For most people, December is the month for giving. But when it comes to taxes, January should be the time to start the planning process for maximizing the tax benefits of donating to charity. One of the best ways to do this is by using qualified charitable distributions (QCDs) from IRAs, because IRAs are the best funds to give to charity.

Qualified charitable distributions allow IRA owners (and IRA beneficiaries) who are age 70½ or older to make their charitable contributions directly through their IRAs. The funds must be directly transferred from the IRA to the qualifying charity, but the distribution from the IRA will generally be tax-free.

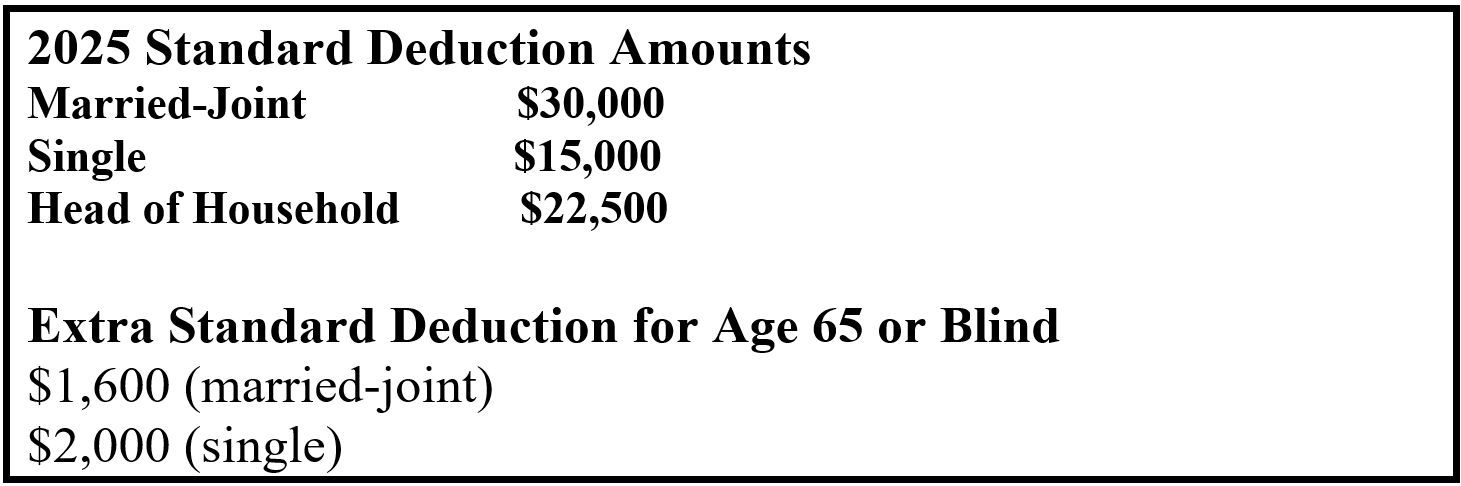

The QCD provides a tax benefit that could otherwise be lost. Most older IRA owners no longer receive any tax benefits from the charitable gifts they make because they don’t itemize their deductions. Instead, they use the standard deduction, which for most is much higher. For 2025, that standard deduction for seniors has now increased (due to cost-of-living indexing) to $33,200 for a married couple filing jointly ($30,000 base amount plus the additional standard deduction of $1,600 each for those age 65 older = $33,200). The 2025 standard deduction for older single individuals has increased to $17,000 ($15,000 base amount plus the additional standard deduction of $2,000 = $17,000).

While the itemized deduction won’t be available for those using the standard deduction, the QCD provides a better tax benefit. That’s because the QCD is an exclusion from income that reduces AGI (adjusted gross income), and AGI is a key number on the tax return that many tax credits, deductions and other tax benefits are based on.

QCDs can produce these specific tax benefits:

-As discussed later, QCDs can offset RMDs (required minimum distributions) and thereby reduce “stealth taxes” based on what would otherwise be taxable RMDs.

- QCDs can increase medical deductions, which might otherwise be limited based on AGI.

- QCDs can lower Medicare IRMAA surcharges, in some cases substantially.

- QCDs have the effect of adding to the standard deduction by, in effect, allowing the charitable deduction (without itemizing). Keep in mind, however, that if the QCD is used, an itemized deduction for that same contribution cannot be taken. That would be double-dipping.

- QCDs can benefit those who may have their charitable contribution deduction limited on account of AGI.

- QCDs can increase rental real estate loss deductions, which might otherwise be limited because of AGI.

- QCDs can help qualify for the 20% Qualified Business Income Deduction for pass-through/self-employed business owners.

