This month’s edition, with contributions from special AdviserTech consulting guests Craig Iskowitz and Kyle Van Pelt, kicks off with the news that Orion Advisor Solutions has acquired Brinker Capital for $600 million to form a combined $40 billion TAMP, as Orion increasingly positions itself as a competitor to Envestnet, with a similar portfolio-management-turned-adviser-workstation solution that in turn is becoming a distribution channel for Orion’s model marketplace and platform TAMP offering. The deal was driven by private equity firm Genstar Capital, which similarly had previously acquired the AssetMark TAMP platform in 2013 for $413 million and sold it just three years later for $780 million, though notably in this case it appears to be less about simply growing Brinker as a TAMP and more about expanding Brinker’s reach throughthe adoption of Orion in broker-dealer channels. The only question is whether or how many broker-dealers are actually willing and interested in changing their portfolio management and adviser desktop solution.

From there, the latest highlights also feature a number of other interesting adviser technology announcements, including:

Read the analysis of these announcements in this month’s column, as well as a discussion of more trends in adviser technology, including Mastercard acquiring account aggregation and financial API provider Finicity after losing Plaid to Visa, Apex expanding its RIA custodial capabilities with a new, more out-of-the-box “Extend” platform, the quiet world of adviser software surveys suddenly becoming hotly debated as inconsistent sampling methodologies show wild swings in market share, and Wealthfront announcing a “New Mission” for the 2020s focused on banking as its future, effectively ending the robo-adviser movement as Betterment remains the “last robo standing” in what has turned out to be a niche solution for a subset of self-directed young investors rather than the “disrupt the adviser industry” movement robo-advisers once predicted they would be.

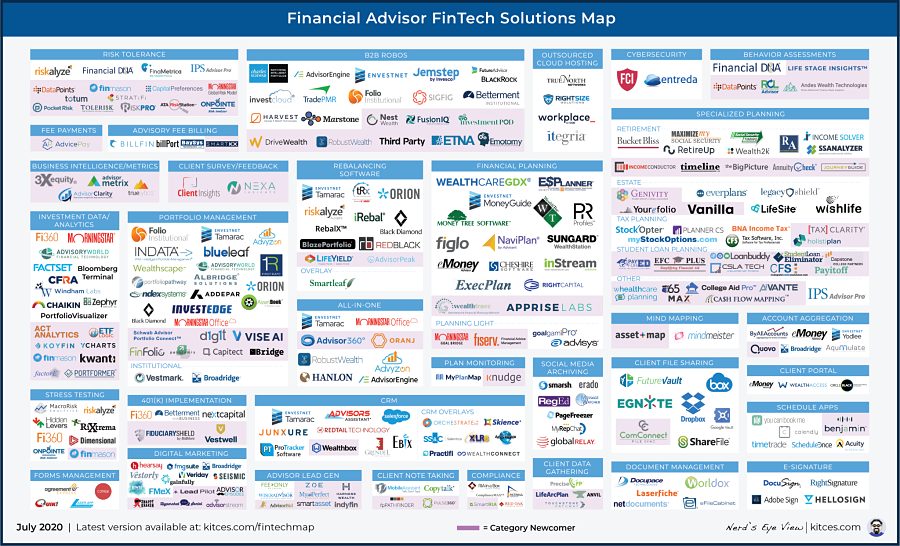

Be certain to read to the end, where we have provided an update to our popular new “Financial Advisor FinTech Solutions Map” as well!

I hope you’re continuing to find this column on financial adviser technology to be helpful! Please share your comments at the end and let me know what you think!

*And for #AdviserTech companies that want to submit their tech announcements for consideration in future issues, please send to [email protected]!

