As advisers, we all want to understand our payout structure, but oftentimes we don't know what, exactly, our real payout is. Spoiler alert: It's likely less — far less — than you think.

“Independent advisers start with a payout that is stated on their firm's grid, say 85% to 90%, but then must deduct two sets of charges to determine their actual net: program fees for their participation in fee-based programs and other 'miscellaneous' fees like technology, E&O, etc.," said executive recruiter Mark Elzweig. "When looking at these other ancillary costs, net payouts in the independent broker-dealer world are typically less (and at times far less) than the headline ‘90%.’”

I came from the independent broker-dealer world and was thrilled to have a 90% payout — right up until I saw the direct deposit hit my bank account. That's when I started to track my true net payout, or TNP.

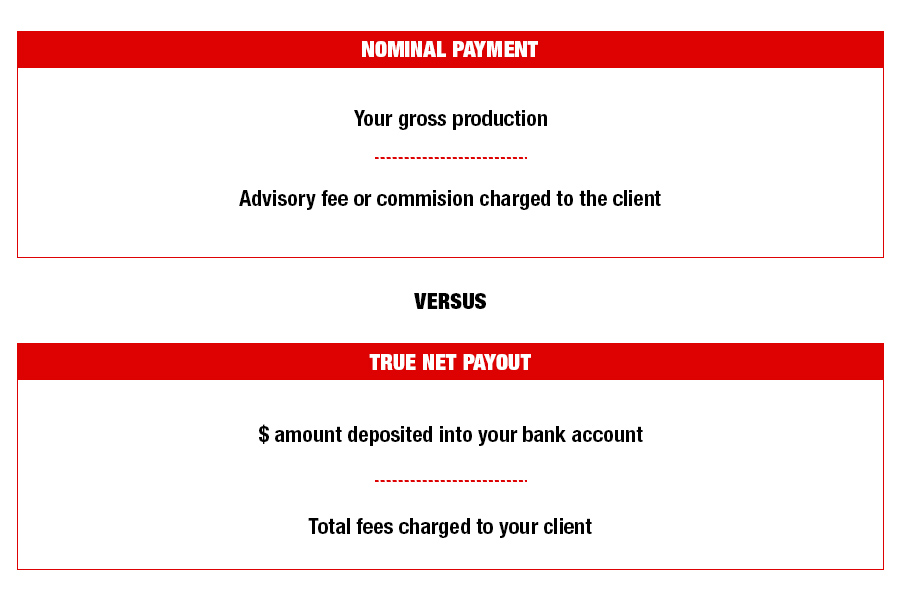

What we generally refer to as our payout is just our nominal payout and it's far from a full representation of the economics related to the relationship we have with our firms and clients.

You need to look at all haircuts assessed to both you and your clients.

Haircut No. 1: The nominal or headline payout.

This is the easiest haircut to quantify and usually the one most touted by firms as they try to recruit advisers.

Haircut No. 2: Ancillary fees that firms charge the adviser.

When calculating TNP, the numerator is easy to figure out — simply look at your bank statement and you'll see clearly what you received from your firm. By doing this, you will be able to parse out all the various ancillary fees your firm charges that are not accounted for within your “nominal” payout percentage. Ancillary fees often charged to advisers include:

• Platform fees.

• Registrations/E&O.

• Tech charges.

• B-D oversight fees for hybrid IBDs.

I know there are many more charges that can be listed here, but you get the idea. Also, to be clear, I'm not saying the fees are unwarranted. I'm simply saying that you should be aware of them, and you should include them as you calculate your TNP. These fees can easily deduct 5 to 10 basis points of payout from a fee-based book at IBDs, and more at the wirehouses. So even with just this second round of haircuts, that 90% payout could already be below 80%. But wait, there’s more.

Haircut #3: Ancillary fees that firms charge your clients.

The denominator in the TNP calculation is much more difficult to nail down and the least transparent and it's often ignored. It is also a significant source of revenues for firms, broker-dealers and registered investment advisers alike.

The denominator — the ancillary fees charged to your client — is where I usually see the greatest reduction in TNPs. In other words, it may be the case that your clients are bearing the brunt of the costs for you to have a 90% nominal payout.

“For fun I like to read broker-dealers’ third-party compensation and related conflict-of-interest reports as well as ADVs,” said Michael Gordon, managing partner of an eponymous consulting firm that works with advisers who are transitioning. “It’s probably the adviser version of reading a prospectus. One of the more common conflicts that add to the cost for clients is the non-transaction fee list. This means that for certain funds and ETFs, there are no ticket charges, however, these same fund and ETF companies pay the broker-dealer .25% on customer assets for this privilege.”

No-transaction-fee lists are one of the most common ways an adviser’s TNP decreases, but NTFs are not the only thing to be aware of. Here are ancillary fees often charged to clients:

• Ticket charges.

• Markups on investment products like structured notes.

• Increases in expense ratios due to NTF lists.

• Asset management surcharges (above what the asset manager actually charges).

In my experience reviewing pro formas for advisers, it's common to find 20 basis points, 30 bps or even 50-plus bps in client savings with solutions found in today’s uber competitive RIA space.

Of course! At the end of the day, there's a range of what it's reasonable to expect clients to pay (in total) for the services we deliver to them. If they're paying 20, 30 or 50 basis points more than needed to your firm for the ancillary charges detailed above, that means your advisory fees are essentially reduced by that same amount.

• As a conscientious adviser, this should bother you.

• As a businessperson looking to maximize your bottom line, this should interest you.

• As a fiduciary, this should scare the heck out of you.

The moral of all this is to be sure you do for yourself what you do every day for your clients: quantify, quantify, quantify.

Only you can judge whether the costs you and your clients pay to your firm are in line with the value you and your clients receive from your firm. The only way you can make this judgement is to first crunch the numbers – all the numbers. So if you're thinking about going RIA, be sure to look at your TNP based on where you are now versus where you could be. I think you'll be pleasantly surprised at what's available out there.

Come on in, the water’s great!

Chuck Failla is principal at Sovereign Financial Group Inc. If you have any questions, comments or story ideas, email him.

After a two-year period of inversion, the muni yield curve is back in a more natural position – and poised to create opportunities for long-term investors.

Meanwhile, an experienced Connecticut advisor has cut ties with Edelman Financial Engines, and Raymond James' independent division welcomes a Washington-based duo.

Oregon-based Eagle Wealth Management and Idaho-based West Oak Capital give Mercer 11 acquisitions in 2025, matching last year's total. “We think there's a great opportunity in the Pacific Northwest,” Mercer's Martine Lellis told InvestmentNews.

Osaic has now paid $17.2 million to settle claims involving former clients of Jim Walesa.

Osaic-owned CW Advisors has added more than $500 million to reach $14.5 billion in AUM, while Apella's latest deal brings more than $1 billion in new client assets.

Orion's Tom Wilson on delivering coordinated, high-touch service in a world where returns alone no longer set you apart.

Barely a decade old, registered index-linked annuities have quickly surged in popularity, thanks to their unique blend of protection and growth potential—an appealing option for investors looking to chart a steadier course through today's choppy market waters, says Myles Lambert, Brighthouse Financial.