Please see our new site: Fintech for Advisers - It showcases cutting-edge fintech trends for technology-driven advisers. The focus on fintech helps advisers stay up-to-date on current technologies in wealth management that can help drive future growth.

Welcome to the March 2020 issue of the Latest News in Financial Advisor #FinTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors and wealth management.

This month's edition kicks off with the results of the latest T3 Advisor Software Survey, which continues to show that a subset of dominant players hold the largest market share in each key category… but that at the same time, upstarts in virtually every major advisor software category from Advyzon to RightCapital to Wealthbox to YCharts are gaining market share, and that some of the biggest shifts in advisor interest are coming from the “miscellaneous” listing of new advisor software categories that are still being created!

From there, the latest highlights also include a number of other interesting advisor technology announcements, including:

Read the analysis about these announcements in this month's column, and a discussion of more trends in advisor technology, including the shift towards “re-bundling” of the advisor tech stack into various platform combinations, the rising trend of ‘second-act’ FinTech entrepreneurs coming back to launch new companies to disrupt the ones they originally built and sold, the emergence of Regulation Best Interest compliance and training tools as the June 30th effective date looms, and the latest list of the Best (Advisor) FinTech companies to work for!

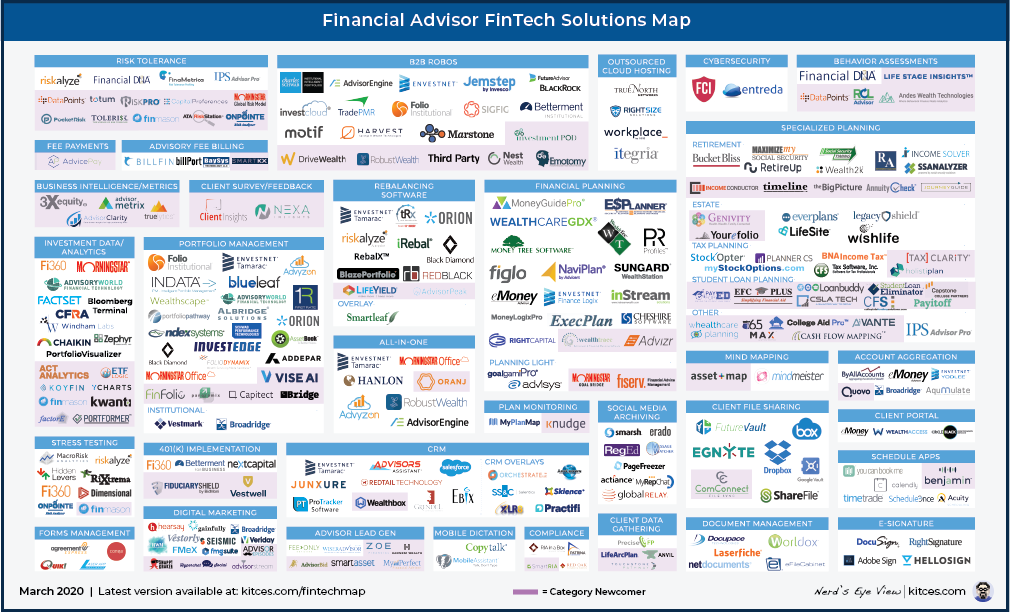

And be certain to read to the end, where we have provided an update to our popular new “Financial Advisor FinTech Solutions Map” as well.

I hope you're continuing to find this column on financial advisor technology to be helpful! Please share your comments at the end and let me know what you think.

*And for #AdvisorTech companies who want to submit their tech announcements for consideration in future issues, please submit to [email protected]!