Orion acquires Brinker Capital for $600 million as it positions to compete against Envestnet as a broker-dealer TAMP? The blockbuster industry news headline this month was the announcement that Orion Advisor Solutions was acquiring $24.5 billion TAMP Brinker Capital for a whopping $600 million (a near-record TAMP valuation of almost $25 million of valuation per $1 billion of AUM!), which combined with Orion’s own nearly $15 billion Portfolio Solutions (formerly CLS Investments) platform will produce the industry’s fourth-largest TAMP (behind only AssetMark, SEI and big-dog Envestnet, which has $185 billion on its TAMP platform) with over 1,000 employees. Notably, the deal also marks the entry of private equity firm Genstar Capital, which was previously an investor in competing TAMP AssetMark, and is also a current investor in both hybrid broker-dealer Cetera and RIA aggregator Mercer Advisors, which reportedly was the one that fostered the Orion/Brinker merger proposal (helping to explain rumors earlier this year that both Orion and Brinker were “on the block”), and is now an equal co-owner alongside existing Orion PE investor TA Associates (though it remains unclear whether or how much capital TA Associates actually took off the table, and whether they’ll be looking to redeploy it elsewhere soon). The crux of the deal appears to be ramping up Orion’s TAMP capabilities, both to achieve greater economies of scale in an increasingly price-competitive business where scale is crucial, and with experienced Brinker CEO Noreen Beaman to head the newly merged Orion/Brinker TAMP offering (in which Orion Portfolio Solutions will be rebranded to Brinker Capital). The deal may be particularly appealing for Orion given its RIA-centric roots as a portfolio reporting solution in that channel and given Brinker’s greater depth in the broker-dealer channel (already the bulk of its 4,000 advisers on the platform) that is expected to produce rapid TAMP growth as brokers shift their value proposition to more financial planning advice and increasingly outsource portfolio implementation (which RIAs often scale their own in-house portfolio management offerings instead). Which means in practice, Orion is squarely positioning itself as a competitor to Envestnet and its platform TAMP offering -- a combination of portfolio management technology tools and an ever-growing marketplace of both in-house (PMC) and third-party (marketplace) TAMP solutions -- as Orion too combines together its CLS and Brinker offering into a $40 billion TAMP. Orion also announced this month an expansion of its model marketplace solutions through Orion Communities, all of which will be distributed through Orion’s portfolio management technology solutions (again akin to Envestnet). On the other hand, it’s notable that Envestnet itself wasn’t the buyer of Brinker -- especially after it acquired FolioDynamix a few years ago for $195 million to similarly expand its portfolio-management-plus-TAMP technology capabilities in the broker-dealer channel -- raising the question of whether new CEO Bill Crager simply doesn’t have the industry-legendary acquisition appetite of former CEO Jud Bergman (who tragically passed in a car accident last year), or if Envestnet already sees its own future as going beyondTAMP distribution with its recent efforts to expand into insurance and annuities (with its Insurance Exchange) and banking and lending (with its new Credit Exchange). At the least, though, the Orion/Brinker deal both cements the increasingly inextricable link between technology and TAMP/asset management solutions and the idea that technology doesn’t necessarily just facilitate asset management but can actually become an asset management distribution channel (it was, after all, Orion acquiring Brinker, and not the other way around) … and that the opportunity to distribute asset management through technology is sosignificant that it can help a sizable TAMP earn a significant strategic acquisition premium on its valuation in an otherwise increasingly commoditized TAMP business. In the end, the real key to the Orion/Brinker transaction will not simply be the ability of Brinker to distribute its asset management strategies further into the broker-dealer (or crossing over further into the RIA) channel, but whether Orion can gain market share over Envestnet’s ENV2 and Tamarac offerings to become the adviser dashboard and portfolio management platform through which Brinker can gain additional adoption.

Commonwealth’s Advisor360 spin-off prepares to ramp up with (insurance?) broker-dealer enterprises with new enterprise IT CEO. Over the past 20 years, the world of independent adviser technology has exploded, driven by the rise of the internet and APIs that can allow “any” software to connect with any other. The significance of the rapidly expanding ecosystem of independent software solutions is that in the past, only the largest firms with the greatest economies of scale could sufficiently reinvest in quality technology, while today stand-alone providers like eMoney and MoneyGuidePro have tens of thousands of users, far more than the largest wirehouse (or even all of them combined), and provide independent software platforms the widest base of advisers across which they can reinvest for the future. In fact, it’s the expanding reach and the opportunity to amortize development costs over a wider base of advisers that drove broker-dealer Commonwealth to spin off its previously proprietary adviser technology platform -- dubbed Advisor360 -- last year into a stand-alone offering and then begin to license it to other broker-dealers. The pivot turned heads at the time, as Commonwealth has consistently ranked at the top of user ratings for broker-dealer technology in the T3 Advisor Tech Survey, raising questions of whether Commonwealth was spinning off its ”secret sauce.” Yet shortly thereafter, the company announced a massive deal with MassMutual that instantly expanded the base of advisers using Commonwealth’s technology from 2,000 to 11,000-plus, demonstrating both the demand among the largest enterprise broker-dealers (and legacy insurance carriers) for a more cost-effective integrated technology platform, and Commonwealth’s opportunity to rapidly scale its offering into the new market. And now, consistent with this big-enterprise focus, Commonwealth’s now-stand-alone Advisor360 platform is announcing a new CEO to lead the business -- Richard Napolitano, a serial entrepreneur with several successful technology exits (to the likes of Adobe and HP), and a former president of sales for Sun Microsystems and president of EMC’s $4 billion software storage division. In other words, Commonwealth and Advisor360 chose not to hire a financial services industry or WealthTech executive, but someone with deep experience in large-enterprise software solutions, a signal both of Advisor360’s growth aspirations, and what appears to be a particular focus on the largest (insurance-based?) broker-dealer enterprises (rather than the increasingly popular independent RIA channel). In addition, it’s notable that while more and more technology for broker-dealers is built to facilitate asset management distribution -- from Envestnet to the recent Orion/Brinker deal -- Advisor360 is simply positioning itself as an enterprise software solution for large enterprises, giving it an increasingly unique positioning in an otherwise crowded marketplace competing for the enterprise adviser’s dashboard (and perhaps especially appealing to insurance broker-dealers that are more likely to offer their own proprietary insurance and investment solutions anyway?). It remains to be seen whether Advisor360 can string together more big deals on the size and scale of MassMutual, given the immensely complex sales cycle and transition effort it details. But given the hire of Napolitano -- and his experience in large-scale enterprise sales and deployments -- Advisor360 is clearly betting that it can. Time will tell.