- Estate planning – QCDs can help reduce the value of traditional taxable IRA funds being left to heirs, especially since most beneficiaries will have to withdraw and pay tax on the inherited IRA funds within 10 years after death. It’s better tax-wise to do charitable giving with taxable IRA funds via QCDs where they are removed from the IRA tax-free.

QCDs will almost always save taxes – and they will never raise taxes.

In addition, for those subject to RMDs (required minimum distributions), the QCD can offset that RMD income, but only if done in the right order.

This is why January is the best time for those subject to RMDs to do QCDs. Yes, the season of giving is in December, but if an RMD for the year has already been taken earlier in the year, then a QCD done after that cannot offset that RMD income.

For those who plan to make charitable contributions in 2025, and who qualify for QCDs (IRA owners or beneficiaries who are age 70 ½ or older), do the QCDs early in the year (or before taking RMDs) so they can offset RMD income.

Here is the way the QCD/RMD ordering should work:

The right way:

Assume Joe (age 76) has an RMD in 2025 of $10,000, but Joe also wants to make $15,000 of charitable contributions for 2025. If Joe first does the QCD of $15,000, then his IRA RMD is fully satisfied for the year and does not have to be taken. The result is a total 2025 IRA distribution of $15,000, all of which is tax free and satisfies Joe’s RMD for the year.

The wrong way:

If, on the other hand, Joe takes his $10,000 RMD earlier in the year, before making his charitable contributions, then any QCD done after that cannot offset his RMD income. If Joe does his $15,000 QCD after he’s already taken his RMD, the QCD will still be distributed tax free from the IRA, But the result is a $25,000 total IRA distribution for 2025, of which $10,000 is taxable.

1. QCDs only apply to IRA owners or beneficiaries age 70½ and over, and for 2025 QCDs are capped at $108,000 per IRA owner, not per IRA account.

2. QCDs apply to IRAs, Roth IRAs and INACTIVE SEP and SIMPLE IRAs. It does NOT apply to distributions from any employer plans. As discussed in #12 below, do not use Roth IRAs for QCDs.

3. QCDs only apply to direct transfers of IRA funds to charities and not gifts made to private grant making foundations or donor advised funds.

4. No split-interest gifts of any type will qualify.

A one-time QCD of $54,000 (for 2025) can go to a split-interest entity, such as a charitable remainder annuity trust, charitable remainder unitrust or a charitable gift annuity. But donor-advised funds still do not qualify.

5. The QCD can satisfy an RMD, turning the RMD into a non-taxable distribution.

6. If a QCD is done, no itemized tax deduction can be taken for the same charitable contribution.

7. For a married couple where each spouse has their own IRAs, each spouse can contribute up to $108,000 from their own IRAs. But a married couple filing jointly cannot use each other’s QCD amount. Each spouse’s limit applies to their own IRA.

8. If more than $108,000 is withdrawn from the IRA and contributed to a charity, there is no carryover to a future year. The excess is taxable income, and a charitable deduction can be claimed if the taxpayer itemizes.

9. The contribution to the charity would have had to be entirely deductible if it were not made from an IRA. There can be no benefit back to the taxpayer.

10. The distribution from the IRA to a charity can satisfy an outstanding pledge to the charity without causing a prohibited transaction.

11. The charitable substantiation requirements apply. You must have a CWA (contemporaneous written acknowledgment), in essence, a receipt showing no other benefits back to the giver.

12. QCDs apply only to taxable amounts. This is an exception to the usual pro-rata rule that applies when someone with both pre-tax and after-tax IRAs takes a distribution. Technically, taxable amounts in a Roth IRA will qualify, but practically it makes no sense using Roth IRAs for making QCDs. These Roth funds have already been taxed.

One extra QCD quirk…

A QCD could become taxable if a deduction is taken for making an IRA contribution, so don’t do that. Contribute to a Roth IRA instead.

Start the year off right with QCDs and tax savings!

For more information on Ed Slott and Ed Slott’s 2-Day IRA Workshop, please visit www.IRAhelp.com

Todd Bryant of Signature Wealth Partners on vanishing pensions, SECURE Act 2.0, and what clients really want to know.

Merrill's latest hires span Colorado to Louisiana, even as industry-wide recruiting data suggests the firm is losing almost as many advisors as it gains.

The $36 million buy allegedly hid inflated books and a $50 million diversion.

“An award citing emotional distress is very unusual,” an industry executive said.

New EBRI research found workers who participated in employer financial education reported higher confidence, literacy and financial satisfaction.

Northern Trust’s Ken Lassner shows advisors how to convert volatility into after-tax portfolio gains

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income