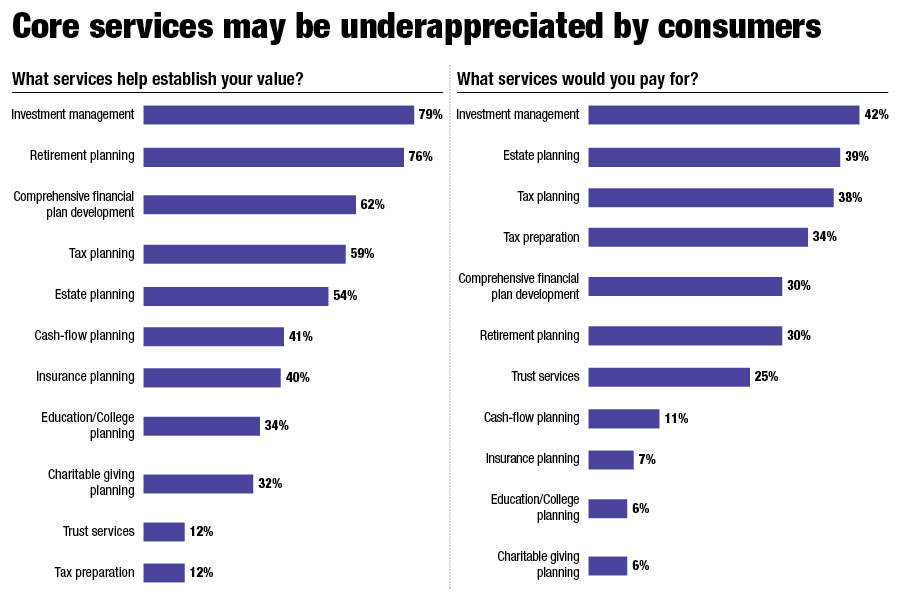

Advisors believe that investment management and retirement planning are the key services that establish their value to clients. That finding came through loud and clear in a new study by InvestmentNews Research for Protective Life on the value of professional financial advice.

This study, which included the views of advisors and clients, uncovered that the perspective of clients was somewhat different from that of advisors. While 79% of advisors believe that investment management helps them establish their value, just 42% of investors said they were willing to pay for successful investment management. Similarly, 76% of advisors believe that retirement planning is important in establishing value, while only 30% of investors would pay for it.

Those responses may reflect how investors currently pay for financial advice, and since most clients receive a bundle of services for the fees or commissions they are charged they likely ascribe their own value to each of those services. Clients may view all the services as important but might prioritize some over others if each were offered on an a la carte basis. Nevertheless, the survey results reveal some level of disconnect between what advisors and clients define as important services. This difference in perspective creates an opportunity for advisors.

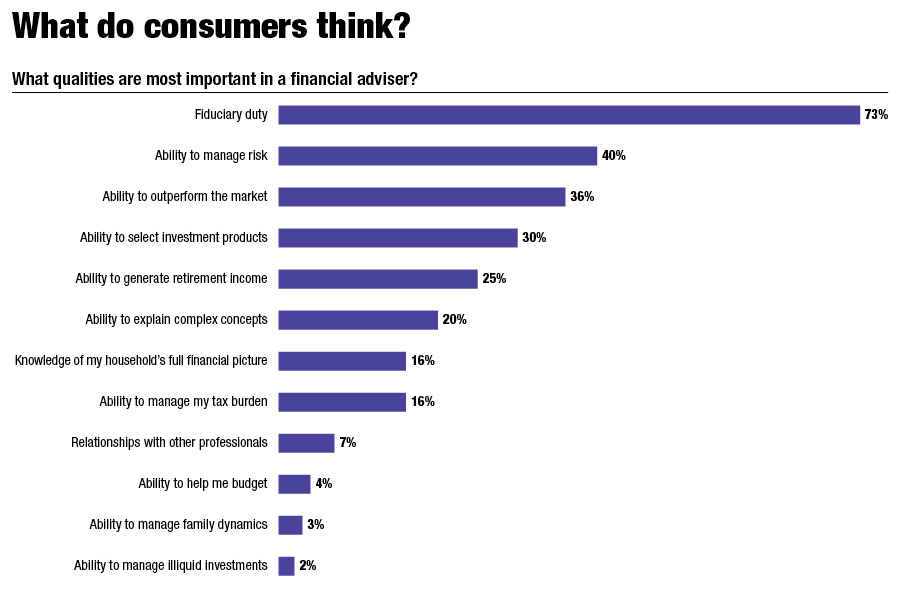

Consider that when clients were asked about the qualities they think are most important in an advisor, ranking first overwhelmingly was the advisor being a fiduciary followed by an ability to manage risk. While clients tend to think of risk largely as it relates to investments, advisors know that there are a multitude of risks clients face in retirement that clients often minimize or fail to consider.