Tegra118 acquires RetireUp’s financial planning and insurance optimization tools for a second bite at the planning software apple. Insurance broker-dealers have struggled for years with bifurcated user experiences between implementing investment and insurance products with clients (not to mention illustrating the products and associated needs analysis). Advisers complain that they have to navigate two completely different account opening processes, while once the products are implemented, clients wonder why their portals don’t display both their insurance and investments in one holistic view. Envestnet has a 12-month head start building out this functionality after snapping up for $500 million PIEtech’s MoneyGuide, which has robust insurance planning functionality that we expect to be combined with their Insurance Exchange launched last year to connect carriers directly to advisers (allowing insurance implementation to occur directly from the financial planning software experience). Now, however, just four months after private equity firm Motive Partners finalized its purchase of 60% of Fiserv’s investment services unit and relaunched it as a stand-alone company -- Tegra118 -- the company has announced its own first acquisition, of retirement planning software RetireUp, to move into the unified insurance-and-investment world. Motive paid a premium, shelling out $510 million for its share of the business, yet it has quickly opened its wallet to show that it understands the new entity will need additional firepower to remain competitive. The RetireUp deal comes exactly 10 years after Tegra118’s previous acquisition of a financial planning software vendor AdviceAmerica, which brought it robust planning tools and a decent proposal generation system, but suffered from a lack of investment from Fiserv corporate and eventually fell behind the competition as its user interface grew stale. However, Tegra118 was successful at integrating AdviceAmerica into its enterprise managed accounts platform, making it one of the few on the market that could deliver a centralized model management infrastructure that a broker-dealer home office could use to automatically deliver internal models to its advisers and maintain consistent investment strategies at scale (in essence, allowing broker-dealers to offer their own robo model solutions to their advisers). Their platform’s scalability has long been at the core of Tegra118’s value proposition, and drove its success in both the broker-dealer space (10 of the top 12) and asset management (10 largest firms), The one segment that Tegra118 has not been able to break into is insurance broker-dealers. A four-way battle has developed to provide wealth systems to insurance firms between pure technology players like Tegra118, enterprise TAMP vendors like Envestnet (Advisor Group), broker-dealer developed platforms like LPL Financial’s ClientWorks (which also powers Equitable’s wealth infrastructure) and Advisor360 (which is licensed by MassMutual and recently spun off from Commonwealth Financial) and RIA custodians like Pershing and Fidelity (used by Lincoln Financial). This is where RetireUp could be key, since it has a unique digital account opening capability for insurance solutions that is integrated with dozens of insurance carriers and can prefill the myriad of forms and electronically deliver them to the correct providers. RetireUp, which is based in Libertyville, Illinois, closed a deal to become part of LPL Financial’s Vendor Affinity Program last October, and it has spent the past few years bolstering its product offerings with its own acquisition of RepPro, a smart forms and digital business execution platform and has steadily built out its line of annuity products from a range of providers. If Tegra118 can combine RetireUp’s insurance onboarding workflow with its existing managed accounts process, it could deliver a unified experience that insurance broker-dealers would be very excited to see. But the company will have to contend with increasing pressure from numerous directions, including integrating RetireUp’s tools into its enterprise architecture, marketing its new brand and identity, and growing its revenue quickly enough to show promise for Motive, while competitors like Envestnet and Advisor360 also hire and ramp up their competitive offerings. Which raises the question: Will Tegra118 be able to convince the top insurance broker-dealers to even consider a new holistic insurance-and-investment enterprise offering, especially as everyone operates in a post-COVID environment where enterprise firms might delay large-scale conversions?

Does Merrill Lynch’s new client engagement workstation show a wirehouse advantage for the next generation of adviser workstations? Back in the 1980s and 1990s, technology was difficult and expensive to produce and required great economies of scale … such that the leading technology solutions were found at the largest adviser platforms (e.g., wirehouses), while the independent adviser community struggled with a lack of any technology at all beyond a series of homegrown solutions that the early independent firms built for themselves and then sold to their peers. However, the growth of the internet, and the rise of application programming interfaces, or APIs, turned this dynamic upside down. Independent software providers could connect together a growing ecosystem of other independent solutions for a rapidly growing independent channel and achieve economies of scale … to the point that today, independent financial planning software platforms like MoneyGuidePro and eMoney Advisor each have almost as many financial adviser users as all the wirehouses combined, and even some of the leading “proprietary” software platforms like Commonwealth have been compelled to spin off their (Advisor360) software into an independent solution to amortize its future development costs across a wider base of advisers than just its own. However, the growth of the independent software ecosystem has not been without its challenges, in particular around the lack of consistent data standards and an exponentially growing number of API connections that need to be made to connect “everything” with everything else … such that while anything can be connected to almost anything else, in practice most independent technology is not actually very deeply integrated with more than a select few preferred providers or key hubs. Which raises the question of whether the opportunity for superior adviser technology may now shift back to the wirehouses, whose everything-under-one-roof unity of data, combined with what is still a sizable base of 15,000-plus advisers (at least for Merrill Lynch and Morgan Stanley), makes it possible to actually build the all-in-one adviser workstation that independents struggle to cobble together. A good case-in-point example is the recent launch of Merrill Lynch’s new Client Engagement Workstation, which combines on-platform account servicing and trading tools, unified client information, and client action items and workflows, along with external market data about client portfolios, into a single dashboard, and then analyzes all the data to provide Next-Best-Action-style “insights” to spot new opportunities for client engagement (from products and solutions that Merrill offers, to planning opportunities like charitable giving strategies). In other words, while in theory independent adviser technology can make the adviser workstation of the future by weaving together an entire ecosystem of solutions, in practice, it’s hard to get everyone to play well together in the sandbox, while wirehouses that own and control all the data and development of their entire sandbox are suddenly emerging as leaders able to actually build and deliver the next generation of the adviser workstation.

