The Internal Revenue Service has raised tax brackets and the standard deduction by about 7% for 2023 as the soaring cost of food, energy and housing continues to batter Americans.

That’s the largest increase to the standard deduction since the tax system was first indexed to inflation in 1985, and will reduce the amount of income subject to taxes for most people.

The IRS adjusts the tax code annually to shield Americans from paying higher taxes as rising prices erode the value of the dollar. While changes have been fairly incremental in the last few years, decades-high inflation prompted an unusually big tweak for 2023, according to Tom O’Saben, government relations director for the National Association of Tax Professionals.

“The tax adjustments for 2023 are keeping up with the increase in everything we consume on a daily basis and are an accurate reflection of our economic reality,” he said.

As a result, employees can expect to see less tax withheld from paychecks as soon as January. Here are the key takeaways, according to experts.

The automatic adjustments to standard deductions and tax brackets will help a majority of U.S. workers whose wages have not kept up with ballooning inflation, allowing them to shield more of their earnings from income taxes.

However, the higher the income bracket, the higher the savings will be in dollar terms, said Annette Nellen, a tax attorney and professor at San Jose State University.

The standard deduction will rise to $13,850 for single filers, an increase of $900 from 2022, and to $27,700 for married couples filing jointly, an $1,800 boost.

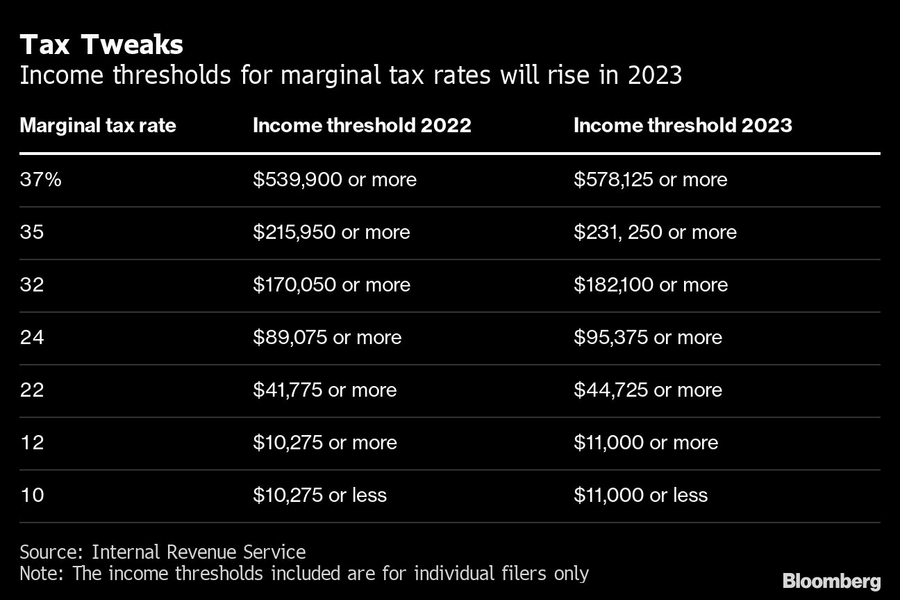

Meanwhile, all tax brackets will kick in at a higher income threshold in 2023. For example, the 24% tax rate will apply to income over $95,375 for single taxpayers and $190,750 for couples, up from $89,075 and $178,150 in 2022. That means a couple with $200,000 of taxable income would pay about $1,300 less next year due to the inflation adjustments, Nellen said.

The changes mean some taxpayers may be bumped down to a lower tax rate. And those who received pay raises may be protected from “bracket creep,” or paying more because they landed in a higher tax bracket, explained O’Saben.

However, Eric Bronnenkant, head of taxes for financial adviser Betterment, noted some tax items are not adjusted for inflation. That includes capital gains taxes and the additional Medicare tax, which applies to individuals making over $200,000 and married couples earning $250,000.

Filers who hope to pass on their wealth will be able to give more tax-free dollars in 2023. For an individual who dies in 2023, nearly $13 million of their estate will not be taxed, an increase from a little over $12 million this year. And for gift-givers, the first $17,000 will be tax-free, up $1,000 from 2022.

With “one of the largest one-year jumps we’ve seen in decades,” individuals can pass on an additional $860,000 to their family or trusts without incurring transfer taxes, said Belinda Herzig, senior wealth strategist at BNY Mellon. And the clock is ticking on the current estate-tax exemption, which is set to end in 2025, meaning filers need to “use it or lose it.”

With open enrollment season on the horizon, Betterment’s Bronnenkant recommends thinking about how to capitalize on employee benefits from healthcare to transportation. The IRS increased the amount employees can contribute tax-free to their healthcare flexible spending accounts to $3,050 from $2,850. Workers commuting back to the office can now spend up to $300 a month on qualified transportation and parking pretax.

The IRS has yet to announce any inflation adjustments for retirement plan accounts, but experts that to happen within a month. While retirees may get some relief from the 8.7% increase in Social Security benefits in 2023, O’Saben said these benefits were not meant to stand alone.

The IRS adjusts the dollar amount that taxpayers can contribute to their tax-deductible 401(k) and IRA accounts every year. When the IRS announces adjustments to retirement contributions, O’Saben and Bronnenkant advise maxing out contributions if possible.

“People should think about how these inflation adjustments could benefit your retirement savings — 401(k) contribution limits go up every year, so consider increasing your contributions and maximizing your IRA savings accounts,” Bronnenkant said.

Clients are saying they would consider switching advisors if another professional offered estate planning services, according to a new Trust & Will survey.

CEO Laurel Taylor says the fintech's composable AI stack helps workers optimize dollars across Trump Accounts, 529s, 401(k)s, and other employee benefits.

The bank has swiped three private banking veterans from BNY as the city climbs the ranks of America's fastest-growing wealth hubs.

Employee accounts, crypto trials and job cuts frame a pivotal year for the Swiss lender.

New name draws on founder's family history as consolidation reshapes the broker-dealer landscape.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.