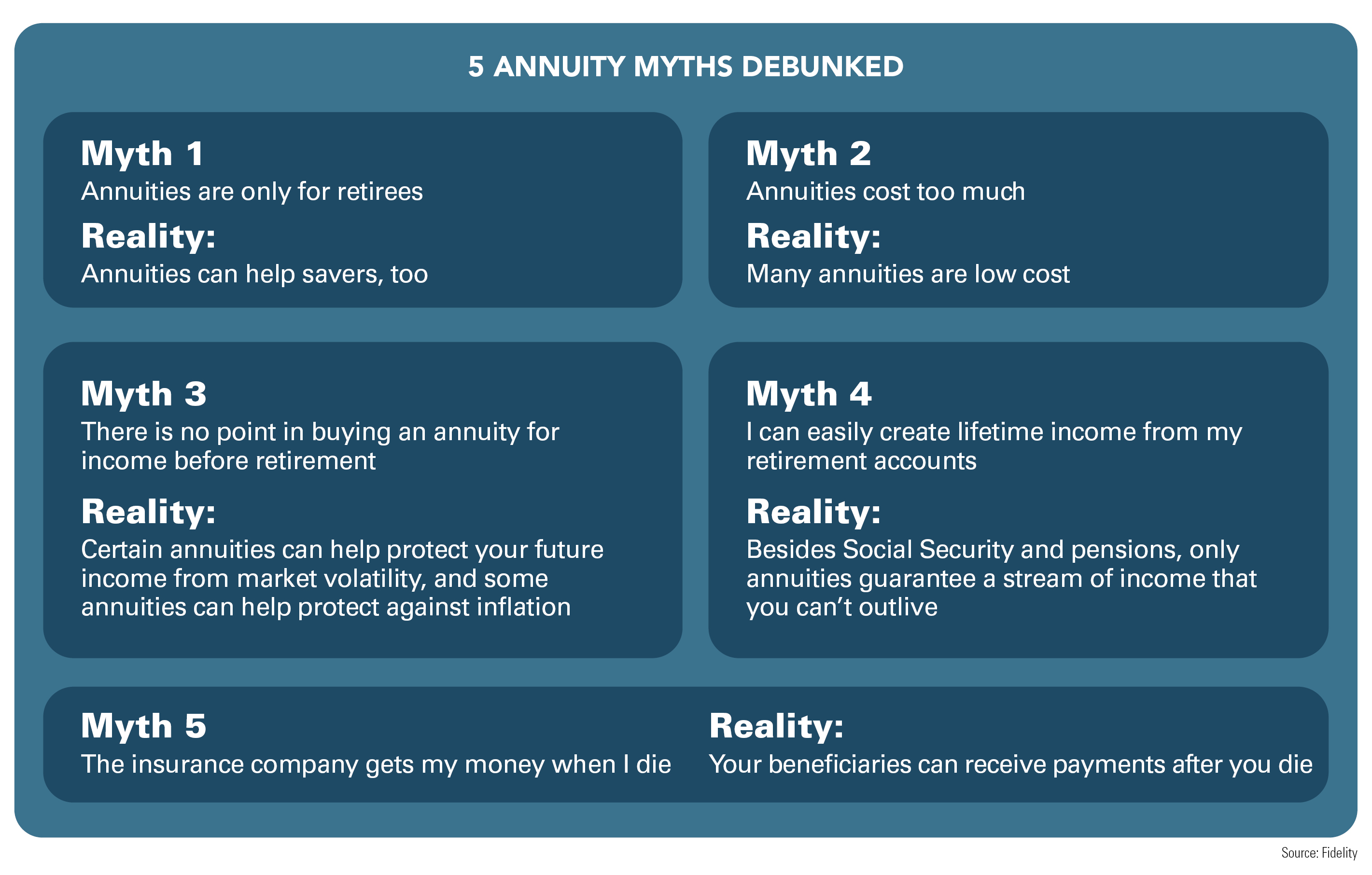

One thing for certain is that annuities have traditionally been seen by retail investors as a more expensive alternative to plain-old, and dirt-cheap, stocks and bonds. That view is not always wrong, despite the drop in annuity fees in recent years.

That’s also the reason why many financial advisors have avoided the annuity conversation altogether. There is no reason to discuss fees, compared to low-cost ETFs, if you don’t have to. Or so the thinking goes.

That’s why Finke believes it’s best to move away from an investment frame to a lifestyle frame to illustrate the benefits of annuities.

“If you have a goal of spending $3,000 a month on top of Social Security to cover basic expenses, you can use a smaller percentage of your overall portfolio to cover this income goal through an annuity than through bonds. This allows the retiree to either spend more on flexible expenses or pass on a greater legacy with their remaining assets,” says Finke.

Bowers, on the other hand, introduces annuities to clients and advisors who haven't used them before through the Insurance Overlays marketplace.

“The solutions you’ll eventually find in it will enable the seamless integration of an insurance 'wrapper' – providing longevity and income solutions – directly within existing managed accounts. The goal is to help expand the number of advisors and clients who have secured retirement income streams,” Bowers says.

Dinkins said he tells his clients that everyone should create a guaranteed bucket of income in their portfolio, especially for those in retirement who truly crave financial certainty.

“The only income certainties are pensions, social security, at least for now, cash value life insurance, and annuities. It’s essential when you reach retirement to feel confident knowing that your basic necessities can be covered if the unexpected happens,” Dinkins says.

Catch-up contributions, required minimum distributions, and 529 plans are just some of the areas the Biden-ratified legislation touches.

Following a similar move by Robinhood, the online investing platform said it will also offer 24/5 trading initially with a menu of 100 US-listed stocks and ETFs.

The private equity giant will support the advisor tech marketing firm in boosting its AI capabilities and scaling its enterprise relationships.

The privately backed RIA's newest partner firm brings $850 million in assets while giving it a new foothold in the Salt Lake City region.

The latest preliminary data show $117 billion in second-quarter sales, but hints of a slowdown are emerging.

Orion's Tom Wilson on delivering coordinated, high-touch service in a world where returns alone no longer set you apart.

Barely a decade old, registered index-linked annuities have quickly surged in popularity, thanks to their unique blend of protection and growth potential—an appealing option for investors looking to chart a steadier course through today's choppy market waters, says Myles Lambert, Brighthouse Financial.