Envestnet launches “Opportunities to Engage” recommendation engine to provide next best action for independent advisers. When robo-advisers first arrived on the scene in the early 2010s, their vision was to take all the advice that human financial advisers provide, reduce it to an algorithmic recommendations engine and deliver those recommendations directly to consumers at a fraction of the cost (by eschewing the human financial adviser altogether). Yet the caveat is that in practice, the robo-adviser approach effectively assumed that all financial problems can be boiled down to “problems of information” -- where if consumers are just provided with the right information, they’ll immediately take the right and correct action. In reality, just as releasing a website that says “eat less, exercise more” doesn’t solve the world’s obesity problem, providing information on the hazards of lung cancer hasn’t eliminated smoking and having a never-ending stream of workout videos on YouTube hasn’t put personal trainers out of business, most people’s financial difficulties aren’t problems of information alone. Instead, while information is necessary (it’s hard to lose weight if you don’t know how body mechanics work, and it’s difficult to save and invest if you don’t understand how markets work), the information alone isn’t sufficient, and there’s still no substitute for the power of another human to help us think differently about what’s possible, and then hold us accountable to help us make the changes we need to make. Accordingly, the real opportunity of robo technology tools is not to automate human beings out of advice… but instead to augment human beings, both to give better advice and to help spot the opportunities to provide advice in the first place (which can be heavily automated in a world of account aggregation!). Accordingly, Morgan Stanley made waves two years ago when it launched its “Next Best Action” solution, in which the wirehouse’s technology would monitor its immense amount of continuously flowing client data and then nudge its advisers to focus on the “next best action” for a particular client, from spotting idle cash to be invested, an overconcentrated position to be trimmed, an investment that needs to be rebalanced or some other financial planning opportunity. Now Envestnet has announced its own version of Next Best Action for the independent advisers on its own platform, dubbed “Opportunities to Engage,” which similarly will monitor data about the adviser’s firm and clients to spot opportunities where clients may be engaged around planning opportunities. The significance of “Opportunities To Engage” for Envestnet, though, isn’t merely the value to the advisers themselves to have software that more proactively spots planning opportunities with clients, but the ability to leverage its Yodlee acquisition as Envestnet pivots to become a “platform of platforms,” from its existing Exchange of third-party managers to its new Insurance and Annuity Exchange and its coming Credit Exchange, providing an ever-widening list of product solutions that advisers can recommend to their clients. In other words, in the future, Envestnet might not only provide nudges to advisers about planning opportunities for clients, but outright show how the client’s underperforming investment manager might be replaced by another on the Envestnet platform with better performance in a similar strategy, how a client’s insurance policy might be replaced by one from the Envestnet Insurance Exchange with lower premiums or how a client’s mortgage could be refinanced today at a lower rate through Envestnet’s credit exchange … where Envestnet becomes the platform shelf (compensated by the product manufacturers for distribution), Opportunities To Engage is the engine that spots deals for clients, and advisers deliver those value-add opportunities to clients for implementation (and earn their fees with the value or cost savings the client receives in the end).

After years of limited success with front-end partnerships, Apex builds its own to extend into the RIA custody business. Apex Clearing has been trying to establish a beachhead in the world of wealth management for years. While it has been very successful with digitally native startups getting off the ground -- Apex was the back end for the early stage launches of Betterment, Wealthfront and Robinhood -- it has struggled with those digital startups leaving (Betterment, Wealthfront and Robinhood all left and built their own back ends) at the very point that they started to reach a size and scale that would have been very interesting wealth management opportunity for Apex. At the same time, Apex has struggled to gain traction in the independent RIA wealth management channel, initially trying to gain distribution through partnerships with so-called “B2B robo-advisers” that offered a front-end adviser and client experience to pair with Apex’s back-end custody and clearing APIs (e.g., InvestCloud, Harvest Savings & Wealth [nee Trizic], AdvisorEngine and Envestnet/FolioDynamix), as these digital wealth platforms just haven’t picked up steam either (largely because advisers don’t seem to want to pay for an independent front-end workstation platform and instead simply expect their RIA custodians to provide such tools as part of their own interface). So enter Apex Extend: Apex has built its own front-end adviser interface to share directly to (enterprise) financial advisory firms and institutions. While Apex has always offered a modern, API-driven custody solution, the APIs were a bit complex to build to, and in practice seem to have deterred larger organizations from building these solutions directly with Apex. After all, digital advice solutions have at least historically been associated with small accounts, which means when considering those solutions, enterprises are extremely cost-conscious. After plugging in Apex custody fees and a digital advice provider’s fees, the math didn’t work out to be profitable enough for the expected effort. Apex aims to solve that with Extend, providing a more out-of-the-box solution that (enterprise) financial services firms can white-label. Now a large fund manager -- or even a sizable RIA or hybrid broker-dealer -- can go to market with a digital advice offering built entirely on Apex technology, but still leveraging their brand. In addition, it wouldn’t be surprising to see a few press releases come out in the near future in which Apex partners with nonfinancial institutions to launch digital wealth products using Extend (e.g., robo-advisers attached to other types of tech companies that have significant reach but would need a purely out-of-the-box robo solution, echoing the calls years ago of whether a player like Amazon or even Snapchat might someday enter the robo-adviser space). From the adviser perspective, though, the real question is whether Apex Extend can position Apex more competitively in the traditional RIA custodial business, which is seeing record numbers of advisers at least exploring new options after Morgan Stanley acquired ETrade and Schwab announced the acquisition of TD Ameritrade, particularly for midsize to large RIAs (or larger hybrid broker-dealers?) that have some tech savvy and want an RIA custodian that will be more flexible in integrating directly to their own proprietary tech stack.

