Target-date funds were not immune from the market correction last week. Some saw negative returns of as much as 10%, according to data from Morningstar Direct.

Still, they performed better than they did in 2008. Target-date funds, which are now ubiquitous in 401(k) plans, were heavily tested during the financial crisis, when they were widely criticized for losses sustained by investors near or in retirement. Since then, managers have taken various steps to manage risk, in some cases cutting back on the ratio of stock allocations to fixed income, and in others, increasing it.

Some fund providers have also added a wider range of asset classes to the underlying mix of investments. Others have implemented wider ranges for the allocations along their products’ glide paths, allowing them to rebalance quickly in response to market changes.

If the recent correction is any indication, many of the funds for people close to retirement might be less risky than such products were in 2008.

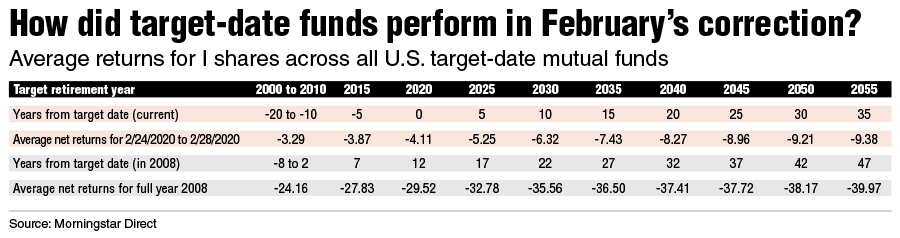

On average, target-date funds with a 2020 vintage had negative returns of 4.1% between Feb. 24 and Feb. 28, according to data from Morningstar Direct. Meanwhile, funds with target years of 2030 had negative returns of 6.3%, and those dated to 2050 returned -9.2%. During that time the Dow Jones Industrial Average dropped by 12%.

By comparison, a simple average of returns for all target-date funds dated 2000 to 2010 saw returns of -24.2% during the full year of 2008, and funds in the 2040 vintage saw negative returns of -37.4%.

To sum that up, last week funds designed for retirees had negative returns about 45% the size of funds with a 30-year target date. In 2008, a comparable rate was about 65%, according to an analysis of the Morningstar data.

However, “the industry has seen a lot of providers increase their equities [allocations] since the financial crisis — the average equity today is probably a bit higher,” said Rich Lang, target-date investment director at Capital Group.

That company’s American Funds Target Date Retirement Funds line made several changes following the crisis, including reducing allocations to high-yield bonds and equities in funds built for retirees, Mr. Lang said. In 2008, Capitol Group’s line of funds had equity exposure that was about 20% higher than its peers. The company gave the markets a chance to recover before dramatically changing that, but in 2009 it reduced the overall equities allocation by about 10%, Mr. Lang said. It has also shifted the mix of stock funds the series invests in, moving toward more dividend-paying funds that have shown less volatility, he said.

“Since then, our series has held up quite well,” Mr. Lang said.

The company still has an equities allocation of about 45% for investors at retirement, which is at least 3 percentage points higher than average, he said. “We feel that at age 65, you’re still a long-term investor.”

That firm’s funds with 2000 to 2010 vintages returned -3.7% last week, on average, while its 2055 vintage returned -8.8%, according to Morningstar Direct data.

Moving targets

Wells Fargo revamped its legacy target-date series in 2017, bringing the management in-house and increasing stock exposure in the glide path. The change came along with a repackaging of its actively managed product, the Wells Fargo Dynamic Target Date series, which is designed to allow hedging in bear markets.

“This type of market is perfect for those [tactical] strategies,” said Christian Chan, a Wells Fargo senior portfolio manager that oversees both lines of target-date funds.

Since last week, the Dynamic series has reduced its equities allocation by 13%, which is a fraction of what it would do in a bear market, Mr. Chan said.

“When we revamped our strategy, one of the things we were really cognizant of was the amount of risk in our target-date funds,” he said. “We were pretty cautious about what equities markets might do over the next five to 10 years.”

