I'm really not in the business of trying to predict a recession-driven market drop. Though it is tempting. What I will say is that there's rising risk in the market. I'm also going to say that if you're using typical risk measures, you will be getting it wrong, because these look at risk today by taking the standard deviation of returns over the past year or two. Clearly, what's happening now is not like what has been going on over the past two years.

What's happening now is high market vulnerability. There is high market and household leverage; high concentration, with 10 stocks making up a quarter of the S&P 500 market capitalization; and limited dry powder sitting on the market sidelines to supply liquidity if those levered in those concentrated stocks need to find an exit. And overarching the vulnerability is waning confidence.

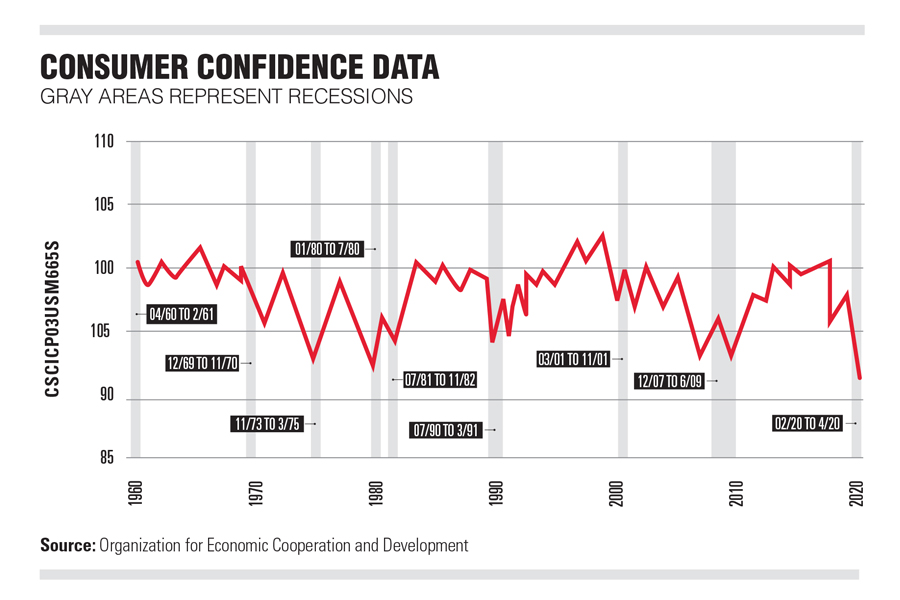

A number of consumer and business confidence surveys are in redline territory. As can be seen by this chart, the consumer confidence survey from the OECD is at its all-time low. And we're talking about the lowest level since 1960. Interestingly, but not surprisingly, the survey has been a great indicator of recessions, diving down before each of the eight recessions over the period.

Recessions and the related downturn for the markets are part economics, part psychology. They depend on the way people react when facing the economics, and their expectations of what the current state of the world holds for the future. They depend on whether investors see the world as a glass half full or a glass half empty. Right now it looks to me to be half empty, meaning consumers will be thinking twice about discretionary purchases and producers will be hunkering down, holding less inventory and putting off capital expenditures.

And low confidence means the markets discount for the worst case. If we're teetering near this state, if we're on the knife's edge for a change in market view, then even if we stand off from prognosticating which way things might fall, we can at least say the risk to the market has jumped. And teetering we are.

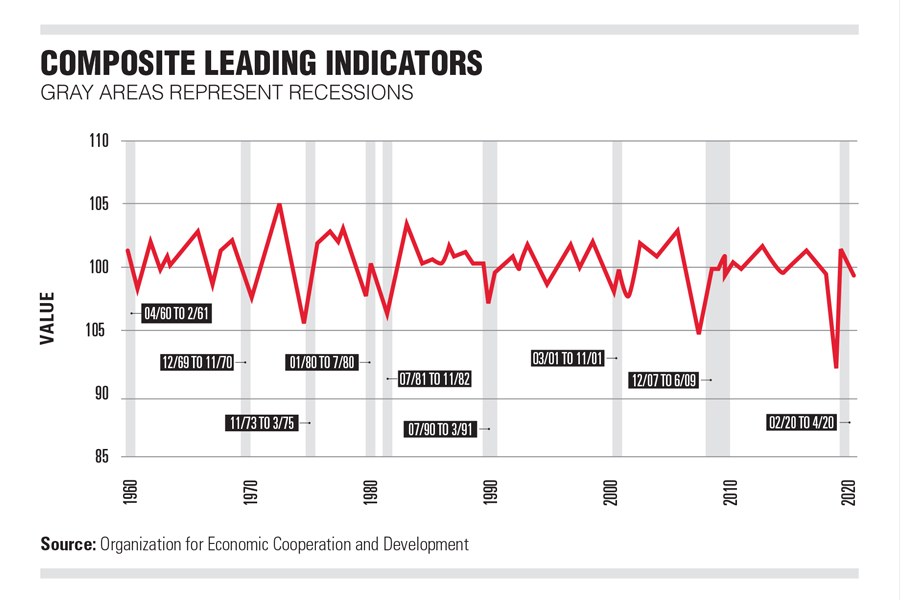

The OECD’s Composite Leading Indicator has hit for each of the eight recessions since 1960 with only two false positives. The index heading down below 99 means recession. Currently, it is heading down, at 99.02. We'll call that rounding error.

Does that mean a recession? You decide. But whichever way you go, clearly it does highlight vulnerability for a market with low confidence.

The statisticians among us will correctly argue that if you look at enough economic and confidence indexes, there are good odds that one will get eight out of eight. But still, there it is. At a minimum, it underscores the recession risk we're seeing in confidence and sentiment. And it warns against looking at current market risk with a glass-half-full view.

The bottom line: Risk going forward is a lot higher than it has been in the recent past. So take the numbers the risk models are handing you, and pump them up.

Rick Bookstaber is co-founder and head of risk at Fabric. He previously held chief risk officer roles at Morgan Stanley, Salomon Brothers, Bridgewater Associates and the University of California Regents, and served at the Treasury in the aftermath of the 2008 financial crisis. He’s the author of “The End of Theory” (Princeton, 2017) and “A Demon of Our Own Design.”

Choice anxiety, prestige bias, and the temptation to make selections based on outsourced confidence are just some of the parallels between investing and the world of wine tasting.

Regulators found Bank of America's monitoring software had a known flaw Merrill left uncorrected for years.

While AI has become a go-to research tool for affluent investors, new HSBC research suggests human advisors remain the deciding voice when investment decisions are made.

A 5-4 ruling preserves the Federal Reserve's independence for now, but the legal fight over presidential removal power is far from settled.

For years, large firms have been facing penalties and questions from regulators over interest rates for clients’ cash accounts.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.