It’s every quant’s nightmare: Trades that look good on paper break down in the real world. And in the $1 trillion business of smart-beta investing, it’s happening on an industrial scale.

According to a new study, hundreds of strategies that showed significant outperformance in backtesting are failing to live up to their hype once they're packaged and sold as exchange-traded funds.

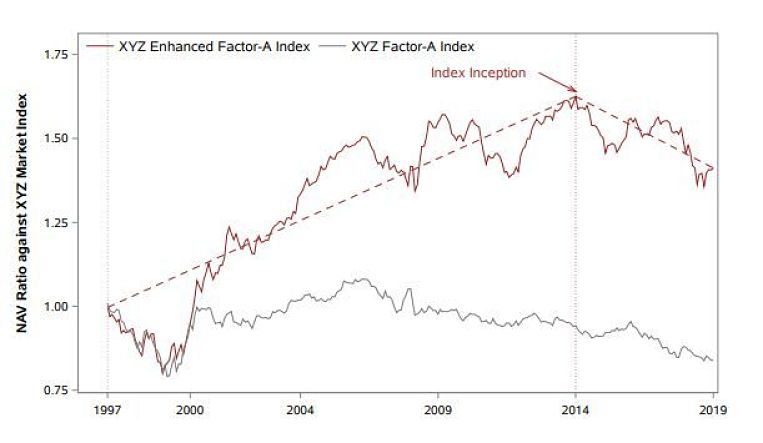

The average above-market return for smart-beta strategies is 2.77% per year before they are listed. That flips to a loss of 0.44% after fees once they actually become ETFs, according to researchers Yang Song at the University of Washington and Shiyang Huang and Hong Xiang at the University of Hong Kong.

“Stellar performance only exists in backtests and has no indicative power for ‘real’ performance,” the authors wrote. “We find strong support that data mining in backtests accounts for the performance deterioration.”

In other words, ETF sponsors are finding strategies that worked brilliantly according to their historic data -- but that aren’t working now.

Of more than 700 U.S.-listed smart-beta ETFs, about 60% have undershot their indexes since the start of this year, according to data compiled by Bloomberg. The median fund has lost about 1.5% on a total return basis, compared with a more than 10% gain for the Vanguard Total Stock Market ETF.

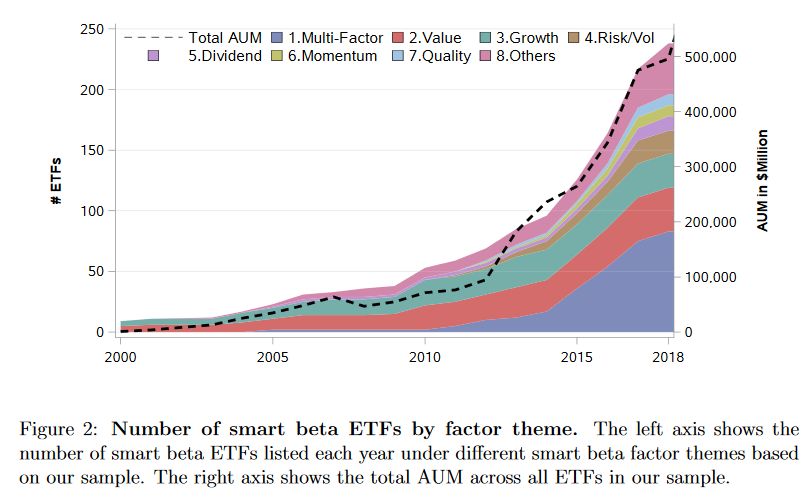

The booming smart-beta industry accounts for more than a fifth of the $4.8 trillion U.S. ETF market.

It’s a blend of active and passive investing that seeks to deploy popular quant strategies in an ETF wrapper. Rather than weight stocks simply by market capitalization like a vanilla index fund, it typically uses factors such as how cheap they are or their growth potential.

The research, titled “The Smart Beta Mirage,” is the latest in a series of criticisms leveled at industry, but smart beta still has plenty of advocates. The strategies used by the investing style are designed to work over the long term, so periods of underperformance are expected and deviation from the benchmark is practically by design.

Smart beta fans like Rob Arnott of Research Affiliates have repeatedly argued that the basic concept of breaking the link between market capitalization and weighting in a portfolio still holds good -- even if the industry’s breakneck growth has stretched the definition.

Nonetheless, the new study’s findings echo much earlier observations in the ETF sphere.

A white paper from Vanguard Group in 2012 identified a pattern among indexes created for fund launches using backfilled performance data in which most fared well before inception but generated weaker returns once turned into ETFs.

A $141M judgment and a federal asset freeze collide over one shrinking pool

The firm's CFO and EVP of Wealth Management Solutions are the latest executives to exit the broker-dealer.

Clients are saying they would consider switching advisors if another professional offered estate planning services, according to a new Trust & Will survey.

CEO Laurel Taylor says the fintech's composable AI stack helps workers optimize dollars across Trump Accounts, 529s, 401(k)s, and other employee benefits.

The bank has swiped three private banking veterans from BNY as the city climbs the ranks of America's fastest-growing wealth hubs.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.