At the 2020 InvestmentNews RPA Convergence Broker-Dealer Roundtable and Think Tank, one of the challenges that emerged was the cost of rampant record-keeper consolidation. It’s inevitable in a maturing fragmented industry, but when a provider like Empower Retirement acquires a business like MassMutual’s record-keeping division, broker-dealers must spend valuable and limited resources.

Edward Jones is notorious for being incredibly careful about allowing record keepers onto its system, spending many months, if not years, conducting intense due diligence.

“We have a six-to-nine-month due diligence process with just eight to nine partners,” said John Davis, the firm’s principal of retirement products. The evaluation process not only examines services and capabilities, but also which firm is likely to survive long-term.

The change in ownership of MassMutual’s record-keeping business means that Edward Jones must conduct unscheduled due diligence. After all, MassMutual is on the Edward Jones platform, but Empower is not. That is interesting, as MassMutual was able to get on the Edward Jones approved list when it purchased The Hartford’s record keeper.

Though not all broker-dealers have the same intense due diligence process, all of them need to evaluate the new record keeper’s services and capabilities. Even if they have approved MassMutual and Empower on their system, broker-dealers should be conducting a new due diligence process to determine which services are being kept and eliminated. There will be a new entity, even if the name does not change.

Record-keeper consolidation is difficult for advisers as well. Clients must change providers and systems, which can be time-consuming, and not just for the additional due diligence they need to conduct as fiduciaries. Even more damaging are the incessant calls to the clients of the acquired provider by poaching advisers.

And think about a plan sponsor that an adviser recently placed at the acquired provider. The client will be forced to go through another conversion process, which does not make the adviser look good. Even if it’s not their fault, it is their problem.

This all demands a lot of time from valuable people, yet there is little if any additional revenue for the adviser and broker-dealer.

There is also a human factor in this. Record-keeper consolidation is being driven, in part, to cut costs, which means eliminating jobs. Think about the jobs lost at MassMutual, especially sales professionals — picture their faces. Do we think there will be more wholesaler positions in the future? In the past, many record-keeper wholesalers were able to move to fund companies, but those positions are also being eliminated.

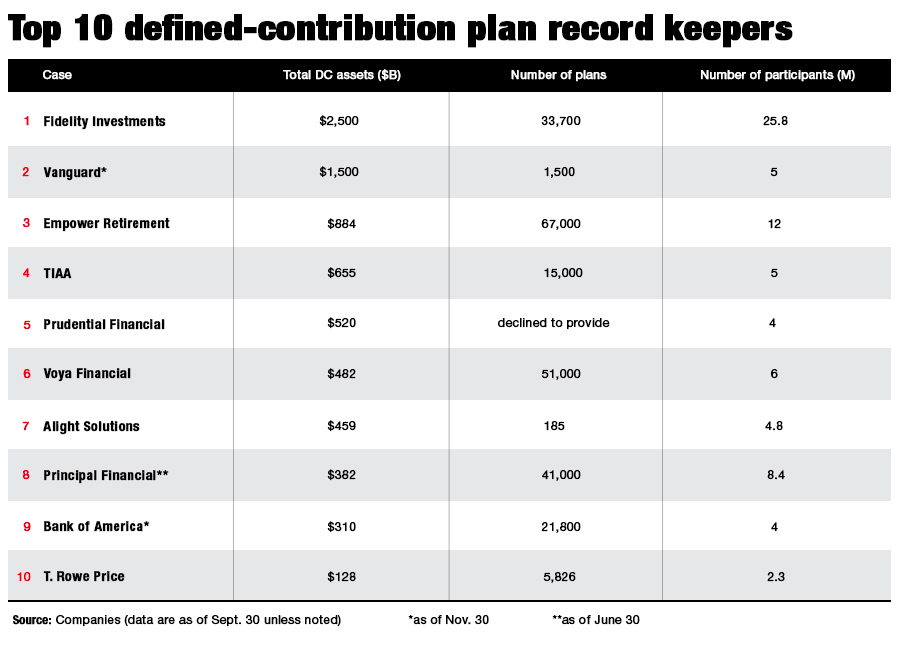

Record-keeper consolidation will undoubtedly continue. Even with the recent Empower acquisition, there are still 43 national providers serving the 401(k) industry, where scale matters. The top five have more than 75% of the adviser-sold DC assets and participants, leaving the other 38 to fight over a dwindling 25%.

What should distributors and advisers do?

It’s safer to put more business with the top five record keepers, which have resources to compete. But as they get better, more of them compete with advisers to service and monetize participants. Fidelity and Vanguard are very open about their intentions, but why do you think Empower, now with 12 million participants, paid $1 billion to buy Personal Capital?

Others like Raymond James, with its purchase of NWPS, a national record keeper based in the Northwest, may see opportunities to control the participant’s digital experience and data. Others are starting to partner with fintech record keepers like Vestwell that are happy to be the “Intel inside" and share data.

It’s easy to say that advisers and distributors need to choose wisely, but just as with investments and fiduciary duties, the process is paramount, with no guarantee of results. How many distributors and advisers have a documented due diligence process conducted by prudent experts periodically?

Fred Barstein is founder and CEO of The Retirement Advisor University and The Plan Sponsor University. He is also a contributing editor for InvestmentNews’ RPA Convergence newsletter.

Flyer on wealth management data aggregation, AI agents, and closing the insight-to-action gap.

Chirayu Rana has added two executives as defendants after dropping his state case against JPMorgan Chase last week.

A class action over the digital brokerage's cash sweep program only hints at an industry-wide reckoning over how client cash is handled, says Gary Zimmerman.

New tool lets advisory teams manage shared retirement-plan accounts en masse as Vanguard retirement plan data show rising exposures to equities across demographics.

Three in four Americans can’t estimate their net worth without checking an app or account, according to a new Western & Southern survey.

Northern Trust’s Ken Lassner shows advisors how to convert volatility into after-tax portfolio gains

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income