Three-and-a-half years after the Trump administration green-lighted the inclusion of private equity investments in 401(k) plans, new research suggests that the asset class might not be as good of a fit for that market as some would hope.

Currently, private equity is all but nonexistent in the defined-contribution plan world, which contrasts with its wider use in traditional defined-benefit pension plans, endowments, and other institutional investors.

The limits of 401(k)s have pretty much kept PE out of plans, although PE assets are barely threaded into some target-date funds and other asset allocation products. DC plan investment options have higher liquidity requirements, and they’re accessed by a less financially sophisticated base, making PE a hard argument for plan sponsors, which overwhelmingly are wary of straying from a standard array of mutual funds.

But PE has also been hailed as a potentially powerful addition to 401(k)s that could dampen volatility and goose returns.

The problem is that traditional pensions may not make the best case for that. A recent study by researchers at Morningstar found that the degree to which pensions use PE varies widely. And, perhaps more importantly, the use of PE doesn’t correlate with plans’ financial performance.

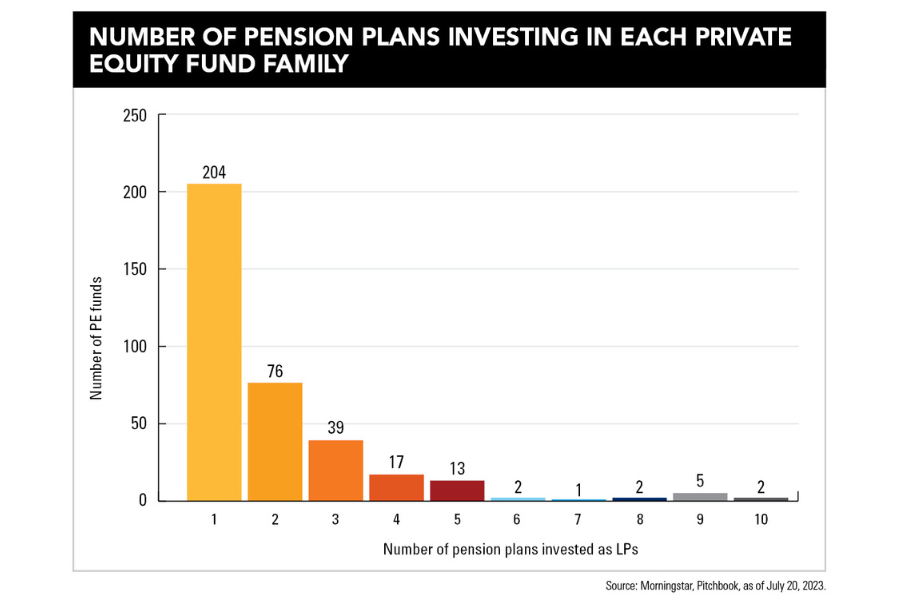

“We see variation of allocations to private equity. Some plans are allocating less than 1 percent, and some are allocating as much as 30 percent,” said one of the study’s authors, Lia Mitchell, senior analyst of government affairs at Morningstar. “That is definitely something that I didn’t anticipate finding.”

Further, large pension plans weren’t more likely to include PE than small ones. A potential explanation of the differences in allocations could be related to participant demographics and a plan’s duration of liability – the time frames it has for making payments to participants – but those were not factors in the study, Mitchell said.

“We weren’t able to find a conclusive answer,” she said.

The new research differs from a lot of academic papers that have examined PE in retirement accounts, as Morningstar “relies on real-world data and avoids unrealistic assumptions,” the authors wrote. “Instead of simulations, like those presented by academics, we examine the actual historical allocations made by pension plans to PE funds and the real returns generated by these PE funds.”

A paper last year from Georgetown University’s Center for Retirement Initiatives and CEM Benchmarking calculated that a 5 percent allocation in 401(k)s to PE and 5 percent to real estate could lead to better financial returns more than 80 percent of the time, with annual returns being on average 15 basis points higher.

The 401(k) market, being almost completely untapped, is enticing to PE firms. About a quarter of PE capital is owned by traditional pensions – and as those are becoming much less common, the trillions of dollars in DC plans represent a huge potential source of investors, the Morningstar authors wrote.

It’s notable that in early 2017, Blackstone CEO Stephen Schwarzman said on a call with analysts that getting PE and other alternatives into 401(k)s was a dream. Later that year, the company acquired retirement plan record-keeper Alight Solutions, which in 2021 went public through a special-purpose acquisition company.

That followed guidance from the DOL in 2020, in response to questions from PE firms, that the asset class could be included in 401(k) plans as a component of the default investments available to participants.

Even so, change is notoriously slow in the 401(k) business. Companies have faced costly litigation over their retirement plans for a wide range of reasons, including investment selection, performance, fees, and others. When plan fiduciaries change anything, they are usually quite careful.

As of the third quarter of 2023, all types of alternatives, not just PE, represented just 0.1 percent of DC plan assets, according to data from institutional plan consultant Callan.

“Private markets in general have not seen a meaningful uptick in DC plan offerings,” Greg Ungerman, defined contribution practice leader at the firm, said in a statement provided by the company.

The new research doesn’t necessarily mean that there isn’t a place for PE in 401(k)s, but it shows that more investigation is very much needed, Mitchell said. It would be helpful to have an index of PE funds to rely on, she said.

“This has been a topic the industry has been researching and discussing for several years, and that will continue to go on,” she said. “Without some sort of product that gets the full range of PE outcomes to one market-weighted average, it’s hard to know what range your individual fund could have.”

A Texas-based bank selects Raymond James for a $605 million program, while an OSJ with Osaic lures a storied institution in Ohio from LPL.

The Treasury Secretary's suggestion that Trump Savings Accounts could be used as a "backdoor" drew sharp criticisms from AARP and Democratic lawmakers.

Changes in legislation or additional laws historically have created opportunities for the alternative investment marketplace to expand.

Wealth managers highlight strategies for clients trying to retire before 65 without running out of money.

Shares of the online brokerage jumped as it reported a surge in trading, counting crypto transactions, though analysts remained largely unmoved.

Orion's Tom Wilson on delivering coordinated, high-touch service in a world where returns alone no longer set you apart.

Barely a decade old, registered index-linked annuities have quickly surged in popularity, thanks to their unique blend of protection and growth potential—an appealing option for investors looking to chart a steadier course through today's choppy market waters, says Myles Lambert, Brighthouse Financial.