The biggest increase to Social Security checks since 1981 was good news for retirees. But it also served as a stark reminder that the program is expensive, with cuts to benefits looming unless it is retooled in coming years.

Alongside news of the benefit increase last week was a tax hike for many Americans, with the wages subject to the Social Security payroll tax set to rise almost 9% next year.

Even before the cost-of-living increase was announced, Social Security’s trust fund was set to run out of reserves by 2035 if no changes are made. Historically, reforms to Social Security don’t make many people happy. So, it’s worth asking: Does the program really need reform, and if it does, what changes are likely?

Social Security is a “pay as you go” system, with revenues collected today funding today’s benefits. Payroll taxes of 12.4% — with employees and employers each paying half that, and self-employed workers covering the full amount — finance about 90% of benefits.

Demographic trends mean that revenue stream is at risk, however, as the number of retirees grows faster than the number of workers paying taxes. In 2000, there were 3.4 workers for every Social Security beneficiary. The program’s actuaries project that will drop to 2.4 workers by 2030.

“That means we have to raise more from each worker or pay less to each beneficiary, or do a little of both,” said Richard Johnson, a retirement expert at the Urban Institute.

A much smaller slice of income comes from taxes paid on Social Security benefits, which were first introduced as part of a package of reforms in 1983. About 40% of beneficiaries pay taxes on part of their benefits, according to Social Security’s website.

The projected Social Security shortfall is equal to about 3.4% of taxable payrolls. If the payroll tax rate rose by 1.7 percentage points for employees and employers, that would enable everyone to get full benefits for the next 75 years, according to Alicia Munnell, director of the Center for Retirement Research at Boston College.

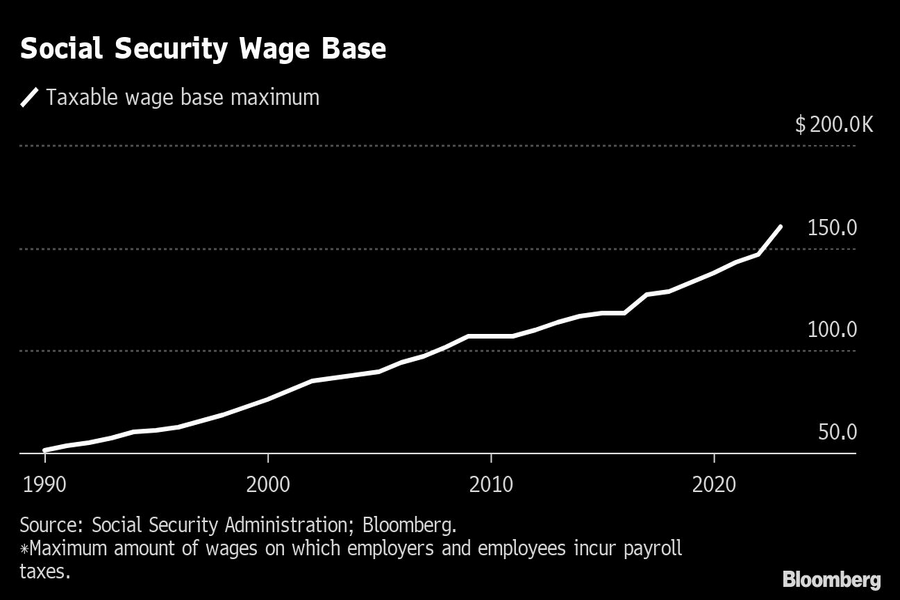

In 2023, the maximum amount of wages that incur Social Security’s payroll tax will rise to $160,200 from $147,000. A proposal from Rep. John Larson, D-Conn., who chairs the Social Security subcommittee on the House Ways and Means Committee, would have a payroll tax kick in again starting at earnings of $400,000, while also creating a minimum benefit set at 25% above the poverty line. (Currently, benefits are based on your 35 highest-earning years and there is no minimum.)

Increasing the taxable base would raise revenues, especially if those payments didn’t accrue additional benefits. But “if it became a really bad deal for higher-income people, I worry there would be less support for the program,” Johnson said. “What you get out has always depended on what you put in, and if policymakers break that link and Social Security is viewed as welfare, you might see support erode.”

The maximum amount of wages that incur Social Security’s payroll tax is tied to a national average wage index and adjusted annually. Next year’s 9% jump is based on the index for 2021, which got a boost as things returned to normal after the pandemic-related shutdowns of 2020.

One way to get more revenue into the system: Have the taxable wage base include employer contributions to employee health-care insurance, said Munnell. Social Security actuaries have estimated that would reduce the 75-year deficit (the period used to measure solvency) by about one-third. Under the proposal, both employer and employee premiums for employer-sponsored group health insurance would be subject to the tax, so both employees and employers would pay more.

“When Social Security was created, almost all of compensation came in wages, and now more of it is coming through benefits, so maybe it makes sense,” Johnson said.

The full retirement age is the age at which you get 100% of the benefits promised. For most people, it’s 66 or 67. The 1983 reforms raised the age from 65 to 67, but the changes didn’t take effect for 17 years “to give people time to adjust work and savings behavior to the reduction in benefits,” Johnson said. The 1983 changes to the full retirement age amounted to about a 12% reduction in benefits, he said.

There has been talk of raising the age to 69. That, however, would penalize workers with physical jobs that don’t allow them to work longer and who may have to claim Social Security early. Many people claim at the earliest age, 62, which means a 30% reduction in benefits compared with waiting to claim until full retirement age.

Instead of raising taxes, Andrew Biggs, a senior fellow at the American Enterprise Institute, favors reforms that gradually lower benefits for middle and high earners, while increasing them for lower earners.

“We’re a rich country and it’s not too much to ask that Social Security provide a true guarantee against poverty in old age, which it currently doesn’t because there is no minimum benefit,” Biggs said in an email. “At the same time, retirement savings outside of Social Security have risen dramatically across all groups, showing that middle and high earners can and will save more for retirement on their own.”

There’s not a lot of overlap between Democratic and Republican proposals for reforming Social Security, so Johnson expects a deal to come down to the wire. He thinks the most likely outcome is a rise in the taxable wage base and reduced benefits for the highest-income beneficiaries.

“Part of the problem, if you’re talking about fixing the program’s finances, is that no one is going to end up being better off,” Johnson said. “Either you cut benefits, or you cut taxes, and that’s not an accomplishment that you can run for reelection on.”

Clients are saying they would consider switching advisors if another professional offered estate planning services, according to a new Trust & Will survey.

CEO Laurel Taylor says the fintech's composable AI stack helps workers optimize dollars across Trump Accounts, 529s, 401(k)s, and other employee benefits.

The bank has swiped three private banking veterans from BNY as the city climbs the ranks of America's fastest-growing wealth hubs.

Employee accounts, crypto trials and job cuts frame a pivotal year for the Swiss lender.

New name draws on founder's family history as consolidation reshapes the broker-dealer landscape.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.