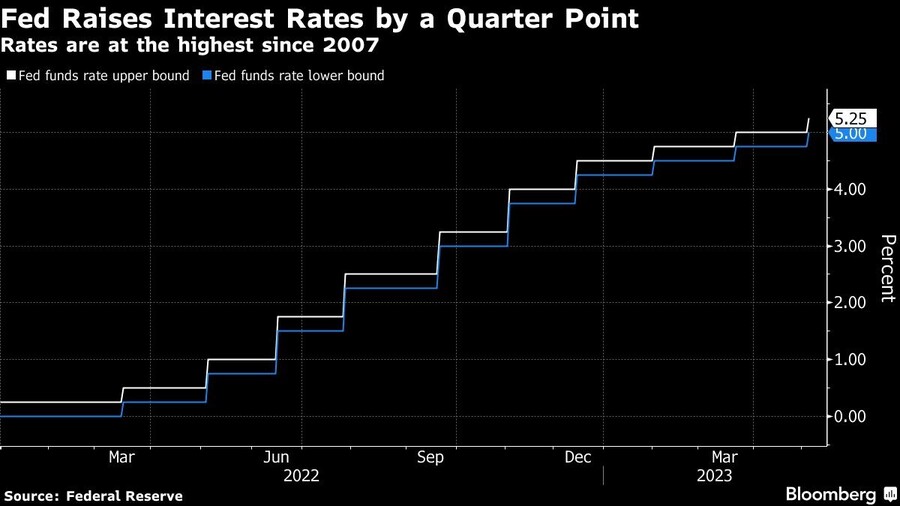

The Federal Reserve raised interest rates by a quarter percentage point and hinted it may be the final move in the most aggressive tightening campaign since the 1980s as economic risks mount.

“The committee will closely monitor incoming information and assess the implications for monetary policy,” the Federal Open Market Committee said in a statement Wednesday. It omitted a line from its previous statement in March that said the committee “anticipates that some additional policy firming may be appropriate.”

Instead, the FOMC will take into account various factors “in determining the extent to which additional policy firming may be appropriate.”

“That’s a meaningful change that we’re no longer saying that we anticipate” further increases, Chair Jerome Powell said at a press conference after the decision, when asked whether the statement is a signal that officials are prepared to pause rate increases in June. “So we’ll be driven by incoming data, meeting by meeting, and we’ll approach that question at the June meeting.”

The increase lifted the Fed’s benchmark federal funds rate to a target range of 5% to 5.25%, the highest level since 2007, up from nearly zero early last year. The vote was unanimous.

U.S. equities maintained gains, while Treasury yields and the dollar declined.

Policymakers are resolved to ensure inflation will continue decelerating — potentially with costs to employment — even as the banking system endures ongoing stress, lawmakers step up criticism and the latest data suggest emerging weakness in the labor market.

Powell said bank conditions had “broadly improved” since early March, but said the strains in the sector “appear to be resulting in even tighter credit conditions for households and businesses,” following a tightening in credit over the past year.

“In turn, these tighter credit conditions are likely to weigh on economic activity, hiring and inflation,” he said. “The extent of these effects remains uncertain.”

Rapid tightening over the last year aimed at curbing the highest inflation rates in decades also put pressure on financial institutions, leading to the largest bank failures since 2008.

In March, California’s Silicon Valley Bank and New York’s Signature Bank went under amid heavy deposit outflows, prompting the Fed to launch an emergency lending facility aimed at shoring up confidence in the banking system.

The emergency measures quelled market turmoil, allowing the Fed to continue its battle against inflation, but strains have resurfaced.

JPMorgan Chase & Co. agreed to acquire the troubled First Republic Bank in a government-brokered deal on Monday, and shares of other regional lenders plunged on Tuesday. That’s raising fresh questions about how long policymakers will be able to maintain interest rates at elevated levels.

In its statement Wednesday, the FOMC reiterated that “the US banking system is sound and resilient.”

Tuesday also saw the release of a monthly Labor Department report showing job openings fell and layoffs jumped in March, in a sign that the job market is finally beginning to feel the impact of monetary tightening.

Still, prospects of rising unemployment are ringing alarm bells in Washington as the 2024 presidential election campaign shifts into gear. A group of U.S. senators led by Elizabeth Warren and Bernie Sanders published a letter to Powell Monday, urging him to cease rate hikes.

While the Fed may be finished raising rates, Powell and his colleagues have pledged to keep them elevated for a time to make sure the central bank’s preferred measure of inflation — down from last year’s peak of 7% to 4.2% as of March — continues receding toward the 2% target.

Projections published after the March FOMC meeting showed officials were nearly unanimous in expecting it would be appropriate to maintain the federal funds rate above 5% through the end of 2023.

[More: Are Fed interest rates going up?]

Investors don’t see that happening. Prices of interest-rate futures have long signaled an expectation in markets that the Fed would pivot to rate cuts in coming months. Earlier on Wednesday they showed around 70 basis points of easing priced by the end of the year.

“It’s time for an economic reset,” wrote the California governor, in a post on X.

Masterworks was launched in 2017 but its RIA, Masterworks Advisers, is just three years old.

One 2017 form, no broker license, and a $42 million gap they say surfaced on a webinar.

Fewer than half of Americans in their peak earning years feel on track for retirement, while many say limited financial knowledge and access to professional guidance are holding them back.

Meanwhile, Wells Fargo hauled advisors overseeing $825 million in the West Coast, while Wedbush has welcomed a seasoned professional from Stifel in California.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.