Financial planning delivered through employer channels heats up as Origin raises $12 million and Brightside raises $35 million. As with any product or service, consumers will only pay for financial planning advice when they perceive enough value in that advice to be worth the cost. In the world of individual financial planning, this has led to a growing focus on figuring out how best to explain the value of financial planning and justify its cost, and what advisers need to do to deliver more value to their particular target clientele. But “provide enough value in financial advice to justify the cost of that advice” isn’t the onlybusiness model to validate the cost of financial advice. Instead, because financial problems have real world costs, from relationships (financial problems are the leading cause of relationship stress and divorce) to health (a physical manifestation of money-induced stress) to productivity (as financial problems distract employees in the workplace), solving one of those indirect costs of financial distress can also generate a return on investment” that makes it worthwhile to pay for financial planning. In fact, one recent study estimated that in the aggregate, almost 50% of the U.S. workforce is experiencing financial stress, leading to nearly $500 billion in lost productivity for employers, and other research has found that financial stress can be costing employers from $1,900 per employee to as much as $4,000 per employee in lost productivity as a result of both financial distractions during the workday and outright employee absenteeism. Which means, in turn, that there’s an economic opportunity in the workplace to deliver financial advice to employees, simply to enhance the business’s worker productivity (not to mention the actual value of the advice to the end employees themselves). Accordingly, in the past month, several new startups have raised significant venture and Series A rounds seeking to work with employers to deliver financial planning in the workplace as an employee benefit validated by the employer productivity benefits, including Origin (which makes financial planning advice available to employees for a flat $6/month/employee in a “prepaid legal” model), and also Brightside (which not only provides advice, but is seeking to make more direct financial wellness enhancements, such as creating a system to route money directly from employees’ paychecks to their otherwise unsecured loans in exchange for negotiating a lower interest rate on the latter because it’s now “secured” by the employee’s paycheck). In fact, Brightside has even attracted the attention of the vaunted venture capital firm a16z, which led its recent $35 million Series A round (and signals the VC view that financial planning is now deemed to be a Big Business opportunity in the workplace channel). Notably, though, the recent initiatives from Origin and Brightside appear to be substantively different than others like Edelman Financial Engines or the recent Empower Personal Capital, in that they’re not necessarily about adding human financial advice overlaying a plan participant’s 401(k) balance, but a more holistic (and likely more household-cash-flow-based) style of personal financial advice (recognizing that for most Gen X and Gen Y workers today, their primary financial challenges are not tied to their investment accounts and their balance sheet, but their cash flow and household spending). Still, though, to the extent that comprehensive financial planners historically have focused primarily on the top 10% of households or so, employer workplace financial planning has a real opportunity to expand financial advice to groups that in the past have had limited access to professional advisers, while simultaneously being able to justify its value with a different kind of (employee, not end-client) value justification that could make it more economical to service such clients in the first place.