T3 Releases Annual AdvisorTech Software Survey Of Adoption And User Ratings. The domain of financial advisors is extremely fractured, with Cerulli estimating nearly 300,000 financial advisors industry-wide, and even the largest mega-players (e.g., LPL for independents, wirehouses Morgan Stanley and Merrill Lynch, RIA custodians like Schwab) struggling to gain more than 5% market share at a time. From the advisor technology perspective, when even mega-enterprises have no more than single-digit market share and the majority of advisors are ‘independent’ (either as RIAs, or under flexible independent broker relationships with an independent broker-dealer), it becomes especially difficult to understand industry trends in advisor software adoption, when the base of users is so scattered and technology platforms may be popular or even dominant in one channel but virtually non-existent in others (which means even slight variations in sampling methodology can result in drastically distorted perceptions of market share). Nonetheless, the most popular industry survey in the marketplace today to understand advisor tech trends is the T3 Advisor Software Survey, historically produced by industry tech guru Joel Bruckenstein (and now conducted jointly with industry commentator Bob Veres’ Inside Information as well), which captures key data points on both what advisors are using (market share), what they enjoy using (i.e., User Ratings), and what advisors are looking to potentially adopt next. Notable data in the latest 2020 survey results includes: Morningstar and Envestnet remain the dominant players in the ‘All-In-One’ category (through their broker-dealer distribution reach), though independent Advyzon and Commonwealth’s Advisor360 are making positive strides; Redtail remains dominant in the advisor CRM channel, followed by Wealthbox, Salesforce, and Junxure; MoneyGuidePro and eMoney remain the big players in financial planning software, but RightCapital is taking a clear claim on 3rd; Morningstar Office and Albridge remain the top players in portfolio performance reporting, but Orion is closing the gap, Tamarac (with its PortfolioCenter acquisition) is even larger, and Black Diamond maintains a strong user base (with one of the highest User Ratings); Riskalyze still dominates the risk tolerance category, and despite the hubbub of competitors, no recent upstart challenger to Riskalyze has gained even 1% market share (to Riskalyze’s 30%+); Morningstar’s Advisor Workstation maintains a hold on investment research, but competitors Fi360, YCharts, and Kwanti are all gaining ground (along with AdvisoryWorld since its LPL acquisition); Calendly is the most popular amongst calendaring apps for advisors; and the most popular amongst the ‘miscellaneous’ category that advisors are considering include CopyTalk and Mobile Assistant for client note taking, AdvicePay for financial planning fee processing, and Everplans and Whealthcare for elder care and estate planning for clients, and MaxMyInterest for client cash management; and the “most valuable technology” for advisors was ranked as CRM 1st, financial planning software 2nd, and portfolio management tools a distant third (raising questions of whether the latter, as traditionally the most expensive software of the advisor tech stack, may soon face advisor pricing pressure?).

The

Artificial Intelligence Rules-Based Expert Systems Are Coming: FP Alpha

And IDT Launch At T3. As a knowledge-based profession, there has

been a growing buzz in recent years about whether someday the exponential

growth of “artificial intelligence” would replace the human intelligence of

financial advisors in working with clients. Thus far, though, advisor software

solutions touting their “AI” features have been non-starters, with the actual

scope of “AI” often limited to little more than basic algorithms that do little

in practice to impact the advisor marketplace. However, at the recent T3

Advisor Technology conference, a new generation of Artificial Intelligence

tools are emerging: rules-based

Expert Systems, which aren’t fully “artificial intelligence” – in that they

don’t actually learn from the data presented, and instead simply apply

a complex series of if-then statements and decision rules to navigate the

information – but do hold the promise of converting what has long been a series

of mental flowcharts and checklists that advisors implement in their heads

based on their CFP knowledge into technology-driven recommendations. After all,

the reality is that most of the technical knowledge of financial planning

really does amount to little more than understanding which analysis and

recommendations are appropriate given various information and data gathered

from and presented by the client… which in the end, is especially conducive to being commemorated

in checklists and flowcharts (which in turn can be programmed into

technology). Accordingly, the recent T3 conference witnessed the launch of both

FP Alpha, and also Intelligent Decision Tools, both of which

are rules-based

expert systems that gather various types of client data and use it to generate

prospective financial planning observations and recommendations. In the

case of IDT, the primary channel for gathering data is whatever clients input

to the software itself; with FP Alpha, the tools are built to actually scan key

client documents in PDF format (e.g., a homeowner’s insurance policy) to

identify key information and identify planning opportunities (akin to what Holistiplan debuted at the XYPN FinTech

