For both clients and advisers, the decumulation phase of retirement can be one of the most challenging to plan for — not to mention navigate in real time.

Individuals face unique risks once they reach retirement, and even the most affluent retirees are often reluctant to spend down their assets. In fact, research shows that few retirees are systematically drawing down their retirement portfolios to supplement spending. Only 22% of retirees plan to spend down their financial assets, whereas 32% plan on maintaining their assets by withdrawing only earnings. Some even continue to save in retirement.

Today’s low-interest-rate environment adds to the stress of establishing a retirement strategy as the "cost" of generating retirement income from a portfolio of stocks and bonds is now higher. Historically, from 1870 to 2015, it cost $26,267 in savings to produce $1,000 of annual income with a 50/50 portfolio. As of January 2021, investors need about $79,118 to reap that same $1,000. Understanding your clients’ portfolio and how it is positioned to support them through an evolving rate environment is imperative.

In an effort to dig deeper into decumulation amid evolving interest rates, we explored three common strategies that retirees tend to rely on to fund retirement: spending only dividends and interest, building a bond ladder and leveraging guaranteed income. Let’s look at the risks and benefits of each strategy.

• Spending only dividends and interest. In the past, individuals could maintain pre-retirement lifestyles in retirement by implementing an income-focused asset allocation strategy and spending only income generated from their portfolios. This is because dividend yields and interest rates exceeded reasonable withdrawal rates (e.g., 4%). While ultra-high-net worth clients can afford to live off dividends and interest, most retirees will have to spend down portfolio principal or seek alternative sources of income to achieve their desired lifestyle.

Additionally, yields on both dividends and interest-bearing investments have declined steadily over the years and, as noted above, it has become increasingly expensive to generate needed income.

• Building a bond ladder. Another common approach is to build a bond ladder. This is done by investing in a range of bonds with different maturities and then collecting the interest and principal as those bonds mature to fund the necessary income each year in retirement. However, since retirees must choose how long the income needs to last when building the ladder, this requires some assumptions around longevity.

• Leveraging guaranteed income. A third approach is to cover the costs of fixed expenses with an income annuity, to be leveraged alongside investments that could provide growth, to serve as a means to provide retirement income needs through a lifetime guarantee. While some advisers may balk at the illiquid nature of income annuities, they offer retirees peace of mind and have become even more valuable relative to other investments in the current interest-rate environment. This is because of mortality credits, which are unique to annuities and represent a larger portion of payouts as interest rates drop.

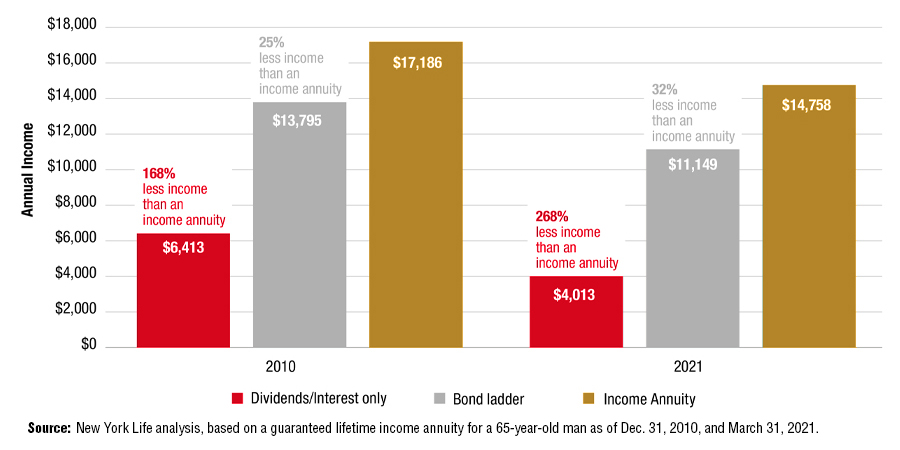

Consider the following hypothetical example, which assumes that a 65-year-old man has $250,000 in retirement savings to use for each of the three strategies described.

Historically, income annuities have provided more income relative to spending from a 50/50 stock and bond portfolio or building a bond ladder. In 2021, income annuities provided an even better value relative to the other strategies in this scenario. While the 10-year Treasury has dropped below 2%, the difference between the income from the income annuity and other two strategies has increased significantly. Of course, there is no residual value with annuities as there might be with bonds and other investments.

Especially in this environment, advisers are challenged to design a safe spending strategy in line with clients’ risk tolerance that allows them to achieve their desired retirement lifestyle — without running out of money.

It may seem like a tall order to achieve, but by considering the inclusion of income annuities as part of an overall strategy, that challenge may be a little bit easier to overcome.

Phil Caminiti is a vice president with New York Life Insurance Co.

“It’s time for an economic reset,” wrote the California governor, in a post on X.

Masterworks was launched in 2017 but its RIA, Masterworks Advisers, is just three years old.

One 2017 form, no broker license, and a $42 million gap they say surfaced on a webinar.

Fewer than half of Americans in their peak earning years feel on track for retirement, while many say limited financial knowledge and access to professional guidance are holding them back.

Meanwhile, Wells Fargo hauled advisors overseeing $825 million in the West Coast, while Wedbush has welcomed a seasoned professional from Stifel in California.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.