Empower retirement mimics Financial Engines by acquiring Personal Capital for $1 billion to bring human advice to 401(k) plans. Record keeping and other qualified retirement plan services have been under intense competitive pressure over the past decade from a combination of new technology pressuring outdated back-office systems and a growing spate of 401(k) fiduciary lawsuits that have put record-keeper pricing and cost structures under a microscope, leading to a giant wave of consolidation as even the biggest players try to get bigger and achieve better economies of scale. Thus was the journey of Empower Retirement itself, born of a 2014 merger of the record-keeping services of Great West Financial, JPMorgan Chase, and Putnam Investments. It is now the second-largest retirement services provider with $656 billion of assets under administration for 9.7 million workers across nearly 40,000 workplace retirement plans. The challenge is that while more size with better economies of scale, plus better technology to improve efficiencies, may over time help record keepers stay competitive, it nonetheless remains a brutally challenging environment, with fee compression pressure as far as the eye can see. Which helps to explain why in late June, Empower Retirement announced the acquisition of Personal Capital, an independent RIA with $12 billion of AUM that was often dubbed a robo-adviser’ but in practice was a human-based advisory firm that had simply built its own proprietary technology to serve clients efficiently. The distinction that Personal Capital was nota robo-adviser is important, because in practice it didn’t charge robo-adviser fees, either, and in fact was able to grow to $12 billion of AUM charging “human adviser” fees that started at 0.89% (or more than 3X the going rate for robo-advisers) for a more holistic advice offering. In other words, Personal Capital proved out that there is at least a subset of consumers that will pay for human advice far above what technology alone can provide. That’s a lesson for robo-advisers that Empower seems to hope to implement in the 401(k) channel to similarly expand its own revenue and margins with a (human) advice offering for a subset of its plan participants. In fact, in the end, Personal Capital’s greatest success arguably was not merely its ability to deliver human advice leveraged with technology -- which virtually any and every human-based RIA does today with a wide range of AdviserTech solutions -- but instead its ability to distribute its personal financial management tools to consumers for free and turn them intoclients. In practice, Personal Capital’s primary marketing channel for its 22,000-plus clients and $12 billion of AUM was the 2.5 million people (with $771 billion of assets being tracked) that used its free software, an effective conversion rate of about 1% of users and 1.5% of tracked assets. In the context of Empower’s existing user base, that means the potential for Personal Capital to be deployed as financial wellness technology that upsells Empower’s defined-contribution plan participants at similar conversion rates could produce another $10 billion-plus of AUM for Empower (or even more when considering the potential to bring in outside non-Empower assets), and may help to justify the otherwise eye-popping valuation of $1 billion on just $12 billion of AUM (which would amount to approximately 10X revenue, drastically higher than the 2X revenue valuation typically applied to the RIA model). Furthermore, the ability to offer an in-plan 401(k) human advice offering also reduces the risk that plan assets roll out when those plan participants retire -- or at least, if they do roll over, it’s simply to an IRA still managed by their same Empower-Personal Capital human financial adviser. In other words, the Empower/Personal Capital is similar to the Edelman Financial Engines deal back in 2018 in that it involves retirement plan providers rolling out a human advice offering to plan participants, both as a way to sell a higher-value, higher-priced and higher-margin advice service to an increasingly commoditized retirement record-keeping business and also to retain (and prevent the roll-out) of retirement plan assets at retirement. As a result, the Empower/Personal Capital deal isn’t just notable in the context of the competitive environment among 401(k) plans (with others like Fidelity similarly rolling out more and more advice services to their 401(k) plan participants) -- the growing trend could also signal a growing risk to independent advisers that the 30-year bonanza of building businesses through 401(k) rollovers may soon be coming to an end, as the previously unadvised 401(k) plan participant in the future may already have a multiyear existing relationship with a human financial adviser who can provide retirement advice to retain their business long before they ever hit the radar screen as a prospect for an independent adviser in the first place.

Mastercard acquires Finicity after losing Plaid to Visa as account aggregation shifts from wealth management to big banking. The blockbuster fintech news back in February was Visa’s acquisition of Plaid for a cool $5.3 billion with an eye to turning the company’s account aggregation and financial APIs away from just reporting on a household’s financial situation and into actual triggers for financial transactions (e.g., using account aggregation comparisons to identify opportunities to actually open a new bank account or credit card with better rates, and processing the account opening itself). For Visa, the acquisition arguably marks a turning point both for account aggregation fintech, and for Visa itself to pivot into a new world of “open banking” with financial-API-driven client acquisition. For Mastercard, though, the Plaid deal can be simply summed up as “the one that got away.” Accordingly -- and with all due respect to Finicity and the remarkable business that it built -- it appears that after Mastercard lost the bidding war for Plaid, and could not be stuck holding the bag forever, it scooped up Finicity (which competes with Plaid in the world of account aggregation and financial APIs) for a billion dollars to keep pace with Visa. Yet notably, the sky-high valuations (the word on the street is that Mastercard paid 50x sales for Finicity, just as Visa did for Plaid) of these account aggregation and financial API deals come from the broader applications to financial services. To some extent, there’s simply the value of the data itself -- harvesting the data from Finicity is valuable, and so is the ability to get even deeper competitive insight into Visa volume through Finicity’s lens. And while $1 billion is an eye-popping number, it is a fraction of Mastercard’s quarterly EBITDA, for which in return the company gets a ton of upside, moving from just being a clear leader in the payment processing space to Finicity’s allowing Mastercard to participate in the upside of other markets, such as: banking and Investing (only about 5% penetrated by companies like Finicity and Plaid, but a $650 million total addressable market serving clients like Robinhood, Betterment, Coinbase and Acorns); lending (a $1 billion market that is only about 2% penetrated serving clients like LendingClub, EarnIn, Quicken and Navient); the next wave of payments (companies like Venmo, Square, Stripe and Transferwise have only penetrated about 3% of this space); personal financial management (Mastercard now has the opportunity to participate in the penetration beyond 4% of a $350 million market with companies like Credit Karma and Clarity Money); and the $200 million business services market (competing with the likes of Intuit, Gusto and other payroll services). And of course, the international market opportunities abound as well. From the perspective of financial advisers -- who are traditionally more focused on asset management and investment accounts -- the reality is that the banking and money movement revolution (embodied by the Mastercard/Finicity deal) may soon begin to spill over into the advisory space as well. For instance, the deal is also a nod toward the rise of companies like AdvicePay and RightPay from Right Capital that are bringing automation to the process of billing advice fees that must come from bank accounts or credit cards instead of investment accounts; both representing bets on a future that more and more advice will be delivered via a transaction that can be done via a bank account or a credit card (and it’s pretty hard to process a payment today that doesn’t touch Mastercard or Visa’s credit card products). And it may also bode well for the potential of being able to move money more quickly from one account to another (e.g., clients who want to open an investment account and might soon be able to transfer the cash from their existing bank account immediately and easily from their smartphone, akin to apps like Venmo that may enable a new wave of robo-adviser automation tools for advisers).

