The alleged $30 million fraud committed by Kenneth Starr and his Starr Investment Advisors LLP constitutes another black eye for the financial advice business. Indeed, the much-publicized scandal has investors once again wondering how high-profile advisers can get away with swindling their clients. (To read about the charges facing Mr. Starr,

click here.)

Questions are already being raised about whether the Securities and Exchange Commission dropped the ball again, after failing to spot the Ponzi scheme operated by Bernard Madoff and the alleged fraud perpetrated by Allen Stanford.

It appears the SEC had the celebrity adviser — who also operated a Finra-registered firm called Diamond Edge Capital partners until March 2010 — on its radar for a while.

According to his Finra BrokerCheck report, Mr. Starr had an open SEC investigation on his records. That investigation commenced on July 23, 2009, and was described as a "fact-finding inquiry" in which Mr. Starr was subpoenaed by the SEC to disclose documents relating to his RIA firm, Starr Investment Advisors. The Financial Industry Regulatory Authority Inc. released no further details because the investigation was not public.

An SEC spokesman declined to comment on that probe. But the commission's

complaint, filed in U.S. District Court in New York on Thursday, gives an indication of how Mr. Starr could have pulled off the alleged scam.

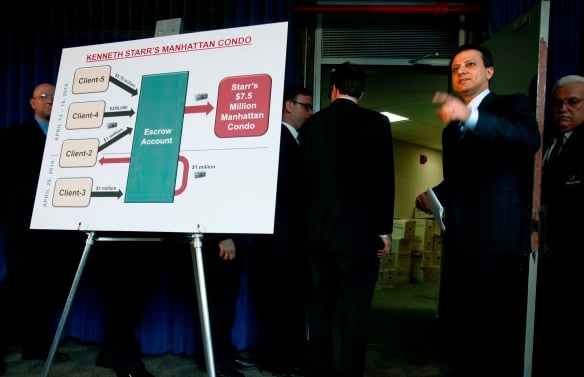

For starters, Mr. Starr and others at SIA apparently had power of attorney or signatory authority over a number of bank and investment accounts belonging to their clients. According to the SEC, that enabled him to transfer money from one client's account to another.

Starr Investment Advisors, like Mr. Madoff's firm, was also a “self-clearing” adviser — meaning the firm didn't use an independent third-party custodian to clear transactions.

What's more, the SEC claims the firm had failed to comply with custodial rules. According to the complaint, Mr. Starr's firm failed for three years, 2006-09, to engage an independent public accountant to perform a surprise examination of its advisory clients' assets over which the firm had custody.

In fact, some assets of SIA clients were allegedly held in the safe of one of Mr. Starr's other companies — Starr & Co. — even though none of the defendants named in the SEC complaint are qualified custodians, the commission noted.

U.S. Attorney Preet Bharara said at a news conference that investigators were searching Mr. Starr's office in New York and were working to freeze 23 bank accounts as they search for more victims. Press accounts have put Starr Investment Advisors assets under management at $700 million. But according to a revised ADV form filed on May 25 with the Securities and Exchange Commission, SIA has roughly $1.3 billion in client assets under management.

Federal prosecutors have estimated that Mr. Starr allegedly stole some $30 million from his clients, who included Uma Thurman, Sylvester Stallone, Caroline Kennedy and Candice Bergen.

One client in particular, Jacob “the Jeweler” Arabov, a New York jewelry store owner who was convicted in 2008 of falsifying records and making false statements in a federal investigation, is said to have been defrauded of more than $14 million by Mr. Starr — roughly half the money allegedly stolen from clients.

In the wake of more headlines that undermine investors' trust, registered investment advisers and financial planners must now deal with the fallout from the scandal.

One adviser, Jeffrey McClure, at The Personal Wealth Coach, an RIA in Salado, Tex., says he's going to be using the Starr case as a starting point for several conversations about the importance of a third-party custodian, one of Mr. Starr's most egregious “red flags.” “I'm going to be bringing it up,” Mr. McClure said. “I'm going to tell everyone and anyone I can about it. I always tell my clients very frankly that they should not trust me to have custody of their funds, and they should not trust anybody who's advising them to have custody of their funds.”

Scott P. Hilsen, a partner at Alston & Bird LLP, and a certified fraud examiner, said advisory firms can also trumpet the transparency of their operations.

“The more open a business is about their processes and controls, the less likely it is that they're hiding anything,” he said. "Good companies should advertise what they do to prevent fraud.”

But Mr. Bharara offered up what may be the most useful advice of all: "Anyone can be a victim of financial fraud, whether you are an ordinary citizen or a savvy businessman or a sophisticated celebrity," he said. "If a deal sounds too good to be true, it probably is."