$1 million hasn't been what it used to be for more than 20 years.

One million dollars in 1960 — around the time when having $1 million took hold in the popular imagination as a symbol of ultimate wealth — had the buying power of approximately $8 million dollars today.

Inflation has averaged 2.78% for the past 30 years. If we exclude the 10-year period from 1974 through 1984, when inflation averaged nearly 8%, the rate has been remarkably consistent since 1914, holding at around 2.75%. If we use that inflation rate as a rough guide, the equivalent of $1 million in 2014 will be $5 million in 2074 (in 60 years). If the place of the $1 million payday in today's lexicon is outdated — and it is — by then, it will be positively extinct.

The lesson here: when you are considering the investment returns you need, don't forget to factor in the power of inflation to eat away at your returns. You need 2.75% just to stay ahead of inflation.

Today's retirees are doubtless already aware of how far (or short, as the case may be) $1 million will stretch. Average life expectancy at age 65 in the U.S., according to the Centers for Disease Control and Prevention, is 85. Without making any daring assumptions about their portfolio, a couple with a $1 million nest egg can expect to draw $40,000 to $45,000 a year for the duration of a 20-year retirement. Financial advisers said the most important challenges to consider are how much money you've saved and how long you're going to live, according to an recent

InvestmentNews retirement income survey that polled 449 advisers.

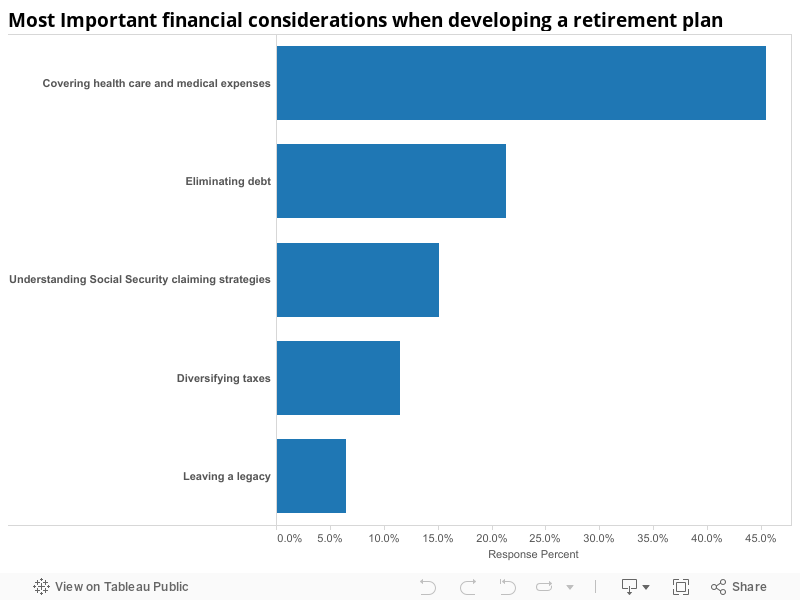

Housing costs also add up quickly and account for more than one-third of a retirees' expenses, according to a Census Bureau consumer expenditure survey. But the largest concern among advisers when developing a retirement plan is covering health care and medical expenses, according to the same

InvestmentNews survey. A couple who expects to pay 90% of their own health care costs out of pocket for the span of a 20-year retirement would need $261,000 for that run, according to the Employee Benefit Research Institute, which adds up to more than 25% of a $1 million nest egg.

See:

Health care will consume your Social Security payment within 10 years

The magnitude of that challenge is made even clearer when, according to a recent survey of investors by the Insured Retirement Institute, 33% of respondents said they expected to work beyond 65, and only 16% had at least $1 million saved. The U.S. has a record 9.63 million households with a net worth of $1 million or more, according to a recent report by the Spectrem Group. Even those millionaires would still be more than $7 million shy of joining the now-infamous “one percent” — which requires a net worth of more than $8.5 million.

If all of this hasn't sufficiently diminished what it means to be a millionaire, consider that by the time the average Generation X couple retires (2035), $1 million may not be enough to cover housing costs. By the time a Millennial couple retires (2055), $1 million will barely cover the cost of out-of-pocket health care expenses.