Original robo-adviser Wealthfront completes pivot away from robo-advice with new banking-based mission. When robo-advisers first arrived on the scene in the early 2010s, the mantra was that “human advisers are expensive and charge ‘an arm and a leg,’” while technology can design and implement the same portfolio for a fraction of the cost … assuming that consumers would then virally flock to their lower-cost alternative. In practice, as robo-advisers quickly discovered, human financial advisers already use technology, largely to automate portfolio implementation and rebalancing (we call it rebalancing software and have had it since 2005), and the bulk of what financial advisers are paid is actually to find and getthose clients in the first place, since asking consumers to transfer their life savings to manage is not an “if you build it they will come” solution. In other words, the real reason financial advisers struggle to charge lower fees or serve a wider range of clientele isn’t the cost to create and implement portfolios for clients, but the client acquisition cost to market and get those clients in the first place (an average of $3,119 per client according to the latest Kitces Research study). Robo-advisers had brought an operational efficiency knife to a client acquisition gunfight. The end result was that in the years that followed, most robo-advisers were wound down, sold or pivoted away to B2B channels, with only the originals -- Betterment and Wealthfront -- remaining in the race. Even among those players, Wealthfront’s growth has slowed in recent years, crossing $10 billion and then $11 billion of AUM in 2018, but climbing to only $13.5 billion today (nearly 2 years later), with the rest of its growth to more than $20 billion of total assets on the platform coming from a new banking offering with high-yield cash (that separately pulled in nearly $10 billion-plus for Wealthfront in 2019 alone). Accordingly, last year Wealthfront began to pivot away from investment management as its primary product focus and toward a new initiative dubbed “Self-Driving Money,” in which its technology will help consumers automate the process of directing their money to wherever it would be best suited (e.g., automating the process of saving, managing bill paying and spotting expenses to trim, etc.), and acquired the technology and financial planning team from Grove to accelerate the transition. And now, Wealthfront has “officially” announced its new mission to disrupt banking -- no longer financial advice -- through its Self-Driving Money solution to make it easier for consumer to manage alltheir finances. From the perspective of the robo-adviser trend, Wealthfront’s pivot arguably marks the end of an era; the only remaining pure robo-adviser play from a decade ago is Betterment, which finally has reached cash flow break-even and is growing but arguably only as a niche solution (the one player left standing) and not a mainstream disruption. And ironically, perhaps Wealthfront’s greatest investment management legacy as a robo-adviser will be the one it never fully capitalized on -- not democratizing investment management through technology, but democratizing direct indexing, which until Wealthfront was limited to only a subset of ultra-HNW solutions like Parametric’s Custom Core, but now is becoming an increasingly mainstream solution viewed as the next big thing to disrupt mutual funds and ETFs (even though Wealthfront showed it was possible but didn’t succeed in distributing the solution disruptively). Still, though, to the extent that financial advisers themselves are arguably overly focused on the “balance sheet” (e.g., household assets, and investible assets in particular) while the average person is more likely to need advice about cash flow and household expenditures, Wealthfront’s pivot is even more on target to the opportunity of truly expanding financial advice and guidance to underserved consumers (or at least, automating away the unnecessary and unproductive choices through Self-Driving Money!). And most financial advisers themselves would likely agree that the traditional banking industry is sorely in need of some disruption as well. In the meantime, though, may the robo-adviser movement rest in peace.

Will the real adviser survey on software market share please stand up? The world of financial advisers is incredibly fractured, with 50,000 advisers among the four major wirehouses, then nearly 150,000 more scattered among 3,800-plus broker-dealers (from independents to regionals to insurance broker-dealer subsidiaries), not to mention more than 30,000 SEC- and state-registered investment advisers, and countless more advisers working for insurance companies. The end result is that not only is it remarkably difficult just to count how many financial advisers there actually are (especially in a world of multilicensed insurance agents with broker-dealer affiliates who are also dually registered as investment advisers), but it’s even harder to understand the trends of adviser technology adoption when there are so many different advisers across so many different channels (ranging from mega enterprises to solo entrepreneurs). Over the years, a number of adviser tech software surveys have emerged, the longest standing of which is the Financial Planning magazine annual Tech Survey. However, as a result of what appears to be a declining focus on putting resources toward the survey, this year Financial Planning’s survey reached a problematically low nadir of just 225 advisers (down from 350 in 2019 and over 3,000 a decade ago), and in turn was split across so many channels that the entire survey included only 29 stand-alone independent RIAs and nine wirehouse advisers, while (over-)sampling nearly 50 advisers at banks and credit unions; in fact, fewer than 125 of the advisers had any affiliation to a traditional wirehouse, broker-dealer or RIA (the rest in banks, insurance companies and 15% in an ambiguous “Other” category). That raises serious questions about whether the survey is representative of much of anything, and it was called out by adviser tech guru Joel Bruckenstein for bizarre results like an indication that MoneyGuidePro’s market share crashed from 65% to 7% in the past year (the year that Envestnet bought it for half a billion dollars, which, if actually true, would be a multi-hundred-million-dollar write-down for Envestnet!). In fact, Bruckenstein several years ago created his own T3 Advisor Technology Survey after breaking away from the Financial Planning survey. Yet while the T3 survey draws from a far wider sample -- literally thousands in the latest 2020 survey -- it too still struggles with inconsistent sampling through the historical use of an open survey link that software companies themselves help to distribute (which increases the sample size, but also effectively turns the representation of market share into a “turn out the vote” exercise for the tech vendors, which in turn has occasionally led to wild swings in T3’s market share data, such as when Redtail’s market share leaped from 19% in 2018 to 57% in 2019). In turn, other providers in recent years have begun to develop their own surveys, from RIA In A Box’s survey of its 1,600-plus advisers (a healthy sampling, but almost exclusively of small to midsize RIAs that themselves are only a fraction of the total adviser landscape), to the InvestmentNews Adviser Tech Survey (which in 2019 surveyed just 272 advisory firms). Arguably when it comes to adviser software ratings -- i.e., do advisers like their software -- T3’s multi-thousand adviser response rate at least gives a solid base of feedback about what software advisers like the most. Still, though, with various adviser software surveys showing swings of 10% to 20% in market share (and sometimes more) from year to year or from one software survey to the next -- almost all of which is a result of their own dissimilar or internally inconsistent sampling methodologies -- it remains remarkably difficult to answer the simple question: Which adviser technology tools are actually growing, or shrinking, their market share?

