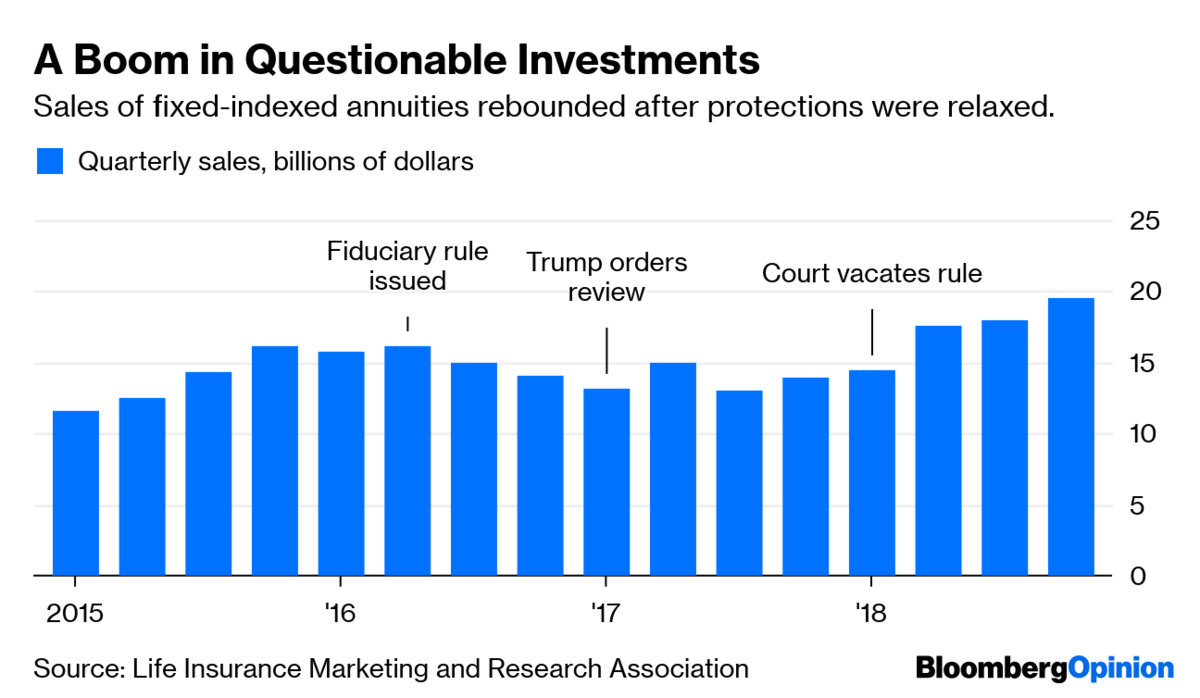

In New York state, which has unilaterally adopted aspects of the fiduciary rule, far fewer insurers sell such products.

How much do savers stand to lose? Consider one product that a major insurance company marketed to me: a 10-year annuity linked to the S&P 500 Index. Based on this annuity's formula and the price at which it was offered, a client would have foregone on average an estimated $54,000 in profit per $100,000 invested over any 10-year period going back to 1989. That's compared with a simple combination of U.S. Treasury bills and S&P 500 index funds that offers the same downside protection as the annuity with less credit risk and more liquidity.

The marketing materials an agent sent me seemed to play on fear, showing a potentially faulty comparison of the annuity's returns to the loss a pure stock position would have suffered during the 2008-09 crash. And the materials did not highlight crucial information such as hefty withdrawal fees and the insurance company's right to reduce payouts.

Such products are just the tip of the iceberg. Every year insurers come out with an array of new annuities employing "black box" strategies that are all but impossible for outsiders to understand. One could be forgiven for suspecting that some such strategies have been tweaked to make it difficult for a lay person to accurately assess their return potential.

(More: 5th Circuit denies states' second attempt to defend DOL fiduciary rule

No current efforts to improve standards — including one by the National Association of Insurance Commissioners – come close to the protections that the fiduciary rule would have provided. A strong form of the rule should be revived and applied to all investment accounts, not just retirement accounts. To be clear, there are upstanding insurers and agents who sell indexed annuities only when appropriate. Proper regulation wouldn't crimp those sales, but it would prevent over-prescription of such products to people whom they can harm.

Ethan Schwartz has worked as an investment manager and financial services executive for 21 years. He was a special assistant to the deputy secretary of the Treasury in the Clinton administration.

In New York state, which has unilaterally adopted aspects of the fiduciary rule, far fewer insurers sell such products.

How much do savers stand to lose? Consider one product that a major insurance company marketed to me: a 10-year annuity linked to the S&P 500 Index. Based on this annuity's formula and the price at which it was offered, a client would have foregone on average an estimated $54,000 in profit per $100,000 invested over any 10-year period going back to 1989. That's compared with a simple combination of U.S. Treasury bills and S&P 500 index funds that offers the same downside protection as the annuity with less credit risk and more liquidity.

The marketing materials an agent sent me seemed to play on fear, showing a potentially faulty comparison of the annuity's returns to the loss a pure stock position would have suffered during the 2008-09 crash. And the materials did not highlight crucial information such as hefty withdrawal fees and the insurance company's right to reduce payouts.

Such products are just the tip of the iceberg. Every year insurers come out with an array of new annuities employing "black box" strategies that are all but impossible for outsiders to understand. One could be forgiven for suspecting that some such strategies have been tweaked to make it difficult for a lay person to accurately assess their return potential.

(More: 5th Circuit denies states' second attempt to defend DOL fiduciary rule

No current efforts to improve standards — including one by the National Association of Insurance Commissioners – come close to the protections that the fiduciary rule would have provided. A strong form of the rule should be revived and applied to all investment accounts, not just retirement accounts. To be clear, there are upstanding insurers and agents who sell indexed annuities only when appropriate. Proper regulation wouldn't crimp those sales, but it would prevent over-prescription of such products to people whom they can harm.

Ethan Schwartz has worked as an investment manager and financial services executive for 21 years. He was a special assistant to the deputy secretary of the Treasury in the Clinton administration.

A $141M judgment and a federal asset freeze collide over one shrinking pool

The firm's CFO and EVP of Wealth Management Solutions are the latest executives to exit the broker-dealer.

Clients are saying they would consider switching advisors if another professional offered estate planning services, according to a new Trust & Will survey.

CEO Laurel Taylor says the fintech's composable AI stack helps workers optimize dollars across Trump Accounts, 529s, 401(k)s, and other employee benefits.

The bank has swiped three private banking veterans from BNY as the city climbs the ranks of America's fastest-growing wealth hubs.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.