competition last summer with respect to scanning tax returns to identify

planning opportunities). Notably, though, the new FP Alpha and IDT (and

Holistiplan) tools are not necessarily meant to be a replacement to traditional

financial planning software (still needed to do the calculation projections),

nor a replacement to financial advisors themselves (as both companies emphasize

they see their role to augment financial advisors, not replace them). After

all, even if an Expert System can fully identify all of the technical planning

opportunities, the reality is that financial planning is about more than just

telling clients what to do, it’s also about giving

them advice that they’ll actually implement that “sticks”… which, because

our brains are wired to interact with and communicate with other human beings

when deciding to change our behaviors, largely remains the domain of

human-to-human financial advice. Nonetheless, with Expert Systems beginning to

emerge, the shift of financial advisors from doing the analytics and crafting

recommendations, to helping

clients better discover what goals they really want to pursue and implement

the behavior changes to achieve them, may begin to accelerate if the

technology really can both improve the quality and consistency of advice (as

Expert Systems have the potential to not only ensure better recommendations and

that key information isn’t missed, but will also likely be compelling to

compliance departments that are especially concerned about the business

risks of inconsistent advice!).

Black Diamond Founder Reed Colley Continues Trend Of AdvisorTech Founders Returning For Second-Act Disruption. It was 1997 that Clayton Christensen first published “The Innovator’s Dilemma”, documenting the phenomenon of why large established firms with dominant market share and reach can still be “surprise” disrupted by new innovation. The problem, in essence, is that an innovation that makes a company successful in the first place often makes the business so large that it cannot justify deep ongoing investments into new ideas (in part because even if it “worked”, the early stage offering is often so small and niche that it can’t move the needle of sales/growth at a large firm). Yet by failing to do so, an emerging niche player can gain momentum, move upmarket, and by the time it reaches an ‘established’ product or offering it’s growing so fast that the incumbent doesn’t have time to react… and is thereby disrupted. In the context of the AdvisorTech world in particular, the challenge of the Innovator’s Dilemma appears to be playing out in a newly emerging pattern: founders that innovate and create AdvisorTech companies, sell them, and then re-appear as second-stage entrepreneurs to build the new innovation they ‘couldn’t’ build in (and that may even disrupt) their original company, from Oleg Tishkevich selling FinanceLogix to Envestnet and launching Invent.us, to Edmund Walters selling eMoney Advisor to Fidelity and launching Apprise. And now, at the 2020 T3 Advisor Technology conference, the pattern is playing out again, with the announcement that Reed Colley – founder of Black Diamond, which was sold to Advent for $73M in 2012 – is “back” launching a new company dubbed “Summit Wealth Systems”, hiring some ex-Black Diamond and ex-Advent leaders, to build a new performance reporting tool. Of course, “performance reporting” is already a crowded segment of the AdvisorTech landscape, but Colley emphasizes that the focus is not simply to build a new performance reporting competitor but to recognize that the ‘next generation’ of performance reporting is shifting away from how to do reporting better and into an entirely new format and approach of how to answer the client question “Am I going to be okay?” (A domain where most advisors still rely on external tools to relate investment results back to financial planning goals, or even just show the client’s path in an Excel spreadsheet.) Ultimately, whatever Summit Wealth Systems’ new offering will be, Colley indicated that it won’t likely be released until the 3rd quarter of 2020. But in a world where so much AdvisorTech creation and disruption has come from advisors themselves (building “homegrown” solutions to solve their own problems and then selling the solution to other advisors), the success of AdvisorTech in the 2010s – including a number of high-profile sales – appears to be driving an exciting new kind of AdvisorTech innovation in the 2020s: successful AdvisorTech entrepreneurs coming back with second acts with more resources, experience, and perspective than ever before.