Will the CFP Board’s new fiduciary standards for adviser technology kill black box insurance product illustrations? If there’s one thing that computers are good at, it’s crunching numbers; while the industry continues to debate whether or how much financial advice will be delivered in the future by robots versus humans, the calculationsthat underlie such advice have long since transitioned to the digital realm, with more and more financial advisers relying on third-party financial planning software or at least leveraging Excel for their financial planning projections, and relatively few still pulling out their trusty HP-12C calculators. Similarly, when it comes to evaluating financial products -- particularly the complex ones like life insurance -- product illustrations have long been the domain of software that produces the illustrations and models their underlying moving parts. Of course, the caveat is that even when software does the number-crunching work, the financial adviser is still expected to know and understand what the software has produced in the course of using that output to make a recommendation. And in its latest update to the Standards of Conduct and Code of Ethics, the CFP Board is now requiring CFP professionals to fully understand their technology as one of the 15 Key Duties of being a CFP Fiduciary, including that the CFP professional “must exercise reasonable care and judgment when selecting, using, or recommending any software, digital advice tool, or other technology while providing Professional Services to a Client,” “must have a reasonable basis for believing that the technology produces reliable, objective, and appropriate outcomes,” and most importantly, “must have a reasonable level of understanding of the assumptions and outcomes of the technology employed.” In other words, it will no longer be permissible for CFP professionals to simply accept “black box” software output without some evaluation of its reliability and objectivity, and without understanding the assumptions being used and how the output is produced. Notably, this doesn’t necessarily mean that advisers must independently deconstruct and recalculate software output, though it may someday stoke the creation of a third-party provider that can put its stamp on technology vendors for their “reliable, objective, and appropriate outcomes” to give advisers their requisite “reasonable basis” beyond just taking the vendor’s word. And it does create more of a challenge when it comes to the software used for product illustrations, particularly in areas like permanent life insurance that do have a series of complex and often not fully disclosed underlying assumptions that, arguably, CFP professionals cannot assess just by taking the illustration output and presenting it to a client (especially since an illustration by the company trying to sell the product doesn’t necessarily meet the objectivity requirement, either!). In fact, in recent years even regulators themselves have acknowledged that life insurance illustrations are so inconsistent that they shouldn’t be used for comparison purposes in the first place, arguably making it even more difficult for CFP professionals to rely on such software output with clients under the CFP Board’s new standards (especially if the details of the underlying assumptions aren’t fully disclosed). All of which ultimately raises the question: Will the CFP Board’s new technology standards force changes to life insurance product illustrations, and more generally to any financial planning software or other projection tool that doesn’t fully and completely disclose its underlying assumptions and calculation engine for advisers to evaluate for themselves?

In the meantime, we’ve updated the latest version of our Financial Advisor FinTech Solutions Map with several new companies, including highlights of the “Category Newcomers” in each area to highlight new FinTech innovation!

So what do you think? Can Orion take on Envestnet or is its technology-plus-TAMP solution already too deeply seated in the broker-dealer community? Will Empower be able to leverage Personal Capital to capture 401(k) rollovers long before retirement, while plan participants are still employees? Will Origin and Brightside be able to scale financial planning as an employee wellness benefit? Can Apex gain market share among independent RIAs with a new, more out-of-the-box custodial solution? Could the new CFP Board Advisor Tech standards create newfound pressure on financial planning software, and especially insurance product illustrations, to be more transparent about their assumptions and calculations?

Disclosure: Michael Kitces is a co-founder of AdvicePay, which is mentioned in this article.

Special thanks to Kyle Van Pelt, who wrote the sections on Mastercard/Finicity and on Apex, and to Craig Iskowitz, who wrote the Tegra118/RetireUp section. You can connect with Kyle via LinkedIn (or follow him on Twitter at @KyleVanPelt), and with Craig on LinkedIn (or on Twitter at @craigiskowitz).

Roundhill, Bitwise and GraniteShares funds remain on hold while the agency weighs how novel ETFs should be regulated.

"Shares of alternative assets managers have lagged this year as investors grow wary of private-credit exposure."

The fintech platform is touting a new AI-free Planning Observations feature, which draws on IRS tax records to uncover opportunities for advisors.

The Omaha, Nebraska-based RIA's latest acquisition expands its Rocky Mountain footprint after two prior Colorado deals last year.

Operational drag between an advisor signing and accounts going live is emerging as a competitive liability for wealth management firms.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.