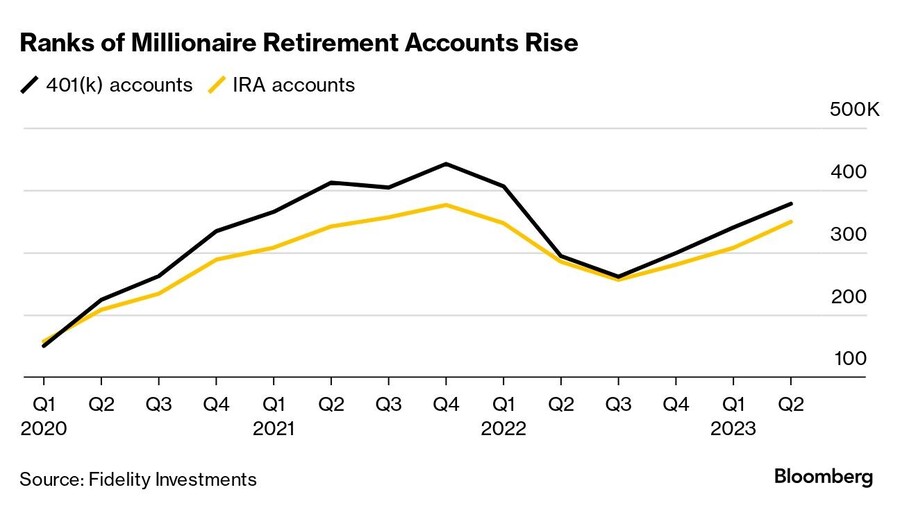

IRA and 401(k) millionaires are staging a comeback, with the number of seven-figure retirement accounts at Fidelity Investments inching back toward a 2021 high.

The tally of such accounts rose by more than 12% in the second quarter to 727,104, according to an analysis released by Fidelity Thursday. That’s the highest since the first three months of 2022 and within striking distance of a record.

This year’s double-digit gains in the benchmark S&P 500 have helped swell retirement balances for a third quarter in a row following a plunge that tracked the stock market last year.

“The average tenure of our millionaire 401(k) savers is 26 years, showing that staying in-plan and continuing to invest over the long term can pay huge dividends over time, particularly during positive turns in the market,” said Michael Shamrell, vice president of thought leadership at Fidelity Workplace Investing.

And while younger savers haven’t had decades in the market to amass large balances, Fidelity data show that many borrowers used the federal student loan payment pause to funnel money into retirement accounts. Close to three-quarters of student loan borrowers put at least 5% of their pretax salaries into 401(k)s during the period when payments were paused. That compares with 63% before the pause.

The average 401(k) balance at Fidelity is $112,400

The bank has swiped three private banking veterans from BNY as the city climbs the ranks of America's fastest-growing wealth hubs.

Employee accounts, crypto trials and job cuts frame a pivotal year for the Swiss lender.

New name draws on founder's family history as consolidation reshapes the broker-dealer landscape.

Deal brings tech-focused planning expertise, expanded Pacific Northwest presence to national RIA platform.

Five low-cost index ETFs to anchor Trump Accounts as advisors weigh options against 529 and UTMA plans for clients

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.