AdvisorTech Re-Bundling Trend Accelerates As Carson Group Rolls Out “Free” Tech Stack. In the early days of financial advisor technology (the 1980s and 1990s), the “best” technology was found in wirehouses and other mega-firms that had the financial resources to invest into developing those tools, while independent advisors languished with a cottage industry of mostly homegrown tools. The rise of the internet and the emergence of APIs, however, turned this equation upside down, suddenly making it possible for various combinations of independent technology to be woven together, so accelerating the growth of independent advisors and their technology that today major ‘independent’ technology solutions like eMoney Advisor have more advisor users than all wirehouses combined! Yet the challenge of the explosion of the independent AdvisorTech ecosystem is that it forces advisors to choose the various combinations of tech necessary to make their own firm-specific tech stack… a challenge that many advisors, being focused on the financial services industry and their clients (and not being ‘techies’), are ill-equipped to handle. As a result, the nearly overwhelming plethora of AdvisorTech choices is leading to a new trend of “re-bundling”, where various advisor platforms try to group together the components of a valid advisor tech stack and offer a single consolidated solution, including both custodians (e.g., Fidelity WealthScape), broker-dealers (e.g., RBC Black), independent technology companies (e.g., Envestnet or Orion)… and now platforms that aggregate independent advisors together, such as Dynasty Financial, XY Planning Network, and most recently, the Carson Group. As while a subset of the most independent-minded advisors will likely always want “total” control of their technology – and continue to select their own tools one by one – the pressure and challenge of weaving together an ever-growing number of independent tools to properly integrate and pass relevant data and actions back and forth means that more and more advisors are willing to select a curated combination solution that will just “work” (based on the vetting and negotiation of their platform). Ultimately, though, the caveat is that not everyone can be a true advisor “platform”, and it remains to be seen which players will emerge as dominant when the bundled platforms of custodians and broker-dealers clash with the bundled platforms of technology companies which in turn are increasingly clashing with the bundled platforms of advisor aggregator platforms. Nonetheless, the key point remains: while the emergence of the internet and APIs has made it possible for an innumerable range of independent AdvisorTech solutions to blossom, in the end most advisors just want all their technology to “work” together… which means if the solution of the future isn’t a holy grail all-in-one, the opportunity remains for various advisor platforms to create their own all-in-one equivalents by patching the solutions together themselves into a bundled offering!

IndyFin Launches Online Lead Generation Solution With Bundled Prospect Screening Call Center. The good news of the ongoing shift of financial advisors towards providing increasingly holistic financial advice is that consumers receive broader and more integrated recommendations, and advisors have the opportunity to demonstrate a broader and more compelling value proposition to justify their fees. The bad news is that when ‘all’ financial advisors providing individualized and personalized comprehensive financial planning advice based on their credentials and years of experience… consumers can’t figure out which advisor to choose, and growth rates begin to slow as the average advisor increasingly struggles to differentiate from all the rest offering the same solution. This “crisis of differentiation”, in turn, has led in recent years to a proliferation of new “lead generation” services for financial advisors, bundling together the capabilities of the internet (and online/digital marketing) with the desire and willingness of financial advisors to pay quite generously for new clients. The caveat, however, is that most financial advisors don’t have well-developed sales systems to handle a significantly larger volume of prospective client leads… to the extent that a recent Kitces Research study showed that financial advisors are more satisfied with their lead generation services based on the quality of the leads (i.e., whether the prospect was qualified and really interested in doing business with the advisor) than the actual cost efficiency of the solution (i.e., whether the revenue generated is a good return on investment for spending on the lead generation solution). In this context, it is notable that a new lead generation solution – Indyfin – launched at the recent T3 Advisor Technology conference and, unlike other advisor lead generation competitors that simply try to serve up online prospects to advisory firms, will engage its own call center to pre-screen, vet, and qualify the lead before handing it off to the advisor (and then providing relevant prospect information to the advisory firm to help close the client), while only charging (and a revenue-sharing basis as a solicitor) for the prospects who actually close and turn into clients of the advisory firm. Of course, the caveat to all such advisor lead generation systems is that, in the end, they’re only as good as their ability to actually generate prospective leads in the first place – regardless of their screening and vetting process – and it remains to be seen whether Indyfin will be able to generate the necessary top-of-funnel flow of leads to put through their system and serve up a subset of the highest-quality prospects to advisory firms in the first place. Nonetheless, with a recent Kitces Research study showing that advisory firms have an average Client Acquisition Cost of $3,119 – much of which is based on the available time of the advisor and is therefore constrained by the advisor’s time – there is arguably still a substantial opportunity for whatever platform can first crack the advisor lead generation formula… for which Indyfin may be uniquely positioned by focusing on lead quality over just volume or lead generation ROI alone (which fits best into the psyche of how financial advisors actually like to buy and pay for leads!).