Wells Fargo did increase equities in its target-dates, but it took steps to reduce risk in the glide path overall, he said.

Across the company’s two lines of target-date funds, the average return last week for the 2000 to 2010 vintages was -2.8%, while it was -9.4% for the 2055 vintages, according to Morningstar data.

In the long-running bull market, 401(k) plan sponsors have started to pay more attention to performance and less to risk mitigation, which can reward fund providers whose products have heavy stock allocations, Mr. Chan said.

“Sponsors have really gravitated toward higher-risk glide paths,” he said. “The last couple weeks in the market might change that conversation a little bit.”

In early 2018, the company lost about $600 million when a major client, the Employees Retirement System of Texas, pulled investments from its index-based series. The retirement plan sponsor was surprised by the change in investment strategy, Reuters reported. Under Wells Fargo's older strategy, which had higher allocations to fixed income, the series performed well in down markets, ranking among the top performing target-date products during the financial crisis. But as the following bull market went on, the series had struggled to perform as well as its more equities-heavy peers.

Making changes

One of the biggest fund providers, Fidelity Investments, has made three changes to its target-date glide paths since 2008, portfolio manager Andrew Dierdorf said. In 2013 the company bumped up equity exposure, which had the biggest impact on investors in their 40s, he said. The increase was relatively small, about 4% to 7% for people at or near retirement, he said.

At the time, the company found that 401(k) participants were generally saving too little, though most target-date investors stayed invested in the products through rough markets.

Conversely, the company reduced stock allocations by about 5% in 2018, and it added long-duration bonds and Treasury Inflation-Protected Securities. And last year it adjusted the mix of equities from about 70% U.S. stocks to 30% international stocks to a 60% to 40% split, Mr. Dierdorf said.

Because the past decade has allowed for strong performance across asset classes, diversification has not shown the value it can have in shaky markets, he noted.

“Diversification is the best way to manage uncertainty in the capital markets and the uncertainty participants face,” he said.

On average, Fidelity’s 2000 to 2010 vintages returned -2.4% last week, while the 2055 vintages returned -9%, Morningstar data show.

Another major target-date provider, T. Rowe Price, recently announced a planned increase in the equities allocations in one of its lines of funds. Over two years, it will bump up stock exposure for the youngest investors to 98%, up from the current level of 90%, among other changes.

The company has two different lines of target-date funds with separate glide paths and different levels of risk exposure.

Since 2002, T. Rowe has added numerous underlying investments to its target-date, including a range of fixed-income investments in 2017. In 2011, it increased the allocation to international equity from 20% to 30%, according to a company spokesman.

The average returns for T. Rowe’s lines of target-dates in the 2000 to 2010 vintages was -3.7% last week, compared with -8.8% for the 2055 vintages, according to Morningstar data.

The largest target-date manager, Vanguard, has made four changes to its products since 2003, according to data provided by a company spokeswoman. That included only one change to the main structure of the glide path — an overall increase in stock exposure of 10% in 2006.

“Notably, changes are not made based on market performance,” the company said in a statement. “Rather, changes are typically the result of Vanguard’s efforts to reduce an investor’s home bias across asset classes, improve product efficiency and lower the cost of investing.”

Vanguard’s oldest vintages, for 2015, returned an average of -3.2% last week, while its 2055 fund returned -9.1%, Morningstar data show.

The mega-RIA with roughly $160 billion in client assets remains firmly in acquisition mode amid rumors of private equity giants vying to scoop it up.

Record annuity demand for principal protection collides with the most hawkish Fed dissent since 2016.

The PE-backed RIA makes its first major move since bringing in a new capital partner, adding a Massachusetts advisory firm alongside a second East Coast RIA

Stearns Financial Group's addition brings 30 advisors and three decades of North Carolina planning experience to the platform.

An 86-year-old from Dallas tried to withdraw funds from his account, but Edward Jones invoked a FINRA-backed temporary lockout before he eventually left for Merrill Lynch.

Northern Trust’s Ken Lassner shows advisors how to convert volatility into after-tax portfolio gains

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income