Why advisors who treat intergenerational planning as ongoing will be the ones who endure

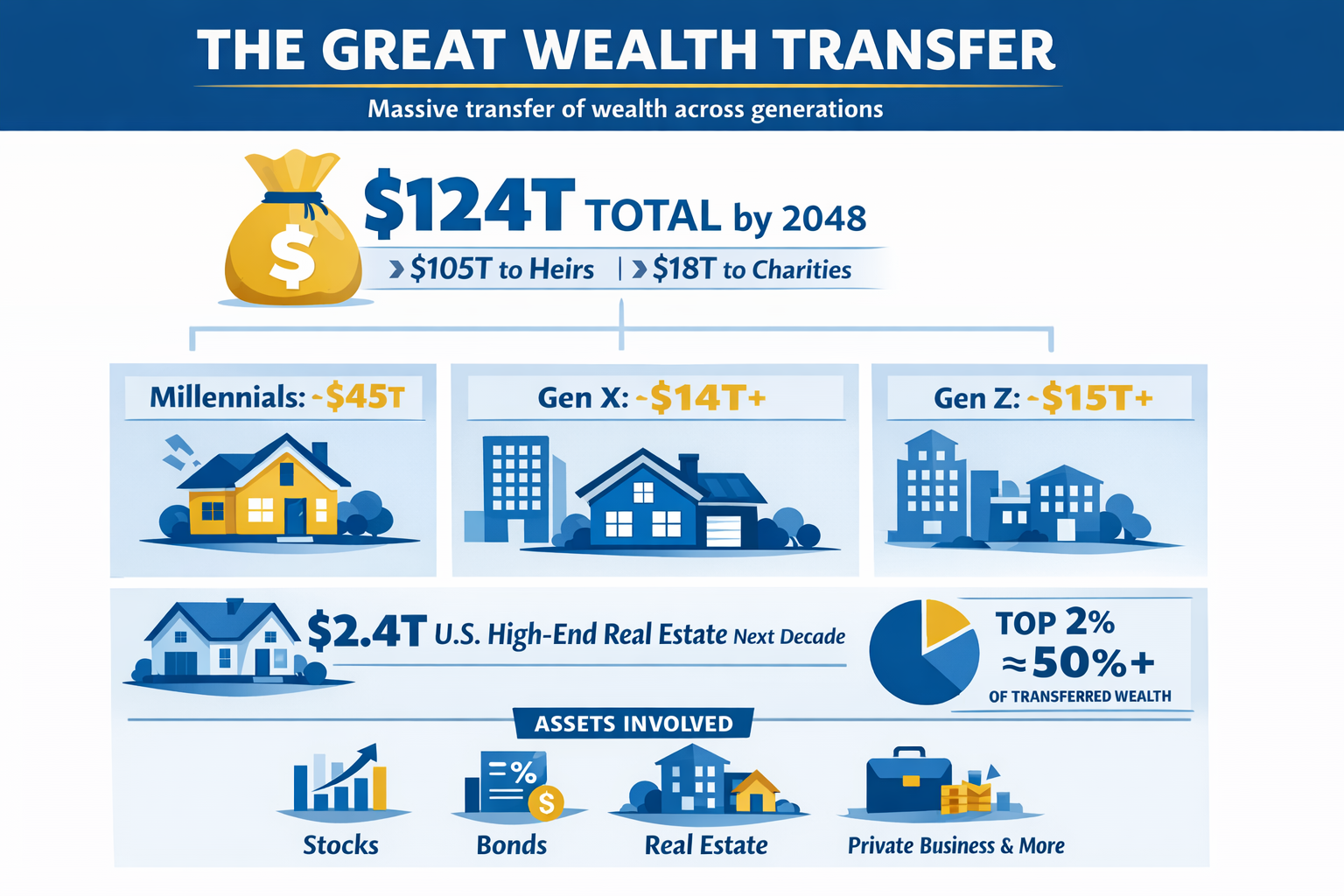

The “great wealth transfer” is often described as a once-in-a-generation moment for advisors. In my experience, that framing misses what is truly at stake. Wealth transfer is not a single transaction triggered by death. It is an ongoing, multi-decade planning process that should be embedded in every relationship involving intergenerational wealth.

When advisors focus solely on the eventual handoff of assets, they miss two critical responsibilities: transferring wealth tax-efficiently and preparing the next generation to receive it responsibly. Done well, wealth transfer planning is as much about people as it is about money.

