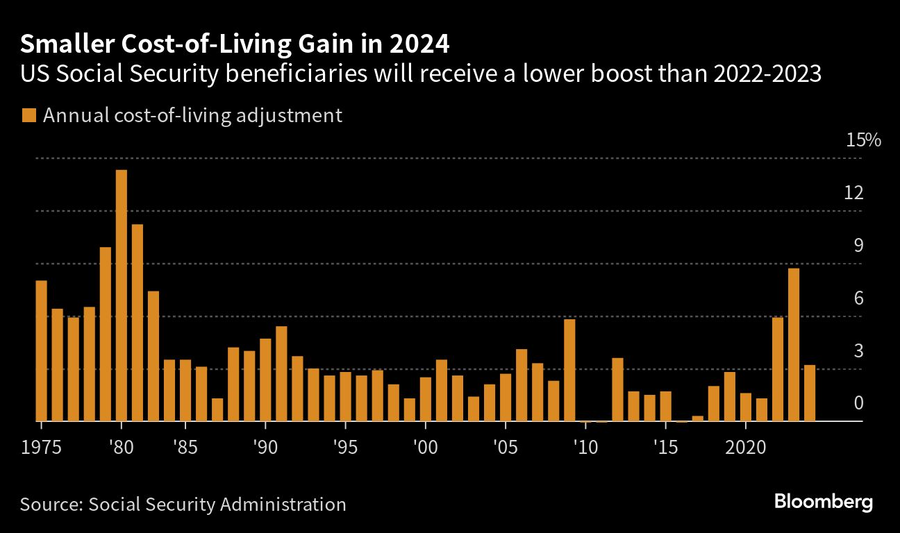

The Social Security cost-of-living adjustment will be 3.2% in 2024, down from the massive boost of 8.75% implemented this year.

The increase, which the Social Security Administration announced Thursday morning, is higher than the average of 2.6% seen over the past 20 years. But the decline in the COLA from 2023’s is a sign of cooling inflation.

The rise amounts to an average increase of $50 a month for the 66 million people who receive Social Security, as well as the 7.5 million who get Supplemental Security Income, the administration said.

“Social Security benefits are really only designed to replace about a third or less of our income, so when we have a COLA, even when it’s higher than average like 3.2%, the dollar amount of this increase is really pretty modest,” said Mary Johnson, Social Security and Medicare policy analyst at The Senior Citizens League. “Even though the inflation rate or the rate of price changes has come down, some prices don’t. Things like rent, your medical costs, they go up and they rarely come down.”

Social Security taxes are also affected by the change, with the maximum earnings that are taxable going from the current level of $160,200 to $168,600. That affects self-employed workers more, as they have to pay both the employee and employer portion of the tax, totaling 12.4%, Johnson noted.

“The 3.2% increase in the Social Security COLA for 2024 is a sign of normalcy and that inflation is getting under control. These are hopeful signs for everyone,” Larry Luxenberg, principal of Lexington Avenue Capital Management, said in an email. "This increase is only slightly above the Social Security Administration’s long-term projection. Prior increases for the last few years were unsustainable.”

The decrease in the size of the annual COLA follows a decrease in core inflation, but that doesn’t necessarily reflect the financial realities for people living on Social Security, Jim Sumpter, president of CMC Financial, said in an email.

“While it is nice that there will be an increase, it could be less than what clients are actually spending money on. Many items still cost much more than the overall increase which could be a net deficit to many seniors,” Sumpter said. “For example, out-of-pocket medical expenses seem to be a large bill for many seniors, and overall inflation on many of those costs is much greater than the 3.2% SSA increase. These clients could likely see a net deficit.”

A report earlier this year from The Senior Citizens League found that 68% of people on Social Security said that their household expenses have been 10% higher than a year prior, even as inflation has slowed. More than half of people surveyed said they were worried that Social Security payments would be insufficient in the future to cover their costs of living.

The forthcoming COLA is necessary to help Social Security participants keep up with the rising costs of essentials — but it also comes as more recipients are being taxed on their payments for the first time, according to data from The Senior Citizens League. That’s because the income threshold for taxation on Social Security hasn’t changed since those payments began being taxed — in 1984.

More than a quarter of recipients who have received Social Security for more than three years said that 2023 was the first time they’ve had to pay taxes on some of those benefits, reflecting the 2022 tax year, according to a survey by The Senior Citizens League. That figure will almost certainly go up next year, given the 8.7% increase for the 2023 tax year.

“The taxation thing is a thorn in everybody’s side. It affects about half of retired households today,” Johnson said. By comparison, an estimated 10% of people were affected by that tax when it was instituted in 1984, she said. Depending on someone’s sources of income, as much as 85% of Social Security benefits can be taxed, she noted.

Johnson said it’s crucial for recipients to check to see if their tax liabilities on Social Security benefits will be higher than usual.

Along with that, the recent COLA increases have had the adverse effect of pulling some recipients over the income line that determines whether they qualify for low-income assistance programs like the Supplemental Nutrition Assistance Program, or food stamps.

While 37% of low-income seniors received some type of assistance in 2022, following a COLA of 5.9%, that went down to 31% this year amid the 8.7% increase, according to survey data from the group. Additionally, while 46% of people in 2022 said their low-income benefits remained the same or higher, that dropped to 38% this year.

Bloomberg News contributed a chart to this story.

Teams head for W-2 independence models with practices totaling almost $1B.

Acquisition adds 400 defined benefit plans and 1.5 million participants, pushing Empower deeper into workplace benefits.

Menlo Park firm brings $900m in AUM and specialist expertise serving Apple and Google employees.

Acquisition of the Shufro-Glass Group pushes the national RIA's total client assets above $157 billion.

IRAs now hold nearly twice the assets of 401(k) plans — and most of that money didn't arrive through annual contributions.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.