Federal Reserve Chair Jerome Powell said the central bank could begin scaling back its asset purchases in November and complete the process by mid-2022, after officials revealed a growing inclination to raise interest rates next year.

Powell, explaining the U.S. central bank’s first steps toward withdrawing emergency pandemic support for the economy, told reporters Wednesday that tapering “could come as soon as the next meeting.”

That refers to the Fed policy gathering on Nov. 2-3, though he left the door open to waiting longer if needed and stressed that tapering was not meant to start a countdown to liftoff from zero interest rates.

“The timing and pace of the coming reduction in asset purchases will not be intended to carry a direct signal regarding the timing of interest-rate liftoff,” Powell said following the completion of the two-day gathering of the Federal Open Market Committee.

Powell said he didn’t expect the Fed to begin rate increases until after completing the taper process, which would wrap up “sometime around the middle of next year.”

“It is a bit faster than the last cycle,” said Jim O’Sullivan, TD Securities chief U.S. macro strategist. “He was very clear in the press conference that ‘soon’ means November.”

Back in 2014, the Fed took 10 months to complete the exercise of scaling back bond buying.

Powell’s performance was being parsed both by investors and the White House: The central bank chief’s term expires in February and President Joe Biden is expected to decide this fall whether or not to renominate him to another four years in his post. Bloomberg News has reported that White House aides are considering recommending the president keep him on the job.

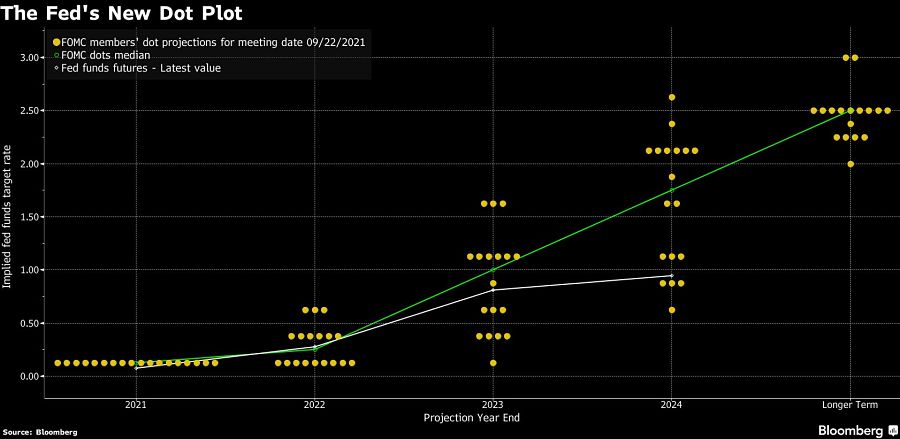

In addition to signaling a scale back in upcoming bond buying, the Fed also published updated quarterly projections that showed officials are now evenly split on whether or not it will be appropriate to begin raising the federal funds rate as soon as next year, according to the median estimate of FOMC participants. In June, the median projection indicated no rate increases until 2023.

The projections are not a policy commitment and reflect the personal views of policy makers, some of whom who may no longer be serving at the Fed next year. Biden is expected to fill an open slot on the seven-seat board in Washington as well as name two new vice chairs when the terms of the current incumbents — Richard Clarida and Randal Quarles — expire in coming months.

“The chairman is a dove among hawks,” said Diane Swonk, chief economist at Grant Thornton. “He would like to divorce tapering from liftoff and stressed the threshold for rate hikes is much higher than that for tapering.”

The U.S. rates market continued to price in a first hike around the start of 2023, although five-year Treasury rates rose as traders anticipated a slightly more aggressive path once benchmark increases begin.

That helped flatten the yield curve as long-end rates fell, while the Bloomberg dollar index gained after being whipsawed around the decision. U.S. stocks pared their advance.

The muted market reaction “is a very good outcome for the Fed in terms of signaling their intent to get the market information well ahead of the tapering decision,” said Jeffrey Rosenberg, senior portfolio manager for systematic fixed income at BlackRock Inc. “The Fed has to be pleased that their communication on the long-awaited tapering has avoided the dreaded fear of the tantrum.”

The FOMC decided to maintain the target range for its benchmark policy rate at zero to 0.25%, and continue purchases of Treasuries and mortgage-backed securities at a pace of $120 billion per month. The vote was unanimous.

Projections for 2024 were also published for the first time, with the median suggesting a federal funds rate of 1.8% by the end of that year. The median for 2023 rose to 1%, from 0.6% in the June projection.

“Participants generally expect a gradual pace of policy firming that would leave the level of the federal funds rate below estimates of its longer-run level through 2024,” Powell said.

“This is not a dovish outcome, but it is not an aggressively hawkish outcome either,” Krishna Guha, head of central bank strategy at Evercore ISI, wrote in a note to clients. “The equity market looks to be taking its early cue from the upbeat 2022 growth outlook and lack of a clear break to a 2022 hike.”

The Fed also said it would double the per-counterparty limit on its overnight reverse-repurchase agreement facility to $160 billion daily.

The U.S. unemployment rate fell to 5.2% in August, well below the April 2020 peak of 14.8%. But it’s still above the 3.5% rate that prevailed in February 2020, just before the pandemic struck. Fed officials have said they expect to keep the funds rate near zero “until labor-market conditions have reached levels consistent with the committee’s assessments of maximum employment.”

Inflation, according to the Fed’s preferred measure, was 4.2% in the 12 months through July, well above the central bank’s 2% target. Many Fed officials have said they expect it to return to around 2% after temporary supply-chain disruptions resulting from the pandemic have been resolved, though several have also cited the rapid price increases as a reason to begin raising rates as early as next year.

The move to charge data aggregators fees totaling hundreds of millions of dollars threatens to upend business models across the industry.

The latest snapshot report reveals large firms overwhelmingly account for branches and registrants as trend of net exits from FINRA continues.

Siding with the primary contact in a marriage might make sense at first, but having both parties' interests at heart could open a better way forward.

With more than $13 billion in assets, American Portfolios Advisors closed last October.

Robert D. Kendall brings decades of experience, including roles at DWS Americas and a former investment unit within Morgan Stanley, as he steps into a global leadership position.

Orion's Tom Wilson on delivering coordinated, high-touch service in a world where returns alone no longer set you apart.

Barely a decade old, registered index-linked annuities have quickly surged in popularity, thanks to their unique blend of protection and growth potential—an appealing option for investors looking to chart a steadier course through today's choppy market waters, says Myles Lambert, Brighthouse Financial.