The stampede to passive strategies has been relentless. But most core active fixed income strategies, unlike their equity counterparts, have tended to outperform their benchmarks.

It could be time to re-evaluate active fixed income.

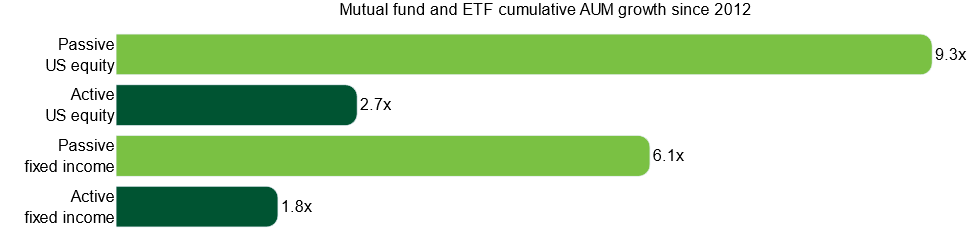

Passive US equity strategies have grown ninefold since 2012, possibly due to complaints about expensive fees and questionable performance within active vehicles.

Figure 1: Investors have stampeded into passive strategies

Source: Bloomberg Intelligence, March 2025.

It is hard to deny active equity funds have something to answer for: 77 percent of large-cap funds failed to beat the S&P 500 net of fees over 10 years (according to Morningstar data to February 2025).

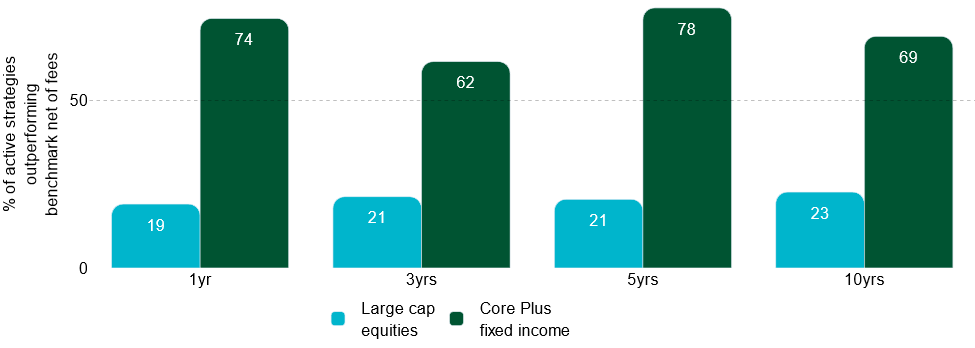

However, a migration to passive core fixed income is less understandable on these grounds. Almost 70 percent of Core Plus strategies have beaten the Bloomberg US Aggregate Bond Index (otherwise known as the “US Agg”) over the 10 years to February 2025 (see Figure 2). In our view, much of this relates to structural inefficiencies within fixed income indices.

Figure 2: Many active Core Plus strategies have beaten the US Agg

Source: Morningstar, Insight, based on net of fees performance data to end of February 2025. Equity benchmark: S&P 500. Core Plus benchmark: Bloomberg, US Aggregate Bond Index. Past performance is not indicative of future returns.

Whereas markets assign the highest equity index weights to the most profitable companies (or those the market thinks will be the most profitable), fixed income benchmarks assign the most weight to issuers with the most debt (or bonds) outstanding. While those issuers are not always the most leveraged, it is hardly a natural way to allocate to the most suitable issuers.

This may be particularly notable in the case of the “US Agg”, which typically serves as the benchmark for US Core and Core Plus strategies. Half of the Agg is allocated to US Treasuries and government-related debt. An active strategy can simply take a large Treasury underweight and a large credit overweight (see Figure 3), potentially enhancing yield and expected returns.

Figure 3: The “Agg” is heavily allocated to Treasuries at the expense of corporates

Source: Bloomberg, Insight, for illustrative purposes only, March 2025.

We would also recommend tactical allocations to off-benchmark markets like high yield and emerging markets. We also believe in expanding the scope of an ABS allocation to include off-benchmark sectors like CLOs and “esoteric” assets like data center-backed deals or whole-business securitizations.

Fixed income indices undergo more frequent compositional changes than equity indices. Where equity markets saw $580 billion of IPOs in 2024, credit markets saw $1.8 trillion of new issuance across investment grade and high yield (according to Bloomberg).

In the same way that equity IPOs tend be priced conservatively, new corporate bonds are usually syndicated to primary investors “new issue premiums” relative to comparable debt.

This can reward active managers participating in deals. Passive strategies can typically only purchase the deals in the secondary market at the end of the month, missing any initial gains.

As passive strategies have grown in popularity, their synchronized monthly rebalancing flows have wider and predictable impacts on market pricing. This can be a potential source of alpha.

For example, when an issuer is downgraded from investment grade to high yield (known as a “fallen angel”), passive investment grade accounts, such as the $468 billion of passive “Agg” funds alone (per Bloomberg data), are forced to sell the bond at the same time.

Our analysis shows this causes an average -10 percent excess return over the six months before a bond’s transition from investment grade to high yield. Over the subsequent year, however, the bonds have typically recovered, delivering +11 percent excess returns on average .

While passive funds are typically “price takers” in these situations, active managers can either retain freshly downgraded fallen angels or purchase them post-downgrade at potentially depressed valuations. We expect fallen angels to be a key theme in 2025, which has started with over $16bn of such downgrades.

Active fixed income managers have several tools such as security and sector selection, relative value trades across regions, currencies or within a single issuer’s capital structure as well as duration and yield curve positioning.

This is not to say that fixed income managers have historically outperformed across every asset class. Exceptions have tended to be less liquid markets like US high yield. However, passive high yield managers have also struggled in this area too, with trading costs and frictions consistently compromising returns (based on eVestment data to the end of 2024). We believe advisors may wish to consider highly liquid systematic management strategies for dedicated allocations to markets like high yield.

However, for core fixed income allocations, we believe that active management can add material value to a strategy. And the rise of passive investing, if anything, has enhanced their opportunity sets.

It could be time to take another look at core active fixed income approaches.

Brendan J. Murphy is head of fixed income, North America at Insight Investment.

Advisors are navigating a new reality as clients pre-consult ChatGPT before meetings

Chuck Roberts and Stifel have been facing scrutiny due to sales of structured products and structured notes.

The bankrupt fintech platform, which had drawn users seeking access to pre-IPO shares of tech startups, claims a last-minute breach of contract threatens to delay recovery for more than 13,000 defrauded customers.

Appointment extends a run of senior hires as Northern Trust builds out complex-wealth services for entrepreneurs and multigenerational families.

Agency notice opens comment period on the federal match as retirement experts weigh the program's reach for underserved savers.

Northern Trust’s Ken Lassner shows advisors how to convert volatility into after-tax portfolio gains

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income