TwentyOverTen Launches LeadPilot And FMG Suite Launches Curator Integrated Content Marketing Platforms To Capitalize On Advisor Tech (Integration) Fatigue. For anyone in the business of “selling” – especially when they sell a complex product, or themselves and the complex value of their advice – one of the most important sales tools in the toolbelt are ones that help collect data from and ‘nurture’ prospects through the sales process (until they actually become clients). In the world of software sales itself, solutions like SalesLoft have filled the void, but in the realm of financial advisors there are remarkably few options beyond the relatively basic capabilities of advisor CRM itself (which is mostly focused on recording and capturing what advisors are already doing in the sales process, not to actually facilitate sales engagement itself). In turn, this gap for content marketing and digital engagement tools has led in recent years to the emergence of players like SnappyKraken as standalone third-party solutions. But given that advisor content marketing will generally happen on a financial advisor’s own website, it’s perhaps not surprising that advisor website maker FMG Suite launched Curator, and similarly, TwentyOverTen has launched its own embedded content marketing platform, dubbed LeadPilot. The emerging trend is interesting for two reasons. First, like SalesLoft (and unlike standalone CRM sales trackers), these new products will give advisors substantially more context on their prospects and make those first in-person interactions (when prospects move from the digital to ‘analogy’ realm) more value-packed. Rather than the same series of the same generic questions for each prospect, now advisors can tailor questions in their approach talks to what the prospect has already identified as the reasons they engaged. (Fingers crossed that this eventually starts to pre-fill financial planning software, too! Imagine the next-level client experience when a prospect comes in for the first time and the advisor already has their goals and profile built?!) The second reason these new content marketing platforms are interesting is the vertical integration with TwentyOverTen and FMG Suite’s core businesses. Already some of the more widely adopted website providers for advisory firms, it is a huge advantage that LeadPilot and Curator are architected to live inside TwentyOverTen and FMG Suite websites and inform the compliance dashboards (though notably, advisors don't need to be a TwentyOverTen website customer to use LeadPilot), potentially reducing the recent phenomenon of advisor “tech fatigue”. Advisor fatigue with their technology solutions is often attributed to advisors having too many software options to choose from, but in reality, it is a challenge of insufficient integrations to facilitate interactions between their client-related software tools. After all, a recent marketing technology study showed that the average non-financial services enterprise uses 91 pieces of marketing software in their tech stack and 43 pieces of sales/CRM related software! And every business has to purchase their non-industry-unique software as well (e.g., financial software for accounting, bookkeeping, and bill paying, productivity software like Microsoft Office or Google Apps, cybersecurity for firewall and intrusion detection, etc.). But the lack of consistent integrations across the key components facilitating the advisor-client (or advisor-prospect) relationship, in particular, can quickly produce advisor tech fatigue in the struggles of getting systems to “talk to each other” better. Thus, until the integration gets tighter in our industry, advisors will likely continue to be hungry for more bundled or vertically integrated software that reduces 3rd party integration headaches... as FMG Suite is now offering with Curator, and TwentyOverTen is offering with LeadPilot. Though ultimately, the real question, in the long run, is not the efficiency and integrations of advisor digital marketing platforms… but simply whether they can scale their website traffic enough to generate the necessary ‘top-of-funnel’ prospects to make those marketing systems work in the first place?