One of the biggest misunderstandings I see across the industry is the assumption that wealth transfer happens all at once. In reality, families with intergenerational wealth should be planning continuously – long before assets change hands.

That planning includes evaluating how assets will move from one generation to the next from a tax perspective, but it also involves something far more nuanced: helping heirs understand what inherited wealth will mean for their lives. Without that preparation, even well-structured transfers can create confusion, stress, or unintended consequences for the next generation.

Wealth transfer should be an ongoing conversation, not a future milestone.

Large inheritances can create real challenges if beneficiaries are not prepared to manage them. In nearly every situation I work on, trusts play a central role in addressing that risk.

Trust structures are not one-size-fits-all. For responsible adult children, access to assets may be granted at specific ages or in graduated stages – for example, partial access in midlife with full access later. In other cases, particularly where there are special needs or concerns about financial decision-making, trusts are designed to provide support without direct control over the assets.

The goal is not restriction for its own sake. It is alignment – ensuring that the structure of the inheritance reflects both the donor’s intentions and the beneficiary’s ability to manage wealth responsibly.

Equally important is trustee selection. Putting the right people in the right seats is essential to carrying out the donor’s wishes. A well-designed trust can still fail if the governance behind it is weak.

Wealth transfer planning touches every corner of a family’s financial life: investments, taxes, estate planning, business interests, and income needs. Approaching these elements in isolation is where problems tend to emerge.

Our role is to serve as the quarterback of the process. While we have deep expertise in investment management and tax-aware planning, true integration requires collaboration. That means coordinating closely with CPAs, estate attorneys, and other specialists to ensure that every piece fits together.

Siloed advice creates gaps. Integrated planning creates clarity. Families benefit most when their advisory team is aligned around a single set of objectives and communicates effectively across disciplines.

One of the most important – and often overlooked – aspects of successful wealth transfer is relationship-building with heirs well before any assets change hands.

We make a point of meeting with our clients’ children early, establishing relationships long before those children ever inherit anything. When the parents eventually pass away, we do not want our first interaction with the next generation to happen during a moment of grief or uncertainty.

In many cases, we are already managing assets for those children or providing planning support. That continuity makes the transition far more seamless during what is often a very difficult time.

It’s also worth noting that many inheritors are not young adults. Often, they are in their 50s or 60s, well into their working lives. Their planning needs frequently resemble those of their parents, making the transition more of a continuation than a reinvention.

There is a perception that younger generations approach investing very differently – taking more risk or gravitating toward alternative strategies. In practice, I do not see dramatic differences.

Risk is risk, regardless of how it is packaged. While younger investors may be more inclined toward diversification through exchange-traded funds and less interested in individual stock selection, their underlying risk tolerance is often similar to that of prior generations.

The fundamentals still apply. Sound diversification, disciplined portfolio construction, and long-term planning remain the foundation, regardless of age.

Advisors who successfully retain and grow relationships through the wealth transfer are rarely doing anything flashy. They are acting consistently as fiduciaries and extending that mindset naturally to the next generation.

That does take effort. It is easier to postpone meetings with clients’ children or assume relationships will fall into place later. In my experience, making that extra effort strengthens the bond with the current client and lays the groundwork for continuity.

When done correctly, the transition feels seamless – not forced.

Philanthropy plays a significant role in many wealth transfer conversations. For families with substantial assets, giving is often a core source of meaning and purpose.

Many parents intentionally include their children in philanthropic decisions, whether through direct charitable giving, family foundations, or donor-advised funds. These conversations are not just about dollars. They are about values.

For many families, the legacy they care most about is not simply what they leave behind financially, but how they teach the next generation to think about generosity, responsibility, and impact. In that sense, philanthropy becomes both a financial strategy and a form of parenting.

Wealth transfer is not just about moving assets. It is about preparing people. Advisors who understand that distinction – and plan accordingly – will be the ones who remain relevant across generations.

Advisors are navigating a new reality as clients pre-consult ChatGPT before meetings

Chuck Roberts and Stifel have been facing scrutiny due to sales of structured products and structured notes.

The bankrupt fintech platform, which had drawn users seeking access to pre-IPO shares of tech startups, claims a last-minute breach of contract threatens to delay recovery for more than 13,000 defrauded customers.

Appointment extends a run of senior hires as Northern Trust builds out complex-wealth services for entrepreneurs and multigenerational families.

Agency notice opens comment period on the federal match as retirement experts weigh the program's reach for underserved savers.

Northern Trust’s Ken Lassner shows advisors how to convert volatility into after-tax portfolio gains

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income