Long-term services and supports (LTSS), which represents one of the biggest threats to retirement security, would likely be improved through the Well-Being Insurance for Seniors to be at Home (WISH) Act, according to a new report from Morningstar. In the report, released today, Morningstar applied its Model of U.S. Retirement Outcomes to simulate retirement adequacy for Gen Z, millennials, and Gen X households under current law and under the WISH Act. LTSS represents major retirement risk, with the present value of LTSS costs for baby boomers' projected costs exceeding $130,000 per household, and the mean for those with a simulated LTSS need exceeded $242,000.

The WISH Act, a bipartisan proposal in Congress, is designed to create a federal catastrophic insurance program for LTSS. The proposal contains language to mitigate LTSS risk by providing benefits after a one- to five-year waiting period, depending on income history, with lower-income people qualifying sooner. Benefits would be administered by the Social Security Administration, with payments estimated at about $4,000 per month in today’s dollars.

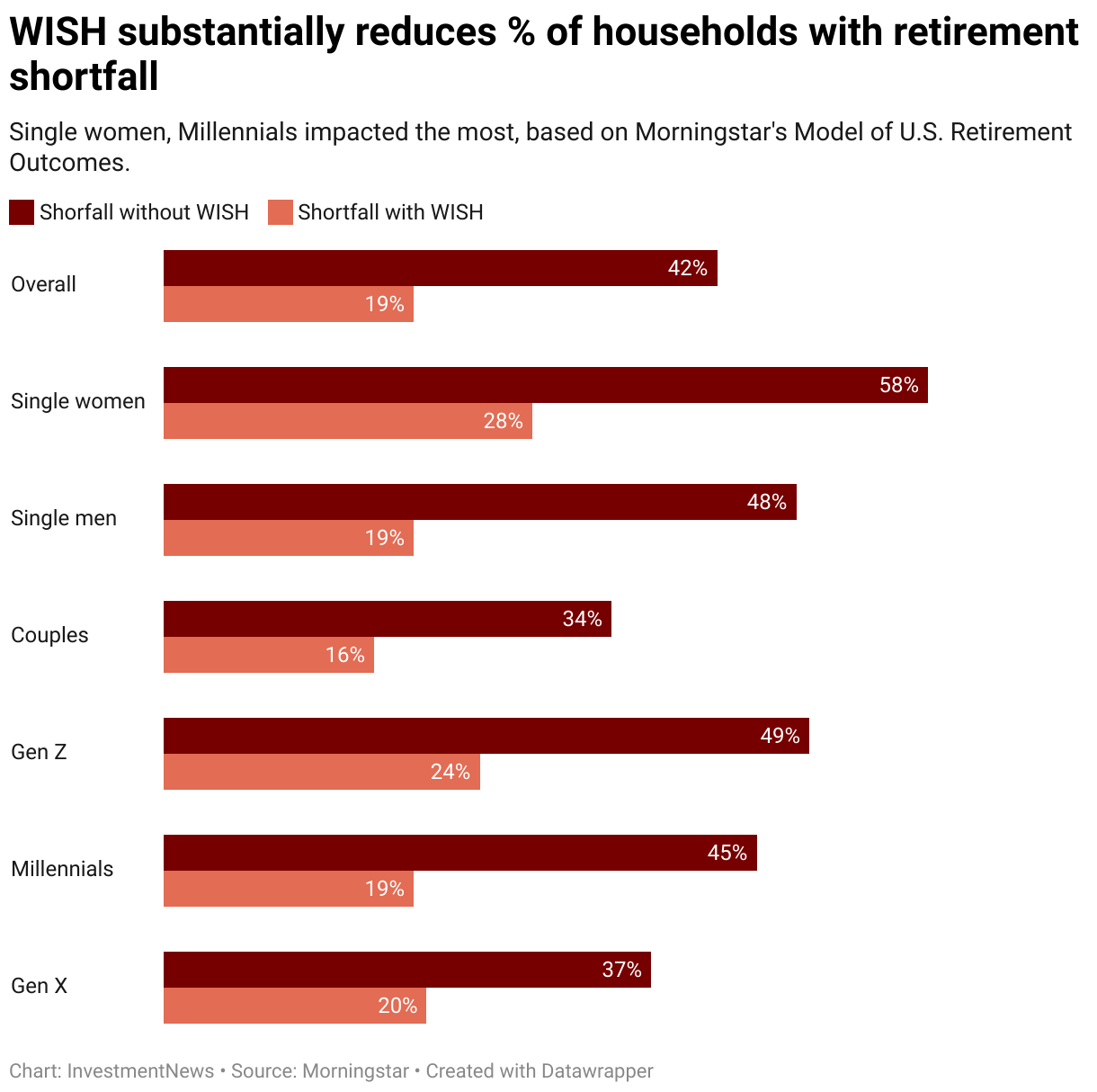

The Morningstar analysis finds the WISH Act dramatically improves retirement adequacy for households who qualify for benefits. Overall, the share of such households running short of money in retirement would fall from 42% to 19%. Single women’s shortfall rates would decline from 58% to 28%, single men’s from 48% to 19%, and couples’ from 34% to 16%. Generationally, Gen Z and millennials see the biggest reductions due to the compounding impact of LTSS inflation, with shortfalls halved. Gen X households also benefit, though to a slightly lesser degree. Middle-income households are most exposed to LTSS risk, as they have too much wealth to qualify quickly for Medicaid but not enough to absorb catastrophic costs.

Even when expanding the analysis to all households with paid LTSS needs, including those whose care needs fall short of the WISH Act’s waiting period, the program still meaningfully reduces retirement insecurity. Middle-income households gain the most from the WISH Act, as they face the greatest exposure to LTSS costs. Households with higher LTSS costs benefit significantly, while hispanic and black households see particularly large gains, helping narrow racial wealth gaps.

Morningstar notes the importance of indexing WISH benefits to LTSS costs. If benefits only grow at the rate of general inflation, the improvements shrink significantly — especially for younger households who are more exposed to long-term cost growth. It would reduce Medicaid reliance, strengthen retirement security across demographics, and potentially encourage private long-term care insurance markets.

Elsewhere, a Commonwealth team in Massachusetts converts to Cetera, while Janney draws four former Wells Fargo advisors to its Radnor, Pennsylvania office.

Clients say he copied the boss on his emails - and now they can't touch their cash.

He wired millions to his own accounts and told investors the fund was winning.

The partnership arrives as most small business owners near retirement age still don't have a formal succession plan in place.

A spokesperson for the estate planning fintech cited AI's reshaping of the industry as Trust & Will restructures its business.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.