Timeline Launches LiveTrack As Retirement Planning Tools Shift From Upfront Planning To Ongoing Relationship Support. For most of its history going back to the origins in 1969, “financial planning” was a form of consultative needs-based selling where “The Plan” demonstrated a gap or need of the client… which the financial advisor could then “solve” with a product to sell, whether an insufficient amount of life insurance coverage (buy this insurance policy to eliminate the coverage gap!) or a retirement savings shortfall (add more money to this advisor-managed retirement account to get back on track for retirement!). Which means in practice, financial planning software has largely functioned as a (product-centric) point-of-sale tool, where data is gathered during the initial prospect or client process, analyzed, used to craft a recommendation, which is then implemented… and at that point, the financial planning software falls by the wayside until the client’s situation changes and a new analysis must be run (generally to identify a new sales opportunity). Yet with the ongoing shift to the assets under management model over the past 20 years – and more generally, the transition from a transactional-sales to an ongoing-relationship business model – the advice process for advisory firms themselves is less and less about the upfront “sale”, and instead far more about the ongoing advice and relationship experience with the client; after all, industry benchmarking studies routinely show that top advisory firms have 97%+ retention rates, which means the average client will be around for 30(!) years… even as financial planning software remains primarily focused on the first 3-6 months of the client relationship, and not the 29.5 years to follow! However, this perspective is beginning to shift, as various advisor-led software solutions are beginning to emerge that are focused more and more on not just what happens in the initial advice process with clients, but also how to track, monitor, and add value to the relationship on an ongoing basis as well. In this context, it is notable that at the recent T3 Advisor Technology conference, Timelineapp – which makes retirement planning tools to facilitate advisors implementing retirement portfolio-based sustainable withdrawal strategies – announced a new “LiveTrack” feature build to show not just whether the client can afford to retire (or not), but whether their ongoing spending in retirement is within the parameters of their original spending goals (given subsequent changes in value due to withdrawals and market performance, which can be pulled in from external portfolio performance reporting systems like Black Diamond via integration) and help clients understand in real-time when spending adjustments may need to occur to stay on track (and if the client does veer off track, notify the advisor to intervene). The good news of such ongoing real-time monitoring tools for clients is that they provide a way for the ongoing to demonstrate ongoing value outside of the portfolio management itself. The caveat, however, is that when the rest of the financial planning process still occurs within financial planning software, it remains to be seen whether third-party solutions like Timelineapp will be adopted separately and in parallel by advisors (where traditional financial planning software handles the upfront planning process and Timeline the ongoing), whether the two will become more integrated on an ongoing basis… or whether traditional financial planning software will finally begin to shift more effectively from being an upfront sales tool to an ongoing advice platform itself?

RightCapital Launches RightPay As Demand For Fee-For-Service Payment Platforms Grow. While the 1980s and 1990s were the heyday of the commission-based model of financial advisors selling mutual funds and insurance policies, and the 2000s and 2010s were the assets under management model of managing comprehensive portfolios, the 2020s are marking the shift into the “Financial Planning As A Service” approach where advisors charge ongoing non-commission non-AUM fees for ongoing financial planning advice or a calendar of ongoing planning services (e.g., in the form of monthly subscription fees or quarterly or annual retainer fees). The benefit of the Financial Planning As A Service (FPaaS) approach is that it expands the marketplace for financial advice itself, as advisors no longer must constrain themselves to clients who have investable assets that are liquid and available to manage (and clients willing to delegate), and instead can serve any type of client who simply has the financial wherewithal (from assets or from income) to pay for financial advice. The caveat, however, is that the commission-based model had a natural payment mechanism for the advisor (paid directly by the product company to its sales agent), as did the assets-under-management model (collected directly from the accounts that the advisor manages)… while the early stages of the FPaaS model has had to rely on collecting physical paper checks from clients (which is time- and labor-intensive, and very difficult to scale, especially in ongoing recurring revenue models that would collect checks on a regular monthly or quarterly basis). In turn, the difficulties in getting paid for FPaaS under various fee-for-service models has spawned the creation of third-party payment processing solutions like AdvicePay, built to fit into existing financial advisor technology and workflows and check the necessary boxes for financial advisor regulation when collecting financial planning fees via credit card or bank account ACH. To the extent that financial planning fees are collected for doing a financial plan, though, it is arguably more natural for clients to facilitate their financial planning payments from directly within their financial planning software… and accordingly, this month, financial planning software company RightCapital announced the launch of its own “RightPay” solution to allow advisors to bill client credit cards (but not currently bank accounts) for financial planning fees from directly within RightCapital. On the other hand, the caveat to having financial planning fee billing built directly within planning software is that few advisory firms operate an exclusively FPaaS model, and most are still at least working with some assets-under-management clients as well… which makes payment solutions more natural to integrate with AUM fee billing platforms than financial planning software. And in the context of large advisor enterprises – where it’s not uncommon to advisors to use different financial planning software solutions under one umbrella – collecting fee-for-service payments within one financial planning software isn’t feasible for the advisors who use other tools. Which raises the question of whether RightCapital offering RightPay will be able to induce enterprises to switch all of their advisors to centralize with RightCapital in order to gain the fee-billing efficiencies… or if instead, firms will choose to centralize their billing instead and allow their advisors to remain flexible in which planning software they use to generate the financial plans for which they’re charging their fees?