Two major risks clients tend to underestimate or fail to consider are those involving longevity and sequence of returns. Data American Academy of Actuaries and Society of Actuaries, Actuaries Longevity Illustrator suggest that a 65-year-old male today, in average health, has a 35% chance of living to 90. A woman has an even greater chance — 46%. If the two live together, there is a 50-50 chance both will still be alive at 81, and that one will survive to 92. In fact, the fastest growing segment of the US population are those over the age of 85. Despite favorable odds, however, many clients simply cannot envision themselves as an octogenarian or someone approaching the century mark, and therefore fail to plan for this.

Clients also may not be aware that when they start withdrawing funds from their retirement accounts affects how long their money will last. Starting retirement during a market downturn, for example, can mean that drawdowns will likely deplete accounts much more quickly than if withdrawals were to begin when markets are rising. Reducing drawdowns lowers retirement income and can cause unplanned and unwelcome changes in spending and lifestyle — all of which clients would want to avoid.

Fortunately, since clients truly value an advisor’s ability to manage risk, they are likely to be receptive to advisor assistance in this area. Advisors can use these discussions as opportunities to introduce the many products available to manage risk. These products can give clients greater confidence in their retirement plans and also often can produce greater retirement income than might otherwise be available. They also may be able to provide other benefits. Products that offer guaranteed lifetime income may provide the solutions advisors and their clients are seeking.

By focusing on the risk-mitigating aspects of these products rather than on their investment value, as advisors can satisfy true client needs. For couples, guaranteed lifetime income products can provide assurance that neither spouse will ever run out of money and that they may be able to provide income for a designated period to those they designate, with most products. Perhaps even more important, clients can use these products to ensure their ability to maintain the lifestyle they want in retirement while keeping other assets invested in the market for possible future growth.

By framing guaranteed lifetime income products as a form of insurance that protects against many of the risks of retirement — risks that clients often don’t fully consider — advisors change the discussion from one about investment performance and fees to one about protection and security. At a time when clients are focused on risk and an advisor’s ability to manage it, discussions around protection and security would be well received.

Lauren Drapeau is National Sales Director of Annuity Advisory Solutions at Protective and a registered representative of Investment Distributors, Inc., a Registered Broker/Dealer, member FINRA and wholly owned subsidiary of Protective Life Corporation.

Protective® is a registered trademark of Protective Life Insurance Company. The Protective trademarks logos and service marks are property of Protective Life Insurance Company and are protected by copyright, trademark, and/or other proprietary rights and laws.

Protective refers to Protective Life Insurance Company (PLICO) and its affiliates, including Protective Life and Annuity Insurance Company (PLAIC). PLICO, founded in 1907, is located in Nashville, TN, and is licensed in all states excluding New York. PLAIC is located in Birmingham, AL, and is licensed in New York. Product availability and features may vary by state. Each company is solely responsible for the financial obligations accruing under the products it issues. Product guarantees are backed by the financial strength and claims paying ability of the issuing company. Securities offered by Investment Distributors, Inc. (IDI) the principal underwriter for registered products issued by PLICO and PLAIC, its affiliates. IDI is located in Birmingham, Alabama. Insurance and Annuities are: Not a Deposit | Not Insured by any Federal Government Agency | Have no Bank or Credit Union Guarantee | Not FDIC/NCUA Insured | May Lose Value

A $141M judgment and a federal asset freeze collide over one shrinking pool

The firm's CFO and EVP of Wealth Management Solutions are the latest executives to exit the broker-dealer.

Clients are saying they would consider switching advisors if another professional offered estate planning services, according to a new Trust & Will survey.

CEO Laurel Taylor says the fintech's composable AI stack helps workers optimize dollars across Trump Accounts, 529s, 401(k)s, and other employee benefits.

The bank has swiped three private banking veterans from BNY as the city climbs the ranks of America's fastest-growing wealth hubs.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.