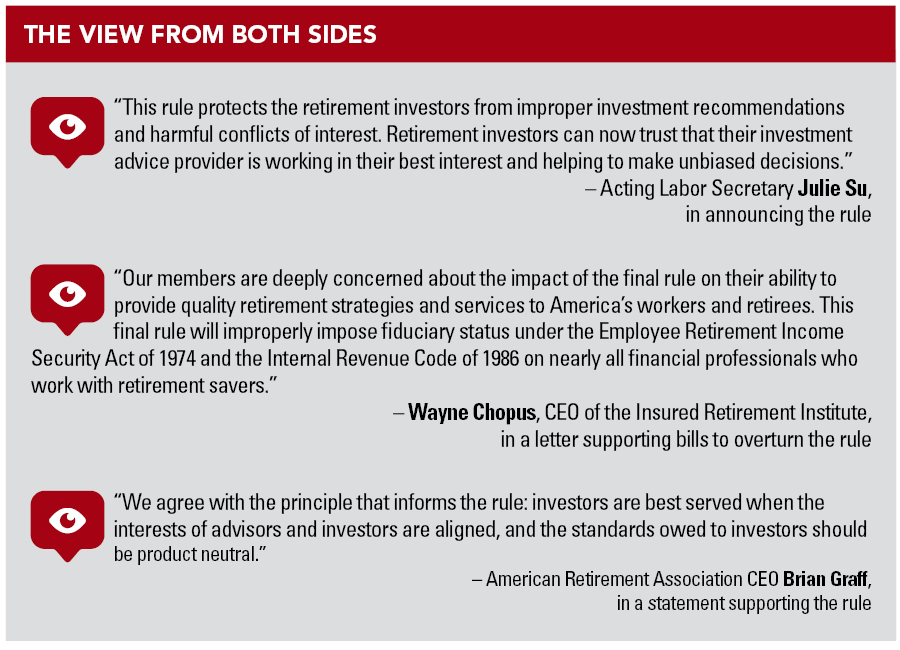

The DOL went to lengths to armor its new fiduciary rule against legal challenges, but recent attacks by Congress and the insurance industry add some uncertainty to its fate.

Last month, lawmakers filed a joint resolution invoking the Congressional Review Act, which is a mechanism for legislators to overturn federal agency regulations. That followed the first lawsuit filed against the Department of Labor over its Retirement Security Rule and amendments to several prohibited transaction exemptions. That case, brought by several insurance companies and an industry group, alleges that the DOL exceeded its regulatory authority.

“Uncertain is probably the best way to describe it,” Steven Rabitz, co-chair of the employee benefits and executive compensation practice at law firm Dechert LLP, regarding Congress’ attempt to overturn the rule and amended exemptions.

“Does the DOL have the authority to do what they would like to do, or is it really Congress’ purview? That’s where the main battle lines have been drawn.”

The agency has been working to redefine fiduciary advice since 2010, and several administrations have made iterations of the rule that, excluding the new one, have been overturned or replaced. Looking at the “fragility” of prior efforts in court, “an objective observer might wonder” whether Congress should be the entity responsible for defining fiduciary advice, Rabitz said.

“There is, to my mind, a path forward that might suggest that the DOL again exceeded its authority,” he said, adding that that is not necessarily his opinion.

It’s notable that the DOL addressed the extent of its authority to make the rule in the preamble to it, a nod to the lawsuit that ultimately killed the 2016 version that was passed in the Obama administration, Rabitz said.

A big departure from the prior standard is that one-time recommendations for rollovers from 401(k)s and other plans to IRAs can be considered fiduciary acts, and, much to the chagrin of the insurance industry, that includes annuity sales. The agency explained that financial professionals who present themselves as giving personalized, reliable recommendations will be considered fiduciaries and must provide “prudent, loyal, honest advice free from overcharges.”

Most provisions of the rule take effect September 23, though some will not be official until April 2025.

The DOL has long sought authority to regulate advice in the IRA market, though that was not part of the fiduciary rule change it considered in 2020, Rabitz noted.

“Effectively they missed one third of the [retirement] market, and now it has become a centerpiece,” he said.

“The big-ticket issue is that a lot has changed in the last 14 years, but there is a lot of the same. The question is effectively whether this is the DOL’s version of Death of a Salesman.”

“If you read the preamble to this 2024 version of the rule, the DOL goes to great lengths to try to explain (1) how they didn’t go beyond their authority, (2) how Congress did give them this authority over IRAs, and (3) how different this 2024 rule is from 2016,” said Bonnie Treichel, chief solutions officer at Endeavor Retirement, in an email. “That being said, Congress could still pass a joint resolution during a specified time period overturning the rule. That would still have to be signed by the president (not going to happen with Biden), but that could be overridden by Congress even still.”

As there is unlikely enough support among legislators to override a veto, the joint resolution is “likely just posturing and allowing or forcing members of Congress to take a position on it,” said Alex Smith, of counsel at Holland & Hart LLP.

Given how controversial the topic has been over nearly a decade and a half, it is likely that more lawsuits aiming to defeat the rule are in the works, he said. Where those cases are filed could make a difference, as courts can reach different conclusions, he noted.

And the results of this year’s presidential election will matter. The DOL, under former president Donald Trump, finalized a less burdensome rule for the industry than the Obama-era rule that was defeated in court.

“It doesn’t necessarily seem unreasonable, in that it’s one of the biggest financial decisions most people make,” Smith said of IRA rollover recommendations. “If someone’s going to a financial expert or someone who holds themselves out [as such] … they are probably expecting fiduciary advice.”

Although the 2016 fiduciary rule was reversed in appellate court, the Trump administration had backed off from defending it – the Justice Department, for example, did not opt to appeal the decision.

“The DOL was on a winning streak – it hadn’t lost any [court cases] until it lost in the Fifth Circuit three-judge appeals panel,” said Jason Roberts, CEO of the Pension Resource Institute.

“What I have never seen … is to just concede in the middle of an active suit,” he said, explaining that it is unclear if and how that would work. “I don’t think I’ve seen that in any agency proceeding.”

More likely is that, if Trump regains the White House, there would be a non-enforcement policy announced and the administration would start another long process to rewrite and replace the current rule, he said.

But another question around the court case is what effect a separate matter before the US Supreme Court could have. The high court is expected to soon rule on two cases challenging a federal regulation over fishing-boat operators. At the heart of those cases is what is known as the Chevron deference, a 40-year-old court decision that has a lot to do with the discretion civil servants have in interpreting their statutory authority.

If parts of that are walked back, for example, the lawsuit against the DOL could potentially be harder to defend, Roberts said. On May 21, the plaintiffs filed for an injunction.

“That’s an ultra-high bar,” he said. “We’re getting questions almost daily and having to remind firms that you’ve got to start putting the pieces in place to be compliant by September. Don’t activate those new policies in the event there may be some sort of delay … or some FAQs that come out and shed some light on areas that are less certain.”

“It’s time for an economic reset,” wrote the California governor, in a post on X.

Masterworks was launched in 2017 but its RIA, Masterworks Advisers, is just three years old.

One 2017 form, no broker license, and a $42 million gap they say surfaced on a webinar.

Fewer than half of Americans in their peak earning years feel on track for retirement, while many say limited financial knowledge and access to professional guidance are holding them back.

Meanwhile, Wells Fargo hauled advisors overseeing $825 million in the West Coast, while Wedbush has welcomed a seasoned professional from Stifel in California.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.