Fidelity Spins Off Akoya To Facilitate API-Based Account Aggregation Connections (That Won’t Constantly Break!?). In theory, account aggregation should be one of the greatest efficiency improvements available to financial advisors, facilitating a continuous flow of data that collects financial planning data, keeps it updated on an ongoing basis, and even helps advisors spot financial planning opportunities with clients in real-time. In practice, though, the efficiencies of account aggregation have been erratic at best, driven in large part by the inconsistency of the solutions themselves, with links to external accounts that routinely “break” and have to be re-connected (and cannot by reconnected by advisors themselves, instead often requiring clients to manually log in to update their credentials), and data that is ported inconsistently due to what is still a heavy reliance on ‘screen-scraping’ data directly from a website login rather than porting the data more directly (in a richer and more standardized format). And the situation hasn’t been helped by the fact that many external companies have used and leveraged account aggregation to facilitate transactions against the data providers themselves – for instance, platforms that use account aggregation from banks to automate transferring money away from those banks into higher-yielding alternatives, or others that leverage account aggregation data to help consumers find better deals on credit cards than what they currently hold. Yet with the recent acquisition of account aggregation facilitator Plaid by mega-incumbent Visa for $5.3B, account aggregation has suddenly be shifted from an ‘outsider’ platform threatening banks and credit card providers, to an industry participant that is a major credit card provider and key partner of banks… which on the one hand means account aggregation is here to stay, and on the other suggests that Visa may soon use its size and clout to ‘force’ the industry to play more nicely in the account aggregation sandbox. In this context, it is perhaps not surprising that Fidelity announced its own account aggregation ‘deal’ this month, spinning off Akoya, which will provide a secure API framework to facilitate account aggregation that is jointly owned by Fidelity and the Clearing House Payments Company and its 11 major member banks. In other words, Akoya is building towards a non-screen-scraping API-based alternative that should create more accurate data flows that remain more consistently connected (for all users of Akoya, which ostensibly will include Fidelity’s own eMoney Advisor). And because it will be owned by a conglomerate of banks and other incumbents, is ostensibly more likely to actually be adopted and implemented (whereas in past years, banks have often resisted more API-based solution that would be more stable and secure but may have also accelerated their own asset disintermediation). Ultimately, it remains to be seen which players, in particular, will prove dominant, and how Plaid and Akoya will position themselves against Envestnet’s Yodlee and other solutions… but the trend is clear towards industry incumbents that have historically held account aggregation at arms length instead bringing them into the fold, which from the advisor perspective should facilitate more accurate and stable data connections and the potential for more ways to leverage account aggregation beyond just flowing the data itself and into real-time financial planning actions and recommendations for clients!

Riskalyze And Fi360 Launch Regulation Best Interest Training And Support Modules As June 30th Implementation Date Looms. While critics have lamented that Regulation Best Interest failed to implement a full fiduciary duty to the recommendations provided by the registered representatives of broker-dealers, “Reg BI” has increased the standard that applies to brokers above what previously applied under the existing suitability standard. Which means, from a practical perspective, that broker-dealers will need to be even more mindful and vigilant in their oversight of their brokers to ensure that advice meets the new ‘Best Interest’ standard. As when a similar rule change occurred in 2016 under the Department of Labor’s fiduciary rule, one of the most straightforward ways for large broker-dealer institutions, in particular, to ensure compliance with new standards is to implement technology that itself can standardize and make their broker recommendations more consistent, easier to review (through technology channels), and leverage technology itself to help identify potentially problematic recommendations and/or to provide training to their brokers on how to deliver more effective (and compliant) advice. Accordingly, with the Regulation Best Interest implementation date of June 30th looming large, advisor technology firms are beginning to roll out their own solutions to help support Reg BI compliance, including a new series of Reg BI training modules from Fi360 (produced in collaboration with ERISA fiduciary guru Fred Reish), and Riskalyze is incorporating more Reg BI oversight capabilities into its tools as well… a trend that is likely to continue in the coming months as more broker-dealers focused on new Reg BI compliance requirements and technology companies aim to fill the void. In fact, with a lawsuit pending from XY Planning Network that could vacate Reg BI – just as the Department of Labor’s fiduciary rule was also vacated by an industry challenge – advisor tech firms are likely limiting how much they invest into Reg BI solutions (for fear of seeing their new offerings scrapped if the rule is vacated), and broker-dealers themselves will likely wait until the ‘last minute’ to fully implement their Reg BI compliance regimes (again just in case the rule itself is vacated). Which means if the courts rule in favor of the SEC this time around and Reg BI really does go through, there will likely be a mad scramble of AdvisorTech compliance solutions being rolled out and implemented in May and June?

Arizent’s Financial Planning Magazine Releases (Third) Annual “Best FinTechs To Work For” List. While the emerging shortage of next-generation advisor talent is creating an increasing focus on how to create high-quality appealing work environments to attract and retain that talent, when it comes to the technology industry, it already is – and has long been – a hyper-competitive environment for the best tech talent. The challenge is perhaps especially acute in the world of Advisor FinTech, where even “big” companies won’t likely ever reach the size and scale (and stock-option-compensation potential) of FinTech high-fliers like Stripe, SoFi, Plaid, and Gusto. Accordingly, Advisor FinTech companies have to compete with talent on the strength of their missions, the quality of their firms, and the appeal of the work environment itself. For several years now, Financial Planning magazine (via its parent company Arizent) has run a “Best FinTechs To Work For” list, which isn’t specific to the domain of Advisor FinTech, but does include a heavy component of AdvisorTech companies in particular. Popular AdvisorTech winners this year included investment research platform YCharts (#1), AdvisorTech consulting firm ActiFi (#2), digital marketing firm Snappy Kraken (#7), advisor CRM Redtail (#11), bond trading platform 280CapMarkets (#13), and portfolio performance reporter and all-in-one Advyzon (#34). Popular ‘perks’ included flexible work schedules, a $100/month allowance for local co-working spaces (for firms with remote employees), sabbatical and service awards, and generous employee health insurance and related benefits. Though ultimately, most of the leading firms appear to emphasize their culture and mission, more so than any particular financial or related perks!

In the meantime, we’ve updated the latest version of our Financial Advisor FinTech Solutions Map with several new companies, including highlights of the “Category Newcomers” in each area to highlight new FinTech innovation!

So what do you think? Are AdvisorTech entrepreneurs who sold their first companies and come back for ‘second acts’ the best way to push forward industry innovation? Do you think financial planning Expert Systems will gain adoption from advisors (or will they be viewed as a threat instead)? Is it better for advisor technology to remain unbundled, or become more bundled again? And is there really a gap for software solutions to help track and monitor client progress in the relationship after the initial financial plan?

Disclosure: Michael Kitces is a co-founder of AdvicePay and a member of the Advisory Board for Timeline, both of which were mentioned in this article.

Kyle Van Pelt, who contributed to the commentary on FMG Suite & Twenty Over Ten, is part of the Strategy team at SS&C Advent. You can connect with him via LinkedIn, or follow him on Twitter at @KyleVanPelt.

Michael Kitces is the Head of Planning Strategy at Buckingham Strategic Partners, co-founder of the XY Planning Network, AdvicePay, and fpPathfinder, and publisher of the continuing education blog for financial planners, Nerd’s Eye View. You can follow him on Twitter at @MichaelKitces.

Why “one big pool of money” needs predictability—and a plan.

Advisor recruiting climbed to its strongest pace in nearly two years, while CEO Richard Steinmeier said the firm has "cleared the decks" for bigger institutional deals.

The combinations involving MirrorWeb and AdvisorRankings illustrate how AI is reshaping both wealth firm operations and wealthtech platforms' business models.

New 5-in-1 onboarding tool aims to cut subscription paperwork as advisor demand for private markets accelerates

Connecting unique offerings with a specific client niche is a sure path to advisor satisfaction and success – but it all has to start with an intentional strategy.

Northern Trust’s Ken Lassner shows advisors how to convert volatility into after-tax portfolio gains

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income